The four game player populations of Cardano's reward pipeline — operators, delegators, non-participants, transaction submitters

Through epoch 623 · 2026/04/09Nicolas Henin · 2026/06/18

Before any conclusion can be drawn about how rewards are shared, a prior question must be answered: who is on the field, how many they are, how much capital each side controls, and who is paying for the chain that distributes the rewards. This report establishes that ground truth across the four game player populations that the SL-D1 reward formula operates on — pool operators, delegators, non-participants, and transaction submitters — and the ADA supply they share.

These four populations are not abstract roles; they are concrete, countable groups of addresses with measurable behaviours, capital, and overlap. The companion The Intended Game frames the staking mechanism as a game; this census names the players. Each chapter zooms in on one: §3 the pool operators, §4 the delegators, §5 the non-participants (the ADA that could play but doesn't, or can't by construction), §6 the transaction submitters (the addresses paying the fees that fund the pot). §2 sets the supply context they share.

The census is also, deliberately, a noise-removal protocol. The raw db-sync tables register 5,919 pools and 1.85M delegation certificates — but most of those pools earn no blocks and most of those certificates are ghosts of empty wallets. Iterative cleaning (production threshold → entity attribution → balance-bearing delegations) brings the productive count down to 733 pools and 1,227,281 delegations carrying 21.18B ADA. The companion Pools Pot Distribution and Operator's Cut reports chain off these cleaned denominators; every metric they report inherits the choices documented here.

The analysis spans the full Shelley history (epochs 211–627, ~5 years) with a snapshot anchor at epoch 623 for the staking-side aggregates (§2–§5) and at epoch 627 for the transaction-submitter analysis (§6, refreshed once Instance B's full db-sync caught up with chain tip). It produces twelve headline observations (CEN.O1–CEN.O12) that the rest of the report makes auditable. The headline picture below walks through the four populations in order.

Pool operators (§3) — the supply side has crystallised, and capital has flowed to consolidators rather than independents.21.75B ADA (60.2% of circulating supply) is staked across 2,877 pools. After cutting at the production threshold (≥3M ADA, the 95%-block-probability bar), the productive core is 733 pools controlled by 367 entities: 83 attributed entities hold 76.7% of productive stake through 449 productive pools, and within that 10 centralised exchange and institutional-validator entities alone hold 34.3% at structurally zero pledge. The pool count has been stable in a 700–1,000 band since epoch 300 — turnover at ~16 pools per epoch sustains the stock by replacement, not growth (3,497 entries against 3,070 exits over the full history). The mechanism's intended pathway from independent entrant to established operator has no observable expression: the independent single-pool segment contracted from 555 pools / 39.1% of stake at the epoch-300 peak to 291 / 24.4% today (a 48% loss), while multi-pool fleets grew from 23 → 85 entities and 135 → 660 pools, with the mid-tier (6–20 pool) entity count tripling. Capital flowed toward institutional consolidators, not toward the independents the design intended.

Delegators (§4) — the demand side is concentrated, settled, and price-blind.1.36M delegators carry 21.18B ADA across the productive pool set; concentration is extreme — 1,000 delegators (0.07%) hold 57% of staked ADA, the top 10,000 (0.74%) hold 79.2%, Gini 0.976. Concentration crystallised by epoch 300 and has not moved since: a 9× growth in delegator count has not budged the top-1% share. The base is bimodal — 42% loyal (201+ epochs, > 2.7 years), 21% volatile (≤ 5 epochs), 37% moderate — and switching collapsed 75% from 2,000–3,500 redelegations per epoch in early Shelley to 600–800 today. When delegators do switch, 50.5% land in pools with statistically indistinguishable yield (median ROS differential +0.02 bps), take direction is symmetric (30.8% cheaper / 31.5% pricier / 37.7% flat), and 92.1% of loyal delegations sit in the same 0–5% margin band — loyalty and low fees coexist rather than trade off. The one asymmetric signal is pool size: capital drifts toward larger pools regardless of price. Visibility, not return, is what moves stake — and most of the network's stake sits in the hands of its most actively-managed delegations (whales hold 65% of stake but only 38% of that capital is in loyal delegations).

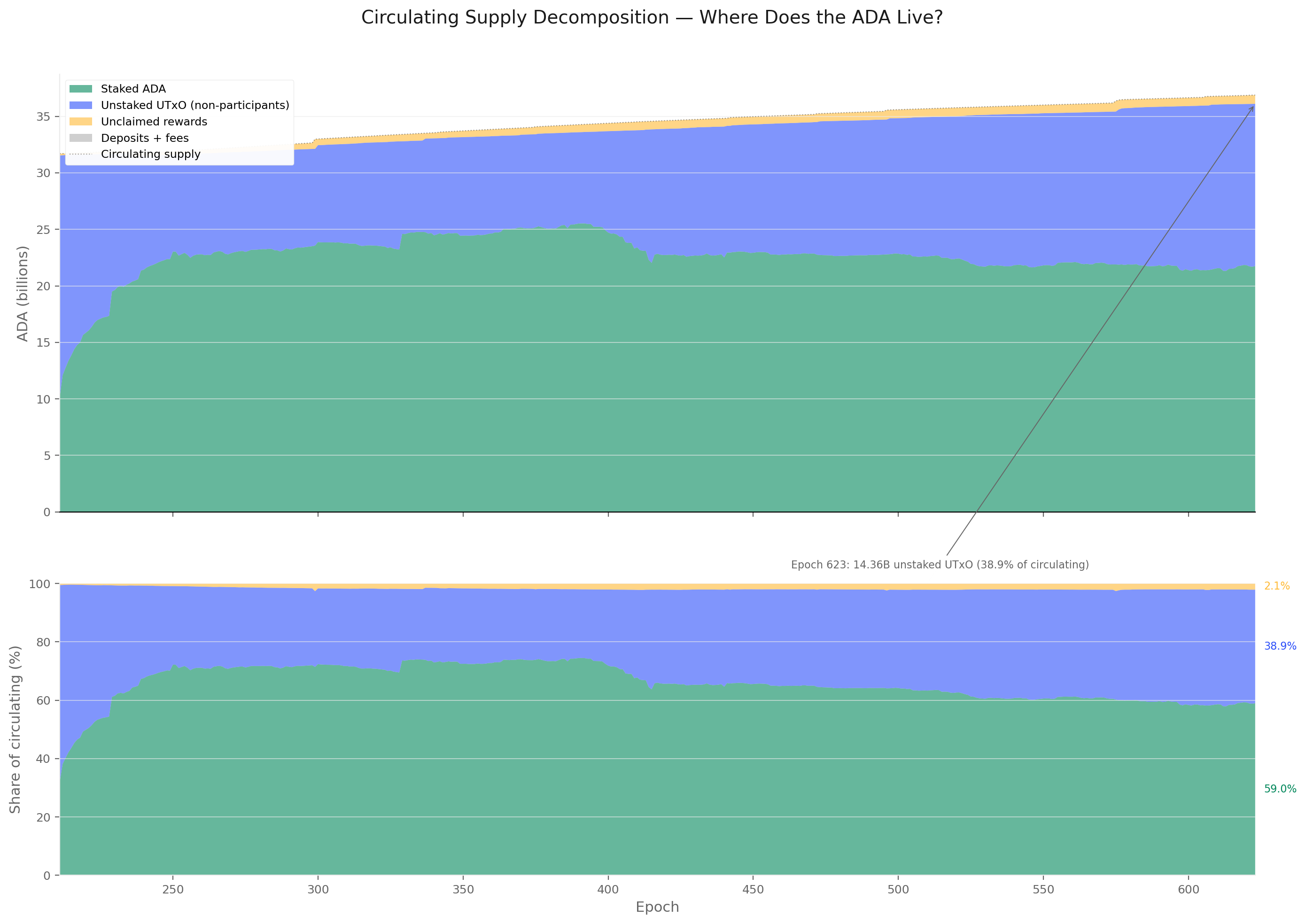

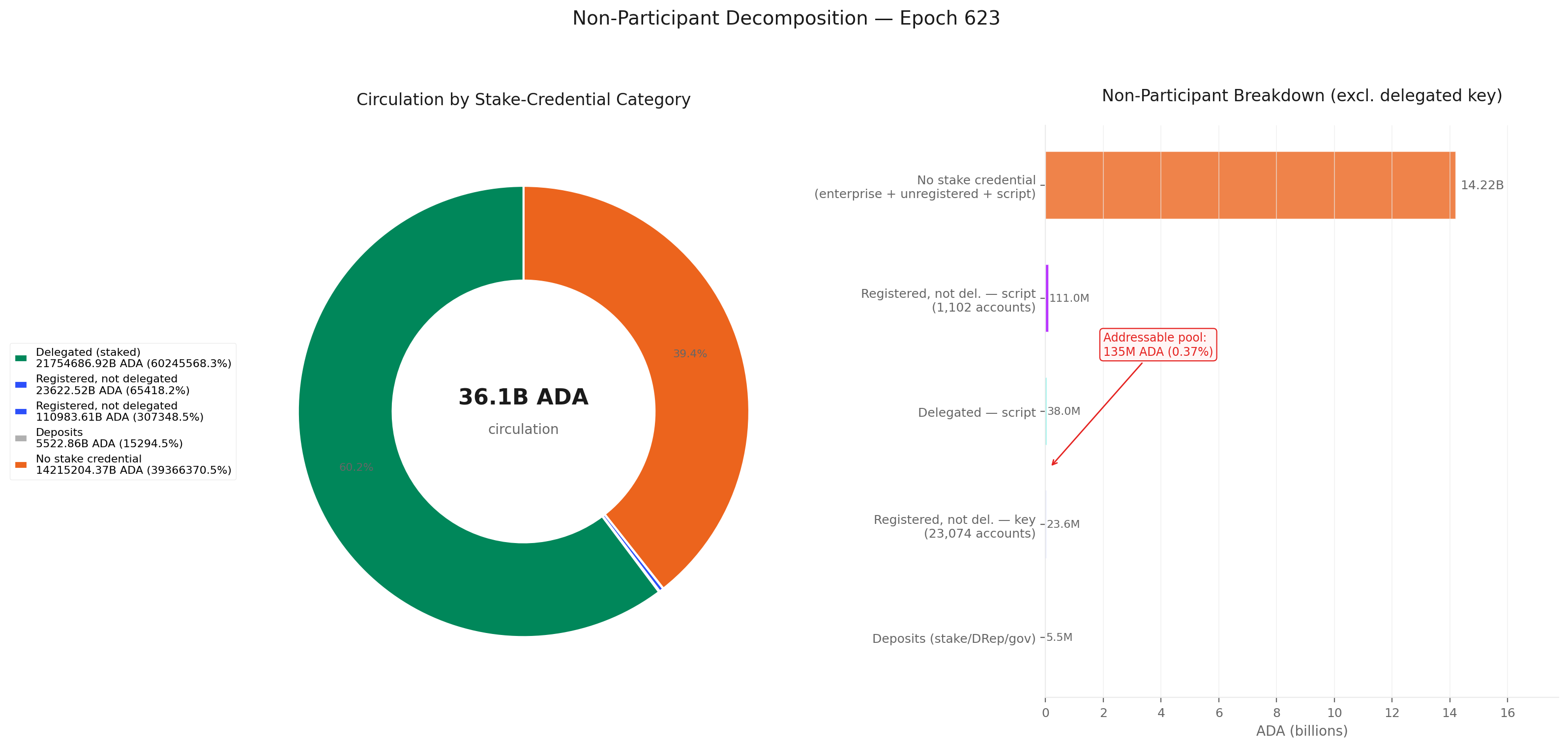

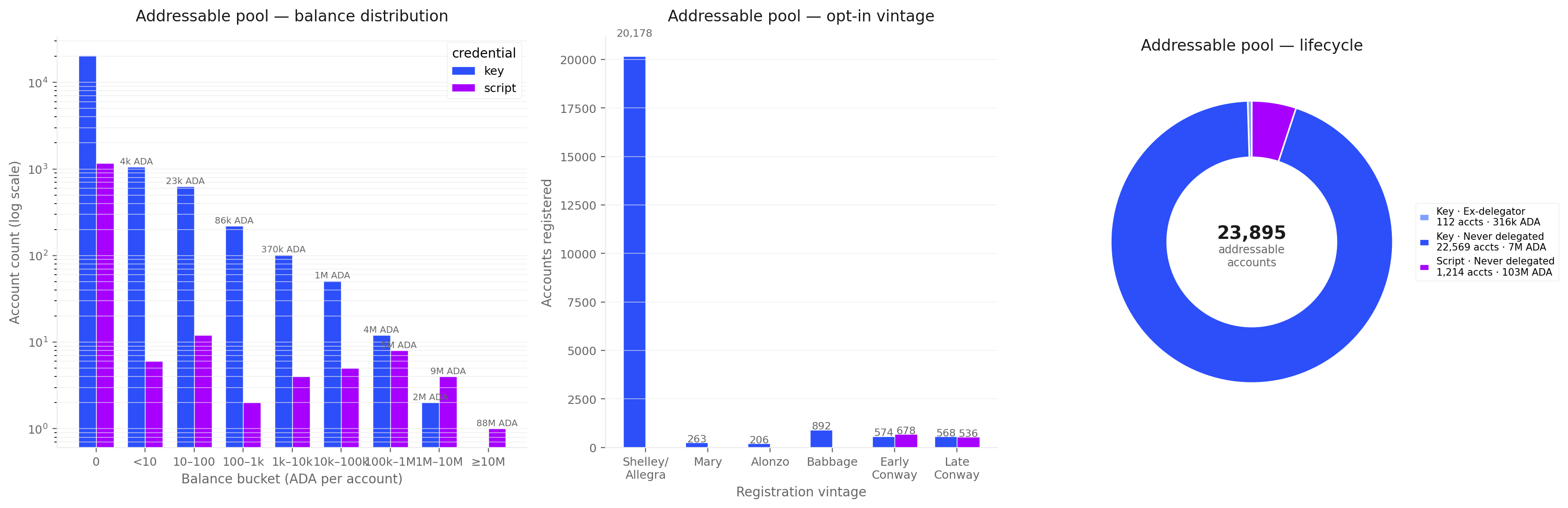

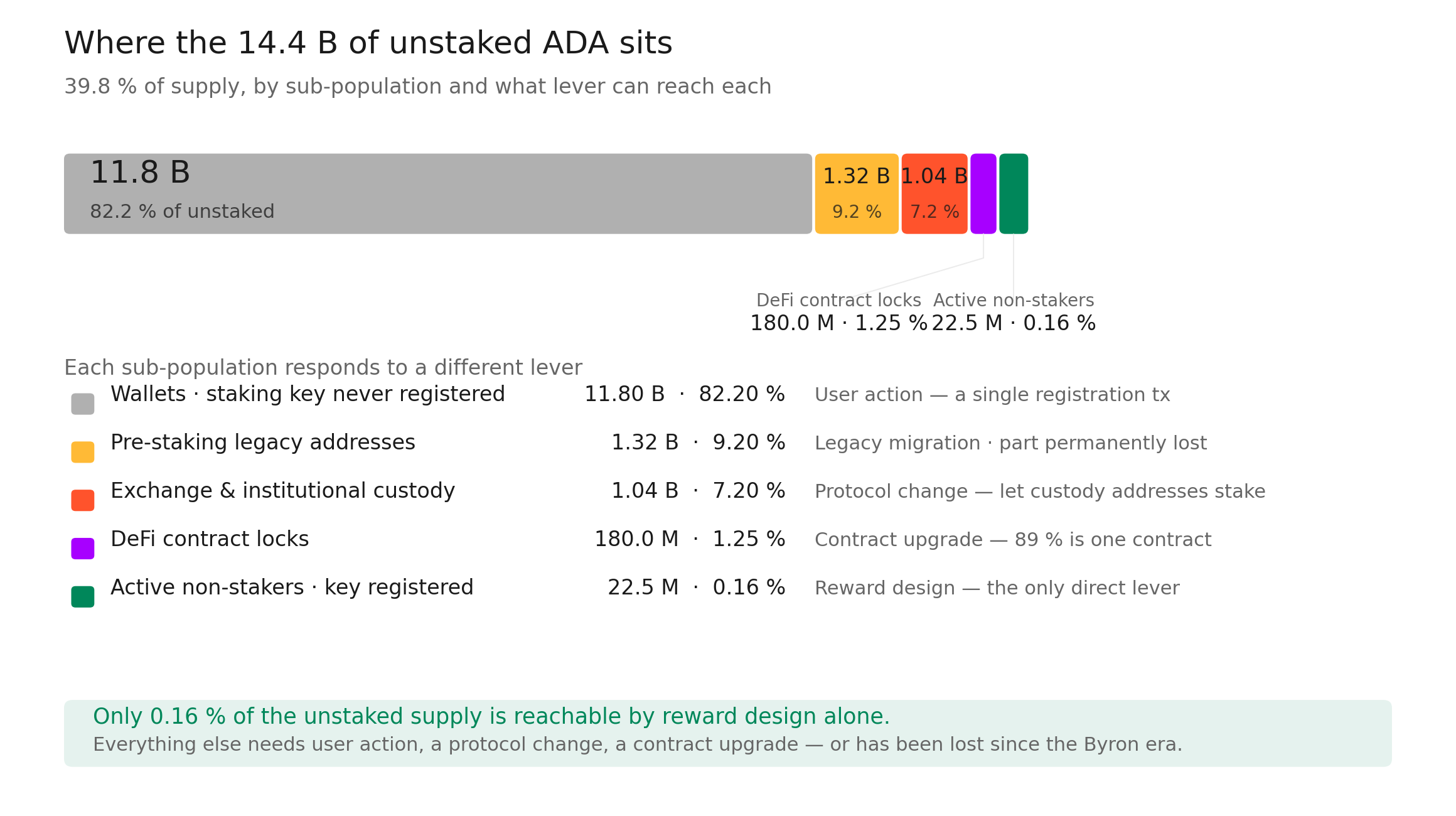

Non-participants (§5) — most of the unstaked supply is structurally beyond reach of any reward-design change.14.36B ADA (39.8% of circulation) sits unstaked, and only 134.6M (0.37%) belongs to accounts with a registered stake credential that have simply not delegated — the addressable pool that incentive design can, in principle, reach. The remaining 14.2B sits in addresses with no stake credential at all: enterprise (addr1v, exchange custody), script-without-staking (addr1w, Plutus contracts and DeFi vaults), Byron-era legacy, and base addresses whose staking key was never registered. The "unreachable" core is not a faceless retail tail — top-3 wallets control 19.1%, top-200 control 68.9% of the 2.5B identified residual; the addresses split into recognisable archetypes (exchange hot wallets, institutional cold storage, pre-staking-era legacy holders, DeFi vaults). The addressable pool itself collapses to ~2,100 active accounts and 0.06% of supply once zero-balance shells and a single 80M-ADA DeFi vault are removed. The recruitment ceiling is narrower than the headline 0.37% suggests by an order of magnitude — meaningful re-engagement requires changing the address architecture, not the incentive curve.

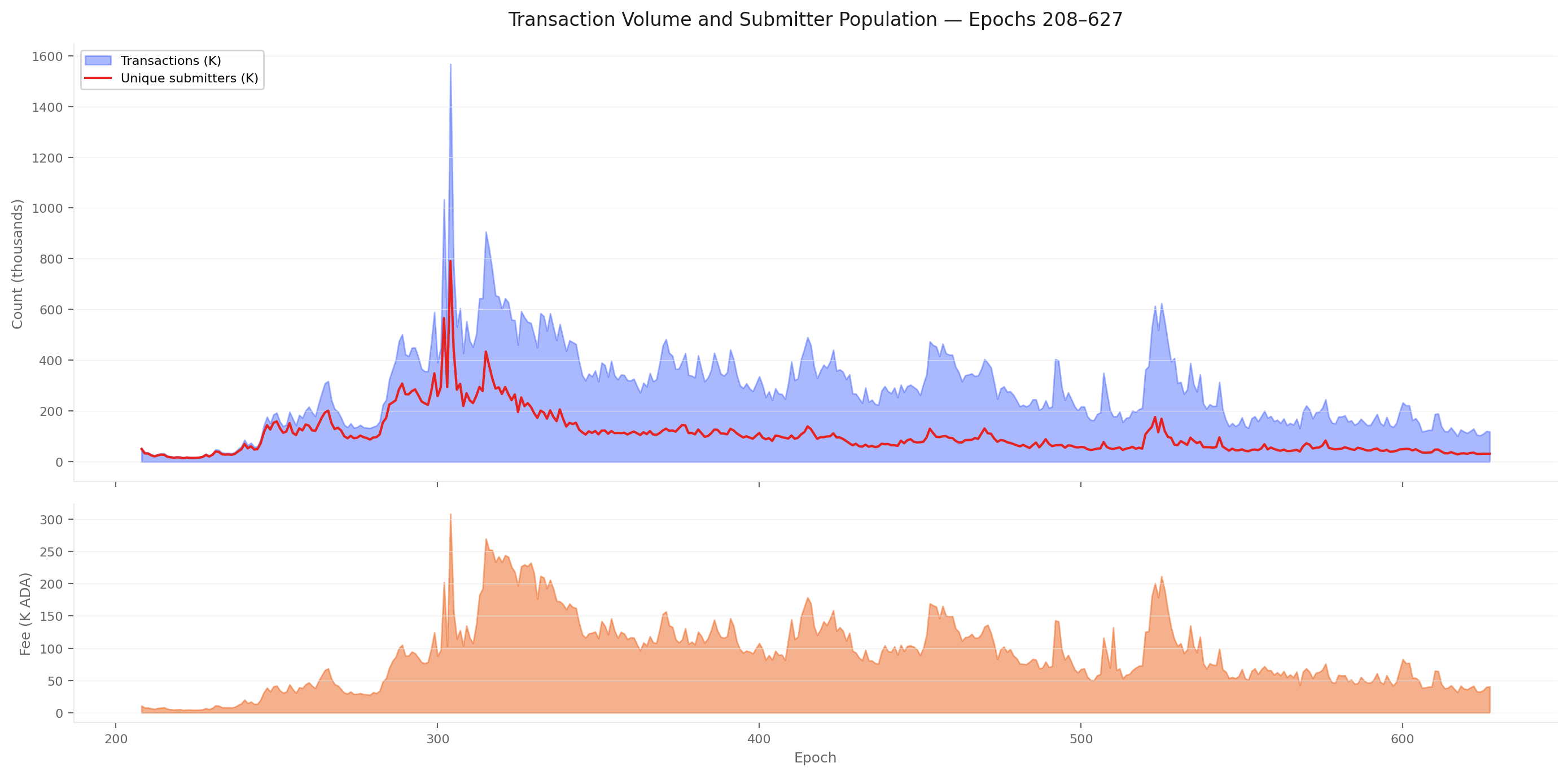

Transaction submitters (§6) — a shrinking population funds the chain, and the funders are largely not the people who get rewarded. Fees contribute roughly 0.2% of the current epoch pot; every long-term sustainability scenario assumes that ratio reverses, and the fee-paying population is moving the wrong way. Unique submitters fell from a peak of 790,335 (epoch 304) to 31,176 (epoch 627) — a 96% contraction against a 92% drop in transactions; the same shrinking core now transacts ~3.8× per epoch (vs ~2.0× at peak). The fee base is concentrated: the top 500 addresses pay 58.4% of recent fees out of ~147K active submitters, and the top 10 alone pay 20.0% — a recognisable handful (a MinSwap DEX-script, addresses tied to NUFI / TITAN / BERRY / OYSTR pools, plus enterprise-script DEX contracts and bot wallets). And the funder population barely overlaps the reward population: only 41.8% of fee revenue comes from currently-delegating addresses, 30.1% from addresses that structurally cannot delegate, 28.1% from base addresses that could delegate but aren't. From the delegator side, only 3.1% of the 1.352M active delegators submit any transaction in a 30-day window. Fewer than 4 ADA in every 10 ADA of fees flow back through the delegation channel to the population that paid them.

Table of Contents

1. Mainnet Observations

CEN.O1

Observation 01 · 9 findings

Multi-pool entities flourished (23 → 85 entities, 65% → 76% of productive stake) while single-pool operators struggle (555 → 291 pools, 39% → 24% of stake)

9 findings

The designed entry → growth → established path is no longer observable. The productive set tracks a 700–1,000 band since epoch 300 (733 pools at epoch 623 as the threshold rises with total stake), with only 1.7% turnover per epoch — but composition has hardened underneath that flat aggregate. 83 attributed entities control 76.7% of productive stake (12 with 11+ pools alone hold 41.0%); multi-pool fleets grew from 23 to 85 while single-pool operators contracted from 39.1% to 24.4% of stake.

Three quarters of registered pools are economically irrelevant. 2,144 of 2,877 (75%) sit below the production threshold (~3M ADA) and together hold only 2.7% of stake

Three quarters of productive stake sits in 83 named entities. They control 76.7% through 449 productive pools (71 strict multi-pool + 12 attributed single-pool) — and the count is a lower bound (operators using fully separate per-pool infrastructure stay invisible)

The pool count flat-lined since epoch 300; the equilibrium is replacement, not growth. The productive set tracks a 700–1,000 historical band (733 at epoch 623) with 1.7% turnover per epoch — 3,497 entries against 3,070 exits balance to near-zero net flow

Concentration is heavy-tailed: 12 entities run 41% of productive stake. Of the 83 attributed, 12 with 11+ productive pools control 41.0% (8.69B / 21.18B); the top 2 alone (Coinbase 41p, YUTA 25p) hold 13.4%

Independent operators are losing the field — 48% pool-count loss in 323 epochs. Single-pool operators contracted from 555 pools / 39.1% of productive stake (epoch 300 peak) to 291 / 24.4% (epoch 623); the contraction has accelerated in the most recent window

Multi-pool entities absorbed the contraction and then some — fleet count nearly quadrupled. From 23 entities / 135 pools / 65% of stake (epoch 210) to 85 / 660 / 75.6% (epoch 623); the mid-tier (6–20 pools) tripled in entity count and nearly doubled in stake share

The mechanism's designed progression path is invisible in the data. Entry → growth → established is supposed to feed the independent segment; instead the independent population is contracting and the replacement pools that maintain the productive total are entity-operated

On-chain attribution alone misses the bulk of fleet structure — 4 entities vs 85, a ~20× jump. Most multi-pool operators use separate keys per pool, so on-chain ownership clustering catches only the small minority that doesn't separate keys; any analysis stopping at the on-chain layer materially understates MPO concentration

Methodological — attribution layer matters

CEN.O2

Observation 02 · 1 finding

When a Titan delegator switches pools, the whole pool moves with them — whale-funded pools swing ±20% between epochs (1 in 5 swings >50%) while retail pools barely move (±8%)

1 finding

A pool's stake stability depends on who its delegators are — not on the market segment it competes in. In whale-funded pools (the 28 custodial-by-delegation pools, where the typical delegator holds ≥ 100K ₳), a single Titan-tier address (10M+ ₳) is large enough that when they move, the whole pool moves: stake swings ~±20% between epochs, and 1 in 5 of them swings more than 50%. The operator loses revenue predictability and the remaining delegators see their block-production rhythm wobble. Retail pools (broad small-delegator base) absorb churn smoothly — they only move ±8% between epochs. Custodial-by-extraction pools (≥ 99% margin) barely budge (±7%) because their delegators are locked in by inertia. What looks like delegator activity in the aggregate is mostly a handful of institutional treasuries shifting capital.

A single Titan delegator moving in or out can shake a whole pool — whale-funded pools swing ~±20% between epochs vs ±8% for retail. In the 28 custodial-by-delegation pools (typical delegator holds ≥ 100K ₳), stake moves by roughly ±20% between epochs, with 21% of them swinging by more than 50% — these are pools where a single address is large enough that its movement dominates the variance. Retail (809 pools, broad small-delegator base) is mostly stable (±8%) — no single delegator can move the pool. Custodial-by-extraction (79 pools, ≥99% margin) is the most inert (±7%) — stagnation, not active management

Segment-driven variance

CEN.O3

Observation 03 · 3 findings

The delegator population is wildly skewed in stake — 1,000 of 1.36M delegators (0.07%) hold 57% of staked ADA, and 9× population growth has not shifted the shape

3 findings

The delegator population is shaped like a power-law tail — almost all the staked capital sits in a tiny upper sub-population. Of the 1.36M active delegators, 1,000 (0.07%) hold 57% of staked ADA; the top 10,000 (0.74%) hold 79.2%; Gini = 0.976 — more concentrated than US wealth (~0.85) and comparable to the most unequal asset distributions in financial markets. The median delegator holds just 32 ADA while the mean is 16,055 ADA — a 500× gap that quantifies the skew. The population has grown 9× since epoch 300 without changing its shape: every cohort of new entrants has joined at the bottom of the distribution, leaving the top-1% share locked at 78–82%.

Half the delegator base stakes less than a single transaction fee at peak congestion. Median: 32 ADA. Mean: 16,055 ADA. The 500× gap measures the skewness of a power-law distribution where each tier above 10K ADA holds roughly 20% of total stake despite containing exponentially fewer delegators

The delegator population's stake is concentrated in its top 0.07%.1,000 delegators (0.07% of the 1.36M population) hold 57% of staked ADA; the top 10,000 (0.74%) hold 79.2%. Gini = 0.976 — more concentrated than US wealth (~0.85) and comparable to the most unequal asset distributions observed in financial markets

Concentration crystallised by epoch 300 and has not moved since. A 9× growth in delegator count has not budged the top-1% share (locked at 78–82%) — new entrants are overwhelmingly micro-delegators (<1K ADA, 96% of new joins) who inflate the denominator without touching the numerator. The economic weight of staking was set in its first ~90 epochs

Structural lock-in

CEN.O4

Observation 04 · 3 findings

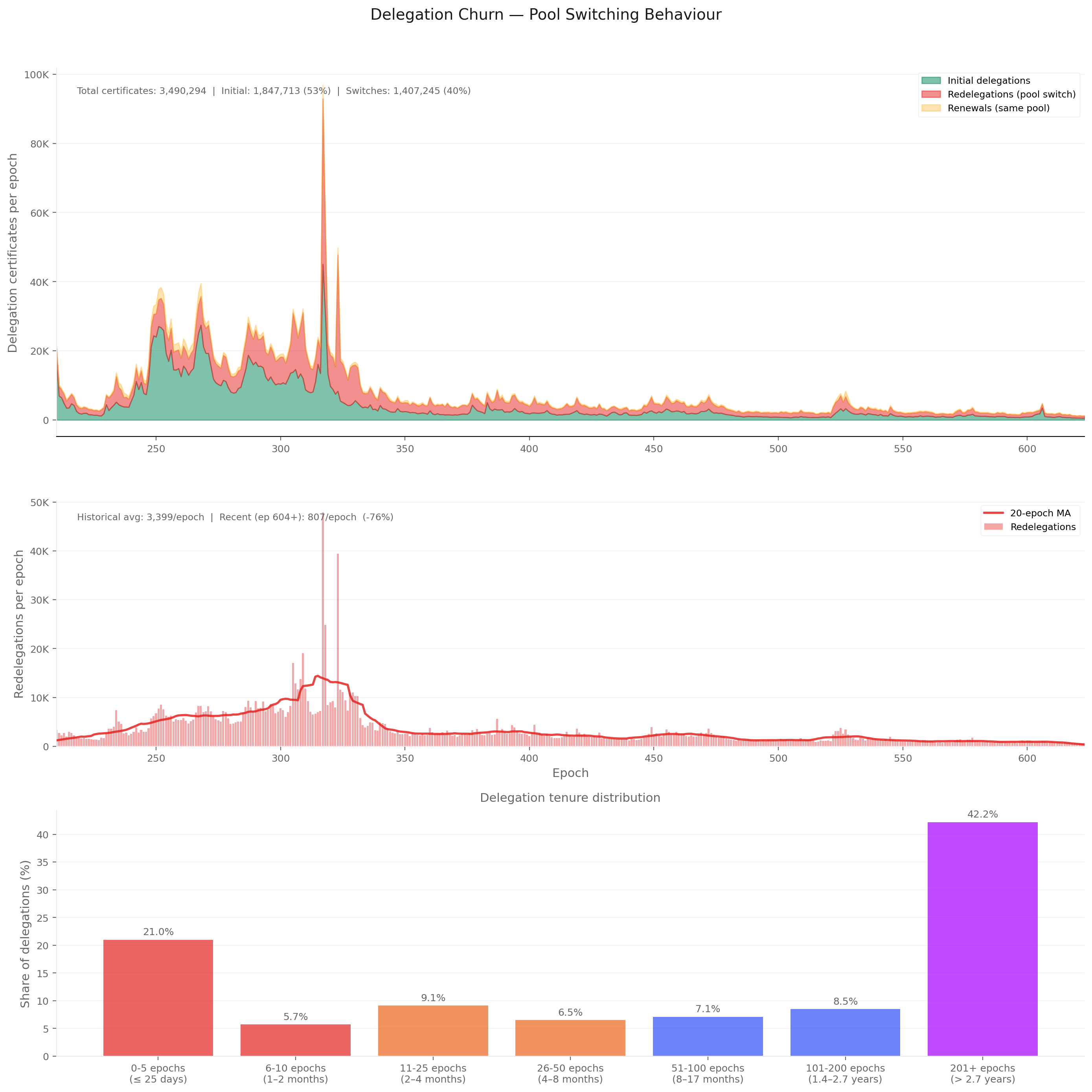

Most delegators stay put for years — 42% have stuck with the same pool for 2.7+ years, only 21% switch within 25 days, and the population's switching rate is 75% below early Shelley

3 findings

The delegator population settled long ago — most of it doesn't move. Tenure splits the population cleanly into three sub-groups: 42% have stayed with the same pool for 2.7+ years (201+ epochs), 21% switch within 25 days (≤ 5 epochs), 37% sit in the middle (somewhere between). Aggregate switching has collapsed 75% from 2,000–3,500 redelegations per epoch in early Shelley to 600–800 today — three regimes: experimentation → middle → mature. And almost all of that switching comes from the retail population: custodial and private pools barely move.

Pool-switching collapsed 75% from early Shelley. Redelegations fell from 2,000–3,500 per epoch (early Shelley experimentation) to 600–800 today — three regimes: experimentation (epochs 210–260) → middle period with hard-fork spikes (260–500) → mature settled market (500+)

The base splits cleanly into stickers and switchers, with a thin middle. 42% loyal (201+ epochs, > 2.7 years), 21% volatile (≤ 5 epochs, < 25 days), 37% moderate. The loyal majority anchors pool economics; the volatile tail generates the bulk of the churn signal

Switching is a retail-market phenomenon — custodial and private pools contribute negligible churn. A retail-only filter (margin < 99.9%, excluding by-pledge / by-extraction custodial) produces near-identical aggregates: 40.0% switch rate, 42.4% loyal tenure, ~799 redelegations per epoch

Churn is retail-only

CEN.O5

Observation 05 · 2 findings

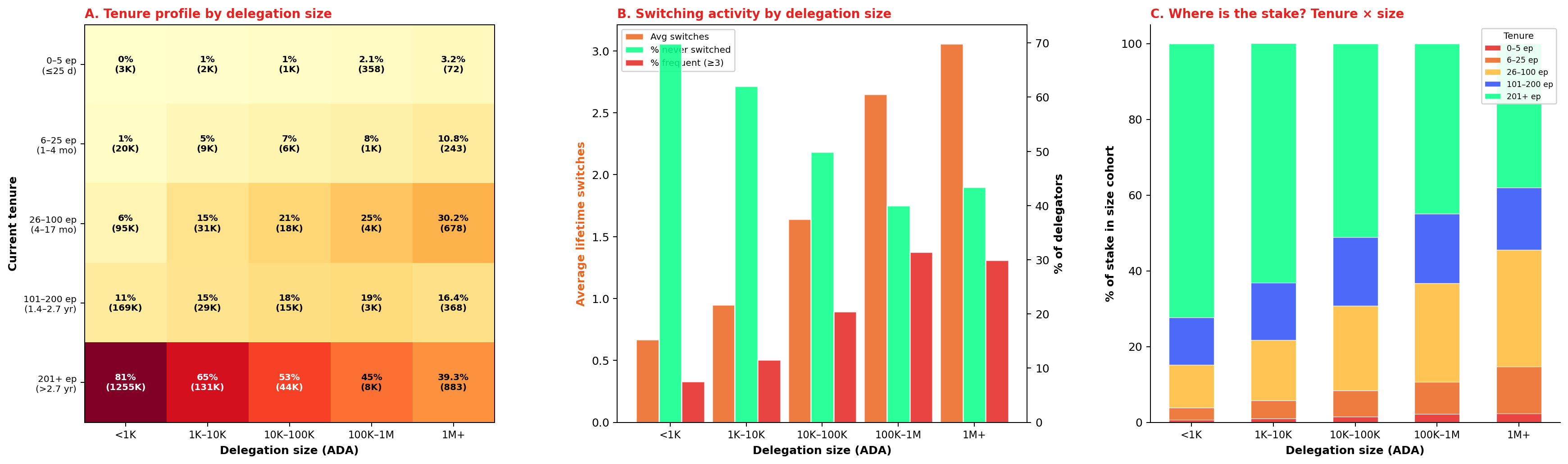

The bigger the delegation, the more it moves — whales (1M+ ₳) hold 65% of the staked supply and switch ~4× more often than small delegators

2 findings

The bigger the delegation, the more often it moves. The smallest delegators (< 1K ₳) average just 0.67 pool switches over their lifetime — they delegate once and forget. Whales (1M+ ₳) average 3.06 switches — about 4–5× more. And whales hold 14.1B of the 21.8B staked supply (65%) — yet only 38% of that capital sits in long-term (201+ epoch) delegations. The bulk of the network's staked capital sits in the hands of its most actively-managed delegations. Pool operators depending on a few whale delegators therefore face structurally higher stake instability than those with a broad retail base.

Most of the network's staked capital sits in delegations that move. Whales (1M+) hold 14.1B of the 21.8B staked total (65%), yet only 38% of that stake sits in loyal (201+ epoch) delegations — the rest distributes across moderate and volatile tenures. Pool operators dependent on a few large delegations face structurally higher stake instability than those with a broad base of small loyal delegators

Capital instability

CEN.O6

Observation 06 · 5 findings

The delegator population doesn't shop on price — half their switches produce zero yield change, switch direction is balanced (30.8% cheaper / 31.5% pricier), and 92% of long-term delegators sit in the cheapest 0–5% margin band

5 findings

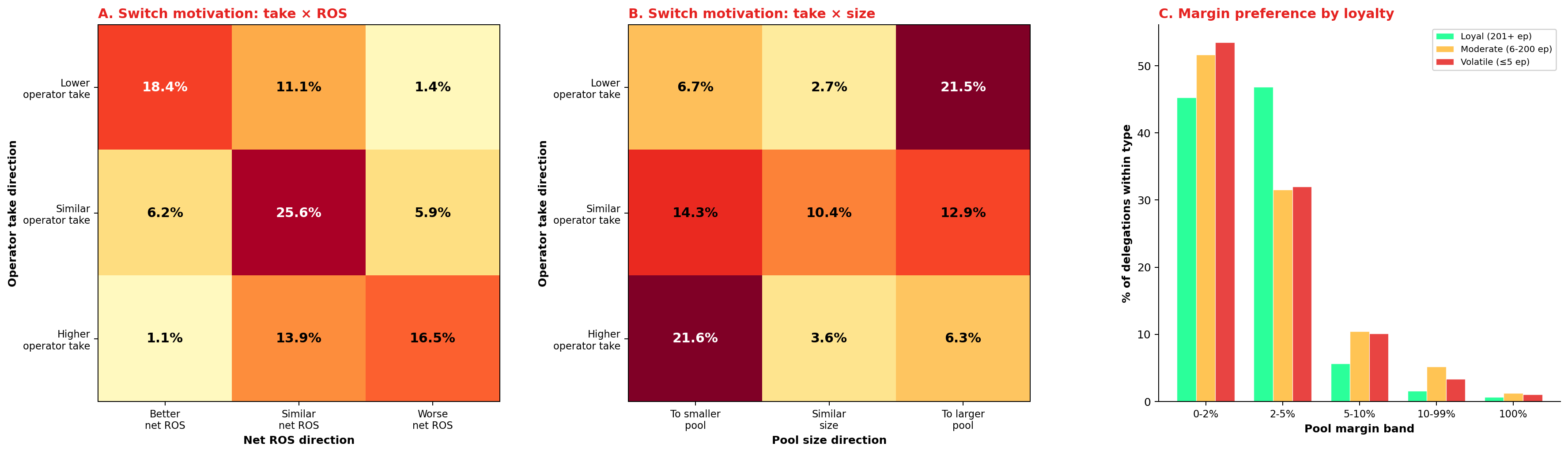

The delegator population behaves like passive parkers, not yield-shoppers. When delegators do switch, half (50.5%) land in pools with statistically indistinguishable yield (±5 bps; median ROS differential +0.02 bps — well below any threshold a delegator could observe). Switch direction is symmetric too: 30.8% go cheaper / 37.7% stay flat / 31.5% go pricier — no fee-chasing pattern. The one asymmetric move is by pool size (the population drifts toward larger pools regardless of price). And 92.1% of long-term delegators (201+ epochs) sit in the cheapest 0–5% margin band — the cheapest pools are also the stickiest, so loyalty and low fees coexist, they don't trade off. The DeFi sub-population is essentially absent: 99.83% of staked ADA is key-based; only 38M ADA across 399 script addresses is held by smart contracts.

Delegators cannot see what they're paying for — the yield signal is too flat to act on. Half of all switches (50.5%) produce zero yield change (±5 bps); the median ROS differential is +0.02 bps with an interquartile range of −0.47 to +0.55 bps. The signal is an order of magnitude below any threshold a delegator could observe, let alone optimise against

Operator take direction is balanced — no fee-chasing pattern is detectable. 30.8% of switches go to a cheaper pool, 31.5% to a more expensive one, 37.7% land at the same take. The take × ROS matrix's diagonal dominates (lower take → better ROS at 18.4%, similar → similar at 25.6%, higher → worse at 16.5%) — confirming take and ROS are two views of one signal, and that signal is too flat to drive behaviour

Pool size — not price — is the only asymmetric signal in switching behaviour. Moves to smaller pools tend to accept higher take (21.5%), moves to larger pools tend to stay take-neutral (21.0%). The asymmetry suggests moves toward small pools follow non-economic factors (community affinity, retirement at origin, decentralisation preference); moves toward larger pools follow a path of least resistance — visibility, not optimisation

Loyalty and low fees coexist — the cheapest pools are the stickiest. 92.1% of loyal delegations (201+ epochs) sit in the 0–5% margin range. Loyalty is a consequence of initial pool selection into the competitive neighbourhood, not a barrier to leaving it; fees segment the market at entry, not during tenure

DeFi operates almost entirely outside the staking system. 99.97% of delegations and 99.83% of stake are key-based; script-based delegation (smart contracts, multisig, governance) is 399 addresses and 38M ADA. The DeFi ecosystem has not integrated with delegation in any meaningful way — and the credential type cannot separate custodial from retail capital, since both present as key-based

No smart-contract staking

CEN.O7

Observation 07 · 8 findings

The non-participant population is 39.8 % of the supply, structurally inert, and held by a tightly-concentrated minority of custodians and legacy holders

8 findings

The non-participant population — addresses controlling ADA that is not delegated to any pool — has been stable at 36–39 % of circulation for over 300 epochs (14.4 B ADA at epoch 623). Only 0.37 % of circulation is reachable by reward design (registered staking key but not delegated); the remaining 39.4 % sits in addresses that cannot delegate without a protocol-level change. The "unreachable" core is not a faceless retail tail — 246 wallets hold 74 % of it, top-3 alone hold 19 %; the addresses split cleanly into recognisable archetypes (exchange hot wallets, institutional cold storage, pre-staking-era legacy holders, DeFi vaults). The "addressable" pool collapses to ~2,100 active accounts and 0.06 % of supply once zero-balance shells and a single DeFi vault are removed. The reward mechanism's recruitment ceiling is narrow; meaningful re-engagement requires changing the address architecture, not the incentive curve.

The staking rate is structurally declining despite persistent net delegator inflows. The rate has fallen from 71% (epoch ~260) to 59% (epoch 623) — a 12 pp loss over ~360 epochs. Circulating ADA grew from ~32B to ~37B while staked ADA grew from ~23B to only ~22B; the non-participant pool is growing faster than the staking pool.

14.36B ADA (39.8% of circulating supply) does not participate in staking — and only a sliver of that is reachable by reward design. The non-participant pool has been stable at 36–39% for over 300 epochs. Only 0.37% of circulation (134.6M ADA, 24,176 accounts) is nominally addressable by an incentive-design change — and even that figure shrinks under scrutiny (§5.5). The remaining 39.4% sits in addresses that cannot delegate without a protocol-level change.

The non-participant floor is structural, not behavioural — incentive changes alone cannot reach 99% of it. Reward-mechanism changes (curve adjustments, fee-structure reforms) can at most shift the 0.37% addressable pool. Moving the other 39.4% requires protocol-level changes — enabling exchange-style addresses to stake, mandating staking-capable DeFi script standards, or introducing delegation-by-default for newly minted wallets.

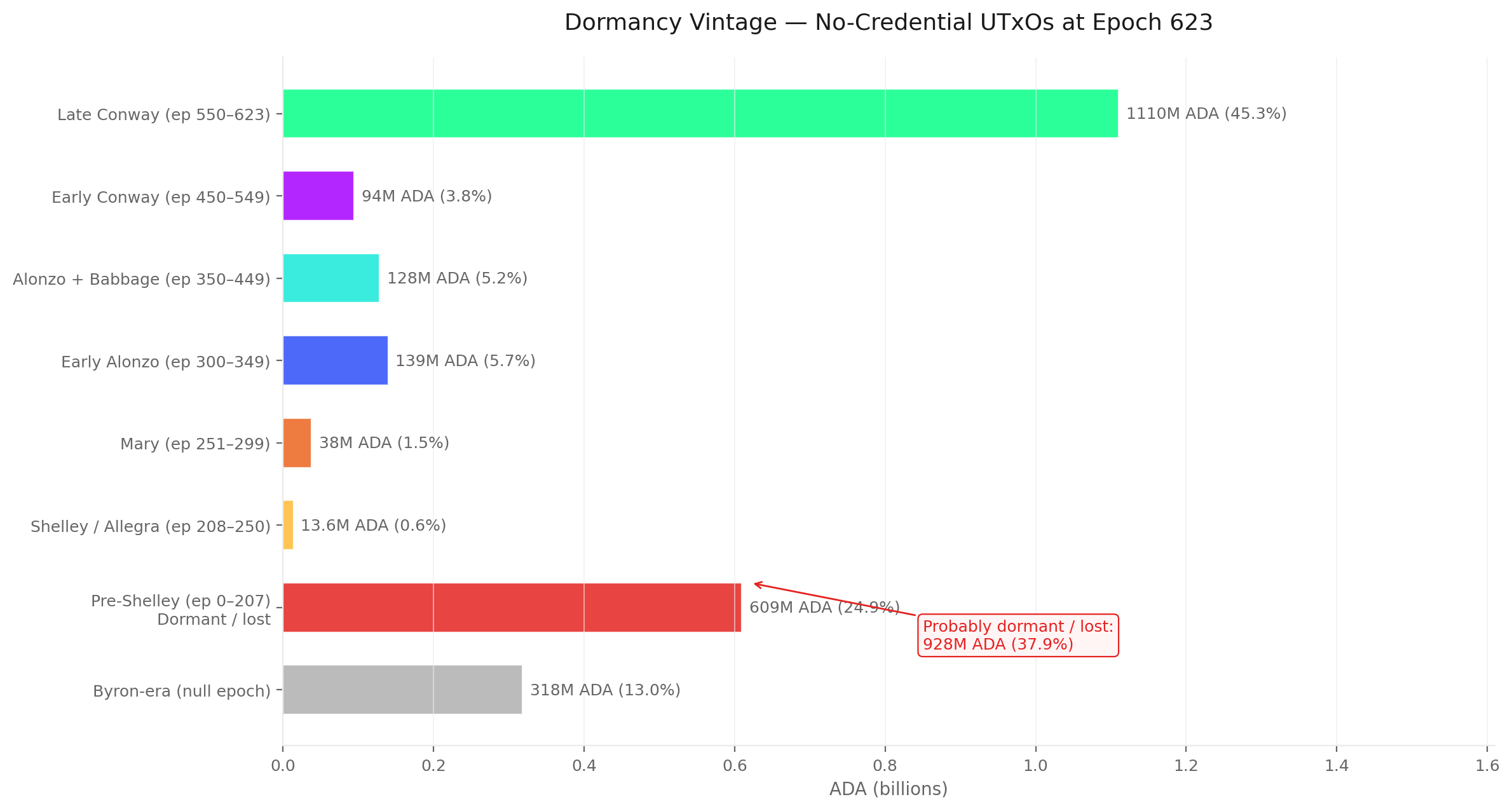

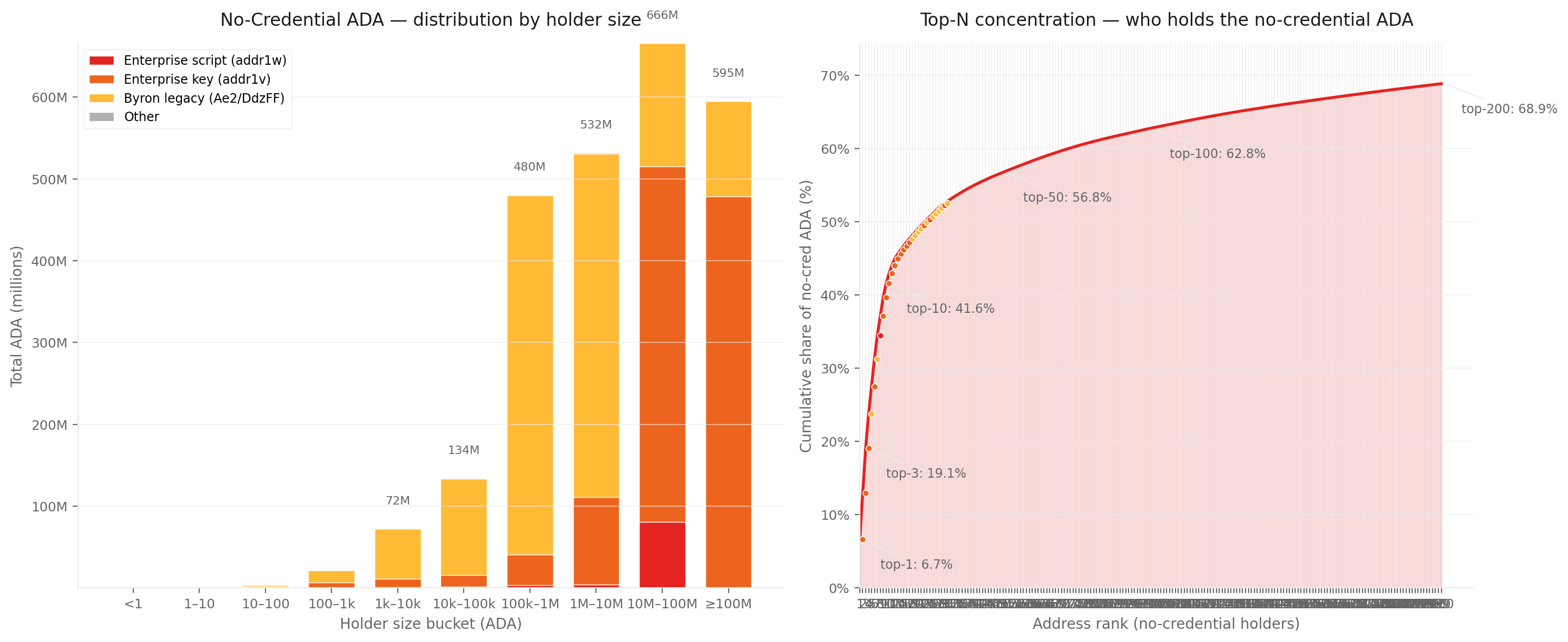

The "no staking key" residual is dominated by legacy and custody, not by active DeFi. Among the 2.45B identified by address shape, exchange-style addresses (1.04B) and pre-staking-era legacy addresses (1.32B) together account for 96%. DeFi contract addresses without staking total just 91M — one tenth as much, growing only slowly. The remaining ~11.8B sits in standard wallets where the holder never bothered to register a staking key. The unreachable mass is overwhelmingly inertia, not active opt-out.

The no-staking-key pool is bimodal: 37% is pre-staking-era dormant, 44% is from the last 73 epochs — the middle is empty. The dormant fraction (928M) erodes at about 0.8M ADA per epoch as wallets occasionally awaken. The recent fraction (1,110M from epochs 550–623) reflects active exchange and DeFi cycling. The middle eras are essentially spent — the population splits cleanly into probably lost and operationally active, with very little in between.

The structurally-excluded 2.5B is held by a few hundred wallets, not by a diffuse retail base. Top-3 wallets control 19.1%, top-10 control 41.6%, top-200 control 68.9% of the 2.5B residual. The top of the distribution splits into recognisable archetypes — exchange hot wallets, institutional cold storage, pre-staking-era legacy holders — addresses that can be named, not anonymous retail. Any policy aimed at this pool acts on a small, identifiable counterparty list.

DeFi-locked-without-staking is a one-contract problem, not an ecosystem problem.89% of the 91M residual lives in one 80M-ADA contract; the remaining 99 contracts together hold ~10M (11%). Mandating staking-capable contract addresses in DeFi standards would primarily move that one contract — the rest of DeFi has either already integrated staking or holds amounts too small to materially shift the residual.

The "addressable" pool is mostly inert — the real ceiling for reward-driven recruitment is 0.06% of circulation, not 0.37%. Of the 24,176 nominally-addressable accounts, 91% hold zero ADA, 89% have been dormant since the first 41 epochs of Shelley, and 80% of the residual ADA sits in one DeFi vault. The genuine ceiling for reward-driven re-engagement is ~22.5M ADA (0.06% of circulation), spread across ~2,100 active accounts. The reward mechanism's recruitment ceiling is narrower than the headline 0.37% suggests by an order of magnitude.

Real ceiling on reward-driven recruitment

CEN.O8

Observation 08 · 2 findings

The active submitter population is shrinking and concentrating into a smaller, more active core

2 findings

The submitter population — addresses paying fees in any given epoch — collapsed from a peak of 790,335 actors (epoch 304) to 31,176 (epoch 627), a −96% contraction against only a 92% drop in transactions. The same population now transacts ~3.8× per epoch (vs ~2.0× at peak), and the address-to-transaction ratio fell from 0.88 (epoch 210) to 0.26 (epoch 627). The chain is not losing activity; the population doing it is shrinking while each surviving member transacts more often.

The submitter population peaked at 790K addresses and has since contracted by 96% — the chain runs busily, with a much smaller crowd. The population grew in step with transaction count through early Shelley, peaking at 790,335 unique addresses and 1,566,974 transactions at epoch 304 (the CNFT minting frenzy). From epoch 310 onward the population collapsed faster than volume: 101K submitters at epoch 384, 58K at epoch 500, 31,176 at epoch 627. Transaction volume fell only 92% over the same window — a population one twenty-fifth of its peak still sustains three quarters of the per-epoch transaction rate seen during 2023–2024.

Breadth is collapsing while per-actor intensity is rising — the same shrinking core just transacts more often. The address-to-transaction ratio fell from 0.88 (epoch 210) to 0.26 (epoch 627), and tx-per-submitter rose from ~2.0 (epoch 304) to ~3.8 (epoch 627). Cumulative Shelley-era throughput totals 118.07M transactions and 37.85M ADA in fees. The growth-trajectory signal is unambiguous: new addresses are not entering the fee-paying population at a rate that would sustain breadth — the same shrinking core is just transacting more often.

Same shrinking core, more active per-member

CEN.O9

Observation 09 · 2 findings

Two submitter sub-populations coexist: a stakeable head-count majority and a small non-stakeable minority that pays a third of the fees

2 findings

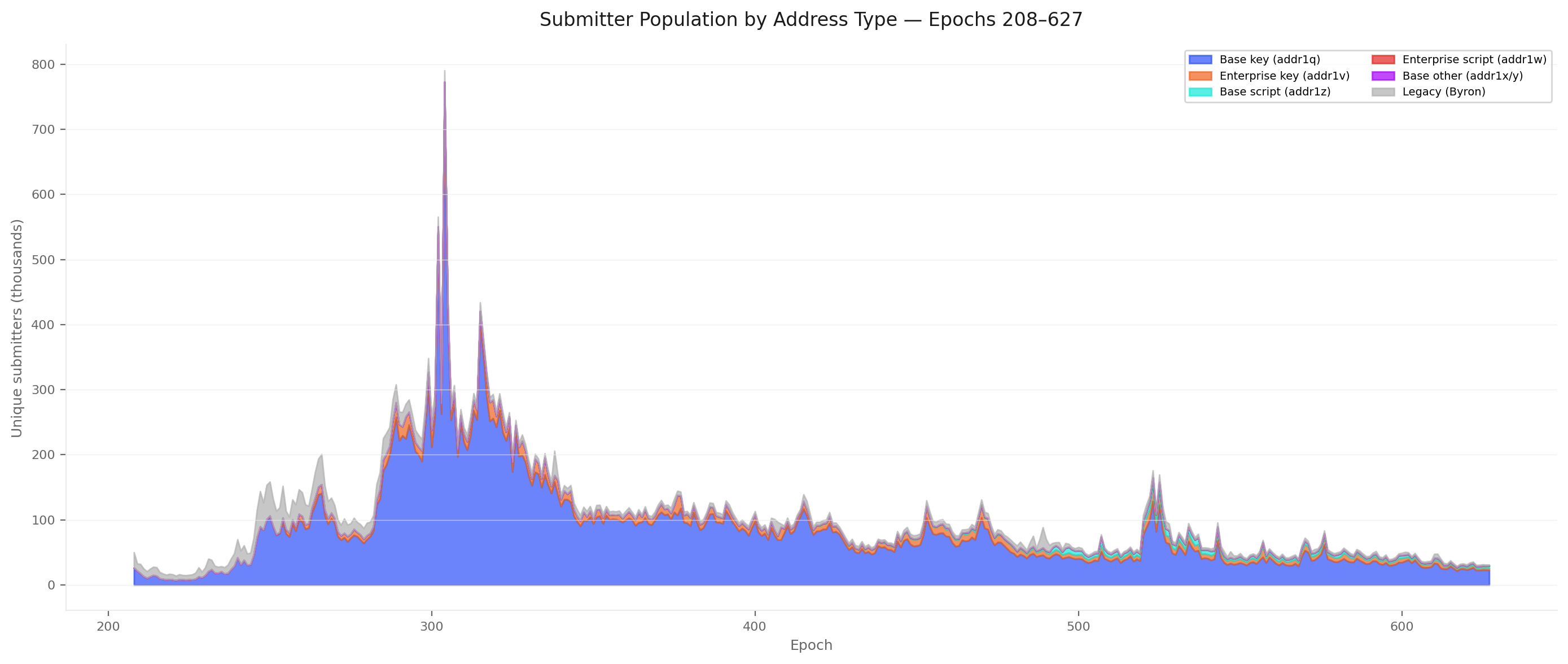

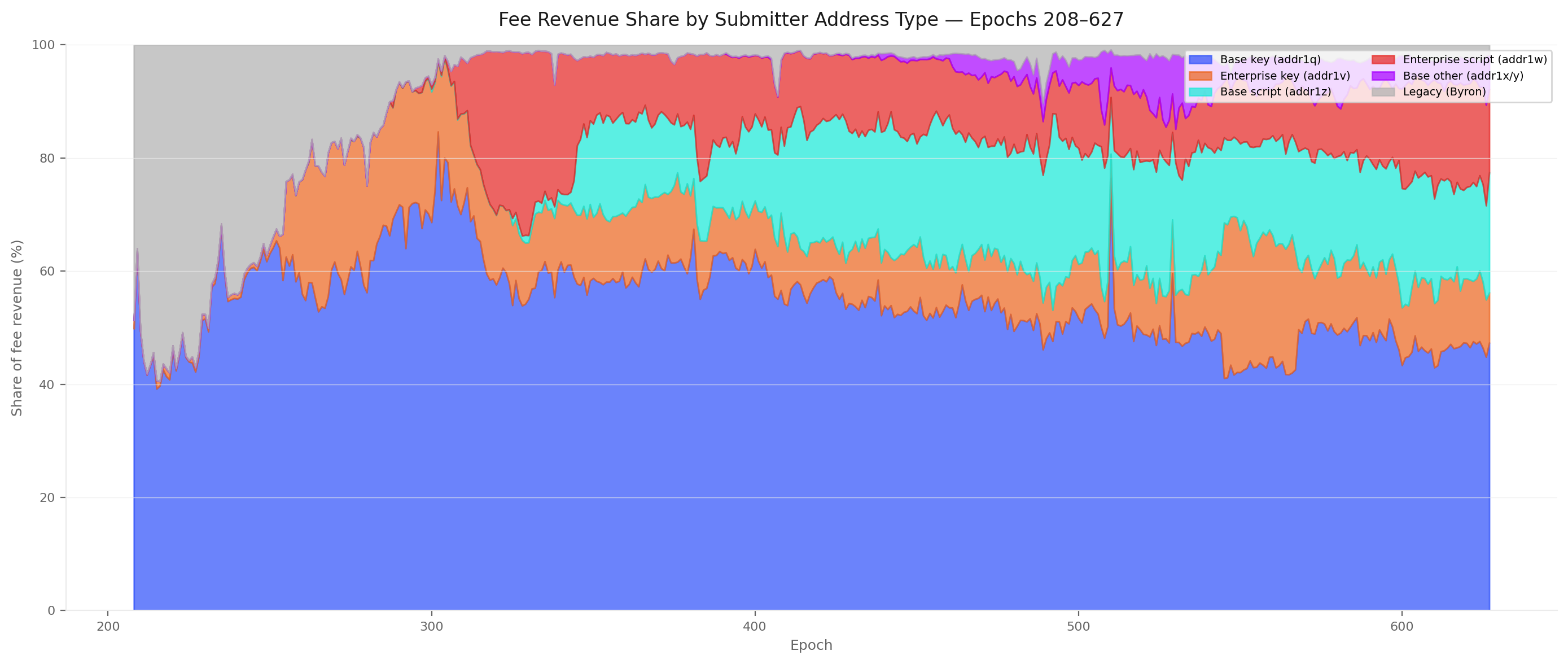

At epoch 627, the stakeable majority — base-key (addr1q) addresses carrying a stake credential — is 73.3% of submitter head-count and pays 47.4% of fees. The non-stakeable minority — enterprise (addr1v, addr1w) and legacy Byron addresses that structurally cannot delegate — is only ~16% of head-count but generates 30.1% of fee revenue (averaged 622–627), and that share has not fallen below 14% since the Alonzo era. The reward pipeline taxes a sub-population it cannot reward.

By address count, the submitter population remains overwhelmingly stakeable — but the script segment has grown structurally. At epoch 627: 73.3% base-key (addr1q) addresses carrying a stake credential, 10.8% base-script (addr1z), 9.2% enterprise-key (addr1v), 4.9% legacy Byron, 1.6% enterprise-script (addr1w), 0.2% base-other. Compared to the earlier snapshot at epoch 384 (87% base-key, <1% script), the shift is clear — base-key dropped 14 pp while base-script grew from 0.4% to 10.8%. The count-based picture remains misleading: the small script population punches far above its weight in fee terms.

Roughly 30% of fee revenue is generated by addresses that structurally cannot delegate, and this share has been stable since Alonzo. Over the recent 6-epoch window (622–627): enterprise-script (addr1w) 17.0%, enterprise-key (addr1v) 10.8%, legacy Byron 2.3% — totalling 30.1%. The non-stakeable fee share has oscillated between 18% and 44% since epoch 300, averaging ~25%; the structural floor is set by DeFi contract activity, the ceiling by speculative episodes. At no point since Alonzo has it fallen below 14% — the reward mechanism taxes a constituency it excludes.

The fee base is structurally misaligned with the reward base

CEN.O10

Observation 10 · 2 findings

A small DeFi-script sub-population — ~3,800 contracts at epoch 627 — generates a third of the fee base

2 findings

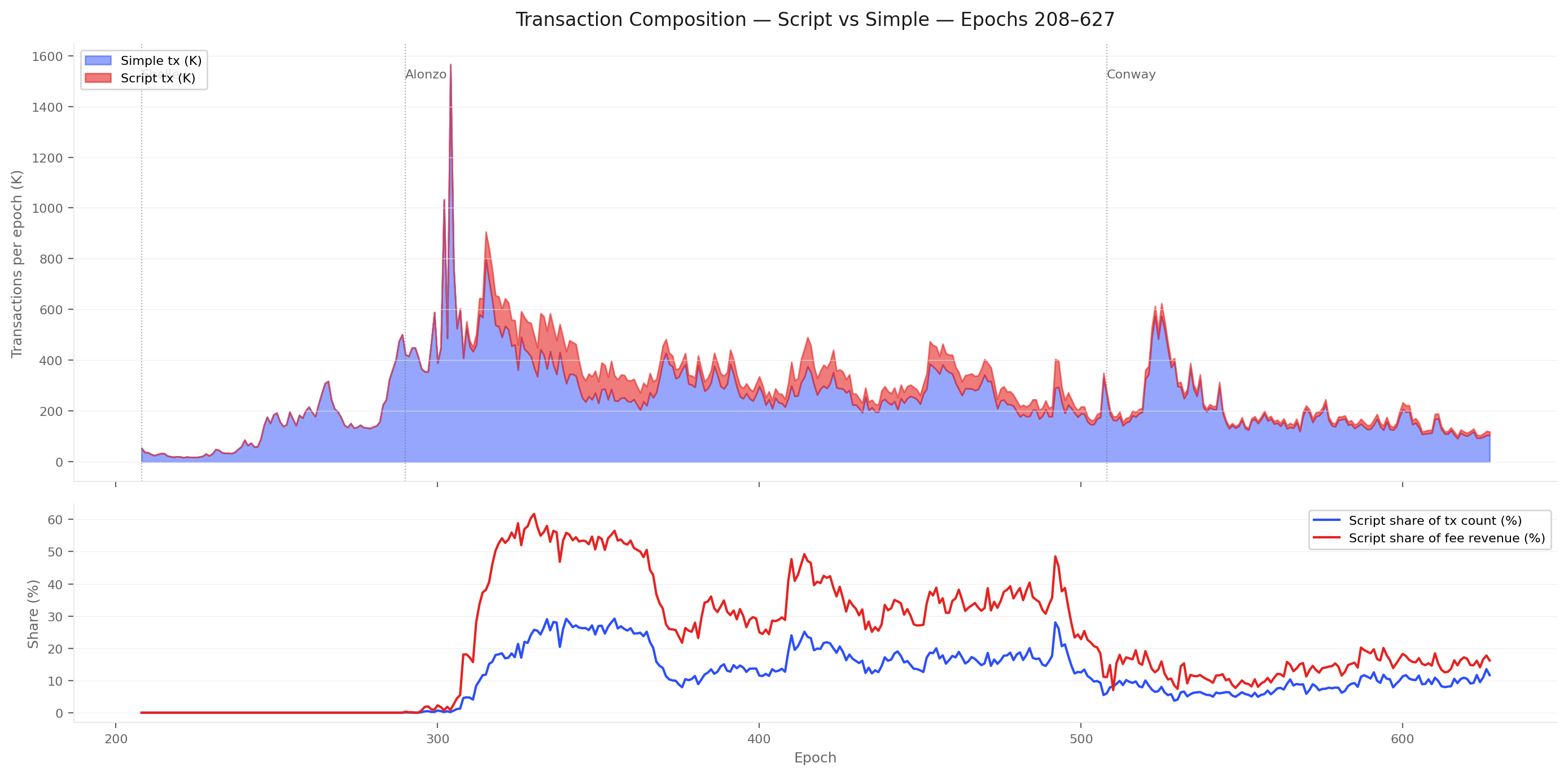

The script-using sub-population — base-script (addr1z) and enterprise-script (addr1w) addresses — is 3,851 actors at epoch 627 (12.4% of submitters) and generates 36.0% of epoch fees. Across the full post-Alonzo era it represents 12.5% of transaction count but 29.6% of cumulative fees. The per-address fee rate of an enterprise-script submitter (12.1 ADA/epoch) is 14× that of a base-key submitter (0.83 ADA/epoch). The chain's fee floor is supported by a population of roughly 3,800 smart contracts — a population dimension the current incentive design does not address.

Script transactions are 12.5% of post-Alonzo count but 29.6% of cumulative fees — the DeFi economy pays a 2.4× per-transaction premium. The premium peaked above 3× during the Alonzo era (epochs 310–340), when fewer than 30% of transactions commanded over 60% of fees. It has moderated to ~1.5× in recent epochs but remains structurally above parity. For the sustainability argument, this means per-transaction fee intensity is coupled to script adoption — a variable the current incentive design does not address.

At epoch 627, ~3,800 script addresses (12% of submitters) generate 36% of fee revenue — the pipeline depends on the continued operation of these contracts. Specifically: 490 enterprise-script + 3,361 base-script = 3,851 actors (12.4% of the submitter population) generated 14,481 ADA in fees — 36.0% of the epoch total. The per-address rate of an enterprise-script submitter (12.1 ADA/epoch) is 14× that of a base-key submitter (0.83 ADA/epoch). The script population grew sixteen-fold since epoch 384 (0.7% → 12.4%) while their fee share held steady around one third — the per-address premium has moderated but the structural dependency has deepened.

Concentration on script activity

CEN.O11

Observation 11 · 2 findings

The fee-paying population is bimodal: a heavy-paying core of a few hundred high-frequency actors and a long tail of ~147K small contributors

2 findings

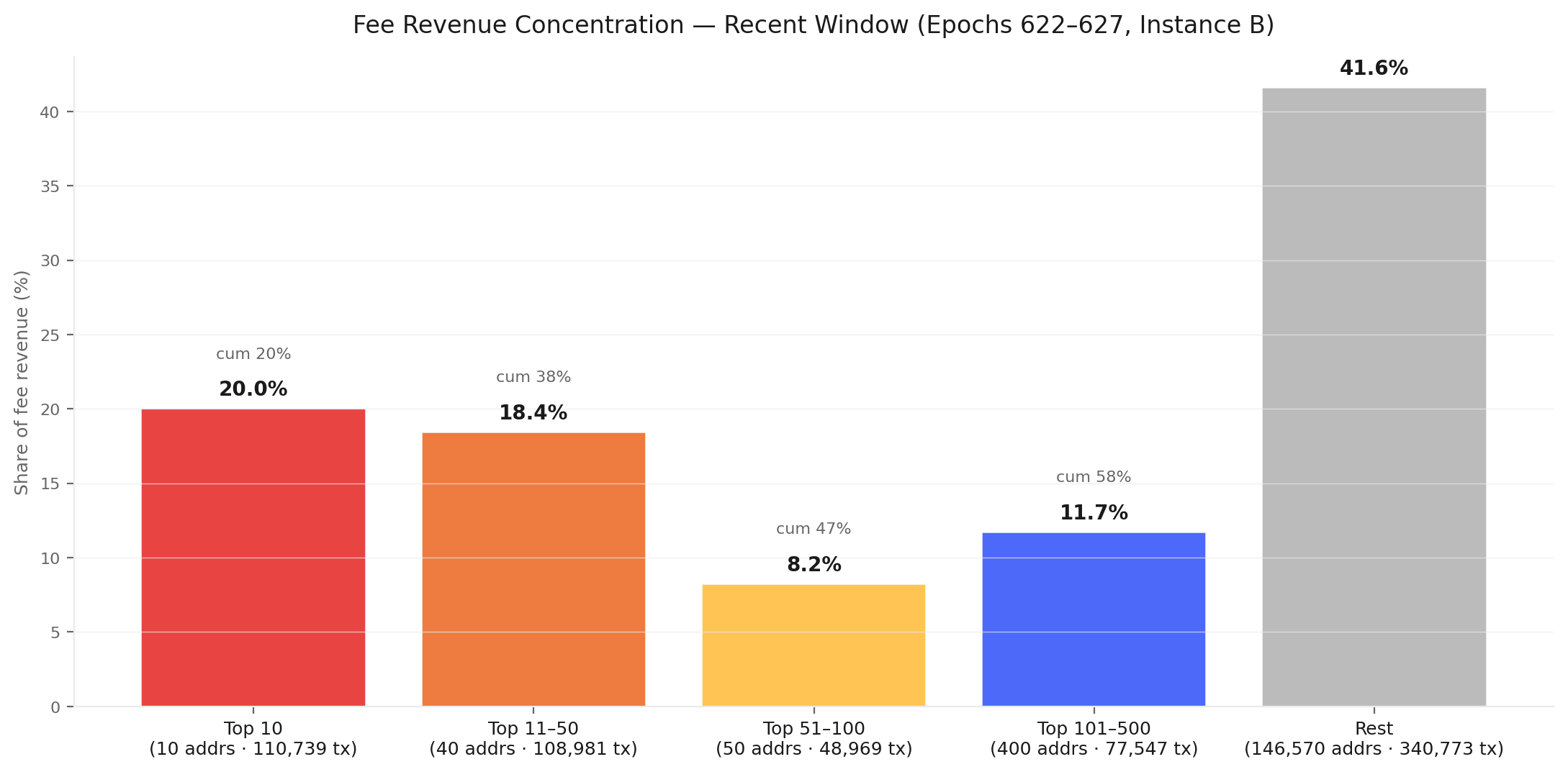

Over epochs 622–627, the top 10 addresses generate 20.0% of fees and the top 500 generate 58.4% — out of ~147K active submitters. The heavy-paying core is recognisable: a MinSwap DEX-script address leads, followed by addresses tied to the NUFI, TITAN, BERRY, and OYSTR pools and several enterprise-script DEX contracts and bot wallets. The concentration is heavy-tailed but below the delegation Gini of 0.976. 500 addresses out of 147K (0.34%) pay the majority of fees — the fee floor depends on a sub-population small enough to know by name.

The top 10 addresses pay 20% of all fees; the top 500 (out of ~147K) pay 58%. Over epochs 622–627, 500 addresses out of ~147K (0.34%) pay the majority of fees. Concentration is heavy-tailed but less extreme than delegation stake (Gini 0.976). Compared to the prior 618–623 window (top-10 = 24.3%, top-500 = 60.8%), the recent window shows a mild de-concentration of 4 pp at the top — driven by a single very-high-volume address whose activity tapered. The fee base sits on a few hundred high-frequency automated actors, not a diffuse retail tail.

High-frequency automated actors (DEX aggregators, exchange hot wallets, arbitrage bots)

The top 10 fee payers ran 110,739 transactions over 6 epochs (16.1% of volume) — fee-pot stability hinges on a population small enough to know by name. The top 50 ran 219,720 transactions (32.0%) over the same 6-epoch window. The top fee payers are dominated by recognisable archetypes: a MinSwap DEX-script address leads at 12,105 ADA over 6 epochs; pools tied to NUFI (NuFi exchange-style operator), TITAN, BERRY, and OYSTR appear among the top 10 alongside enterprise-script DEX contracts and bot wallets. The fee floor of the network depends on a population of ~10 actors whose churn risk is not modelled by any incentive parameter.

Single-actor exposure

CEN.O12

Observation 12 · 3 findings

The fee-paying population and the delegator population barely overlap — funders and beneficiaries are largely different people

3 findings

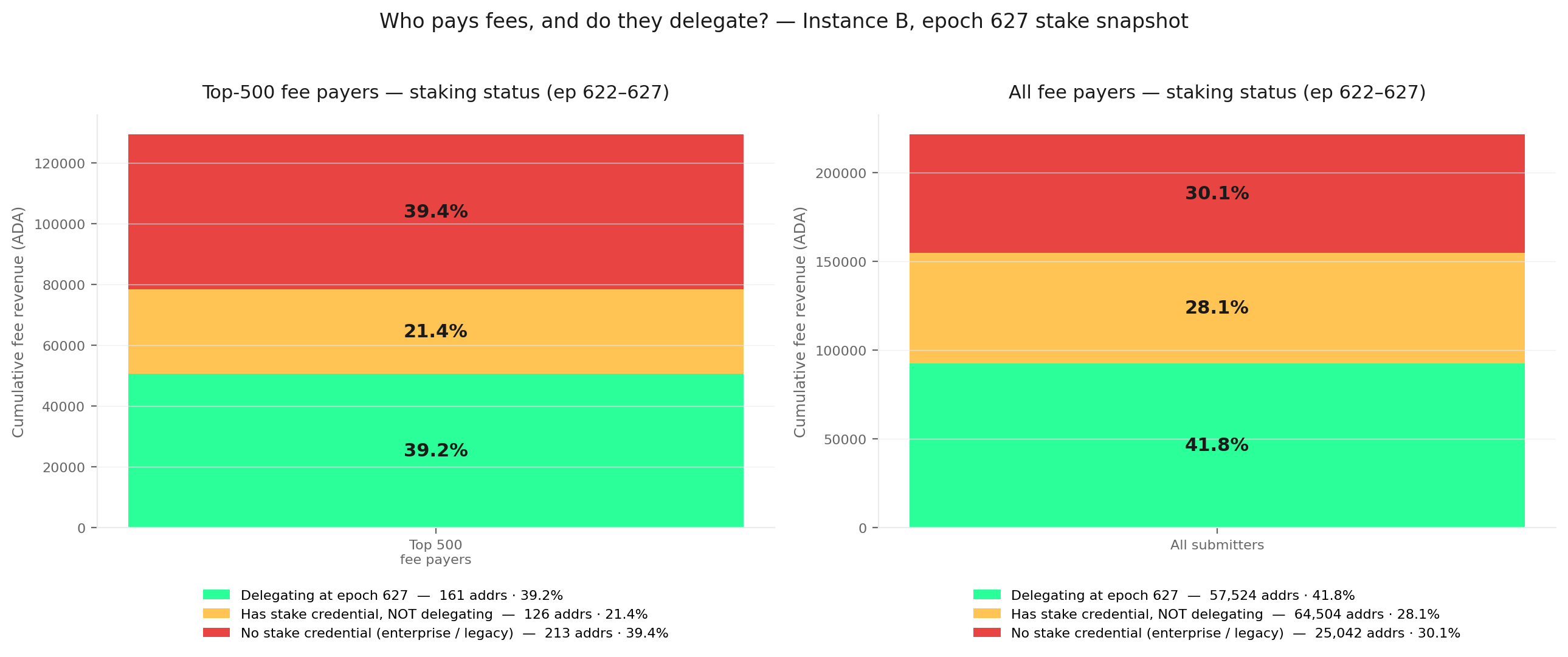

Joining the submitter set (~147K addresses, epochs 622–627) to the 1,352,113 active delegators at epoch 627 reveals the population gap: only 41.8% of fee revenue comes from currently-delegating addresses; 28.1% from base addresses whose stake credential is not in the delegation set; 30.1% from addresses with no stake credential. From the delegator side, only 3.1% of the 1.352M delegators submit any transaction in a 6-epoch window. Fewer than 4 ADA in every 10 ADA of fees flow back to the population that paid them through any reward channel.

Only 41.8% of fee revenue comes from currently-delegating addresses; the remaining 58.2% comes from addresses outside the delegation set at the snapshot epoch. Across epochs 622–627, the 1.352M delegators at epoch 627 contributed 41.8% of fee revenue (92,538 ADA out of 221,565). The stakeable-but-inactive segment (base addresses whose stake credentials are not in the delegation set) contributed 28.1% (62,340 ADA). The structurally non-stakeable segment (enterprise + legacy) contributed 30.1% (66,684 ADA). The mismatch is symmetric on both sides — the funding base does not match the reward base.

Only 3.1% of delegators submit any transaction in a 6-epoch window — 96.9% of delegators are passive holders. Of the 1,352,113 active delegators at epoch 627, only 42,082 appear as the first input of any transaction during epochs 622–627 (a 30-day window). The remaining 1,310,031 (96.9%) hold stake, accrue rewards, and never touch the chain. From the other side, the submitter base has 76,561 unique stake credentials over the same window, of which 42,082 (55.0%) are in the delegation set — the rest carry a stake credential that has never been delegated, has been deregistered, or sits idle.

Delegators are passive; submitters are a different population

In the top 500 fee-paying addresses, the largest segment by fee weight is the population the reward mechanism cannot reach. Top-500 split: no-stake-cred 39.4% (213 addresses, 50,960 ADA), delegating 39.2% (161 addresses, 50,685 ADA), has-cred-not-delegating 21.4% (126 addresses, 27,728 ADA). The pipeline's largest fee contributors are concentrated in the population it cannot reward — half of the heavy-paying actors are structurally outside the delegation game by design (DEX scripts, exchange enterprise wallets), and another fifth are technically inside but have opted out. Any fee-redistribution mechanism that passes value through the delegation channel returns less than 40 ADA in every 100 ADA of fees to the population that paid them.

Heavy-paying actors are concentrated outside the delegation channel

2. The ADA Supply

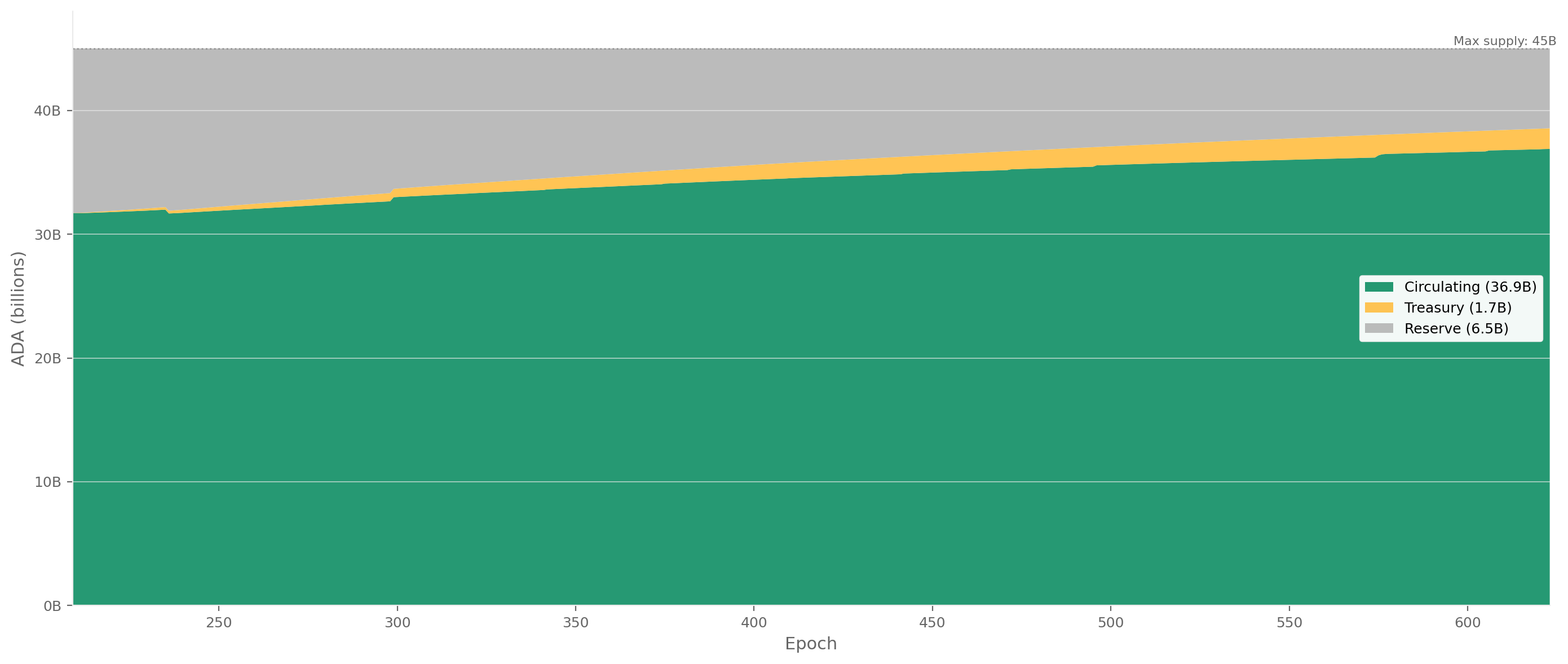

The Cardano monetary policy fixes the maximum supply at 45 billion ADA.

At epoch 623, the circulating supply has reached 36.88B, with 6.45B remaining in the reserve and 1.66B accumulated in the treasury. Monetary expansion — the rate at which reserve ADA enters circulation — decays geometrically.

FigureCEN.2.1ADA supply decomposition into circulating, reserve, and treasury across the Shelley era. At epoch 623, circulating supply has reached 36.88B of the 45B ADA maximum, with 6.45B remaining in the reserve and 1.66B accumulated in the treasury under geometric monetary expansion.

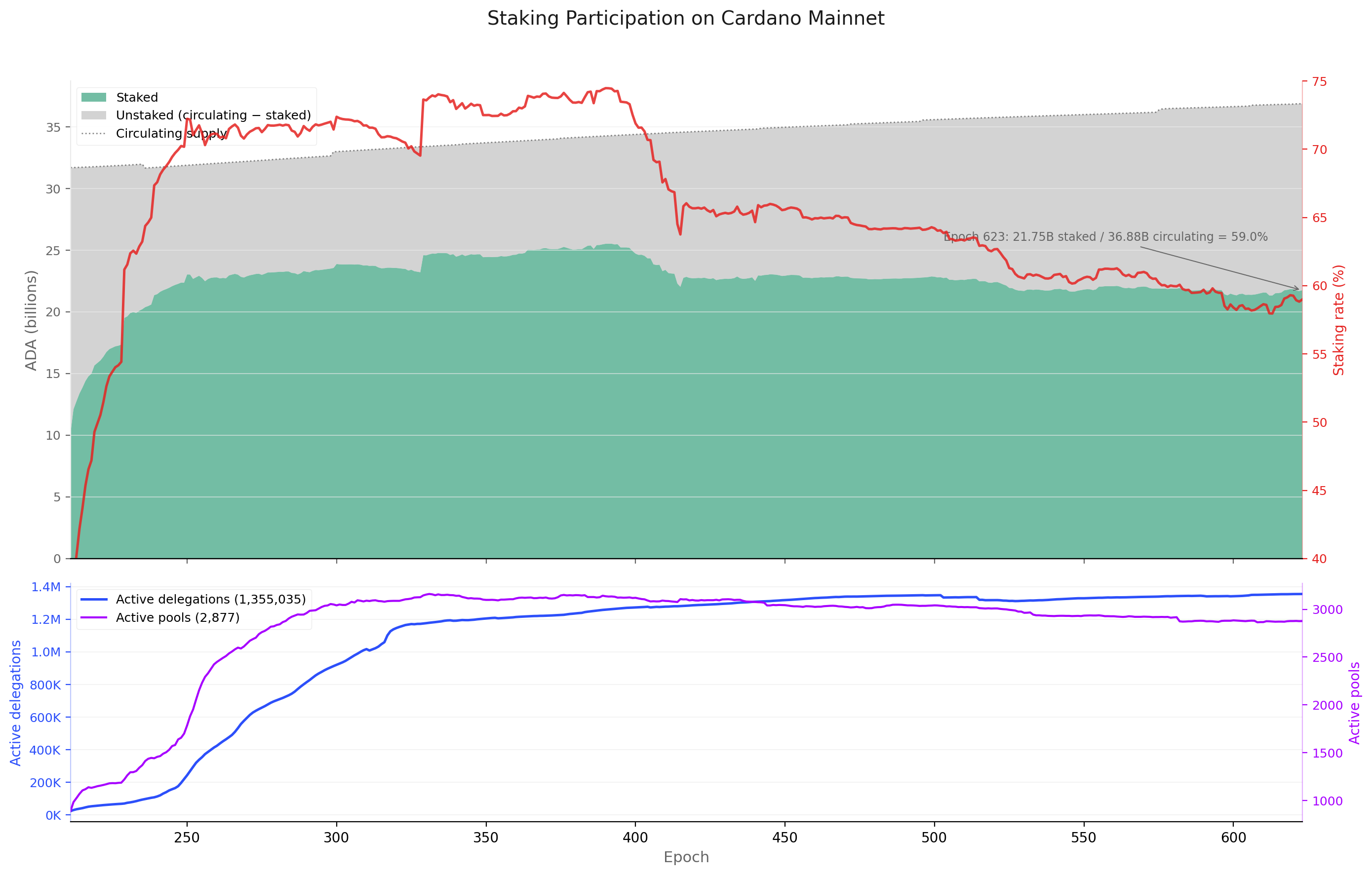

At epoch 623: 21.755B ADA staked out of 36.110B circulating = 60.2% staking rate. The remaining 14.355B ADA (39.8%) is not staked.

Of this, only 134.6M (0.37%) has a registered stake credential without delegation — the addressable non-participant pool. The remaining 14.2B sits in addresses with no stake credential at all. This population is decomposed in §5.

FigureCEN.2.2Staked versus unstaked decomposition of circulating supply with the staking rate (red, right axis). The rate peaked near 71% around epoch 260 and has drifted to 59% at epoch 623 — driven by circulating supply growth outpacing new stake inflows.

The top panel shows the staked/unstaked decomposition of circulating supply with the staking rate (red line, right axis). The rate peaked near 71% around epoch 260 and has been declining gently, driven by circulating supply growth outpacing new stake inflows.

FromObservationCEN.O7 — The non-participant population is 39.8 % of the supply, structurally inert, and held by a tightly-concentrated minority of custodians and legacy holders

Finding#1→ The staking rate is structurally declining despite persistent net delegator inflows. The rate has fallen from 71% (epoch ~260) to 59% (epoch 623) — a 12 pp loss over ~360 epochs. The decline is driven entirely by supply-side expansion: circulating ADA grew from ~32B to ~37B while staked ADA grew from ~23B to ~22B. The non-participant pool is growing faster than the staking pool.

3. Pool Operators

3.1. What the raw db-sync shows — 5,919 pools, most of them empty

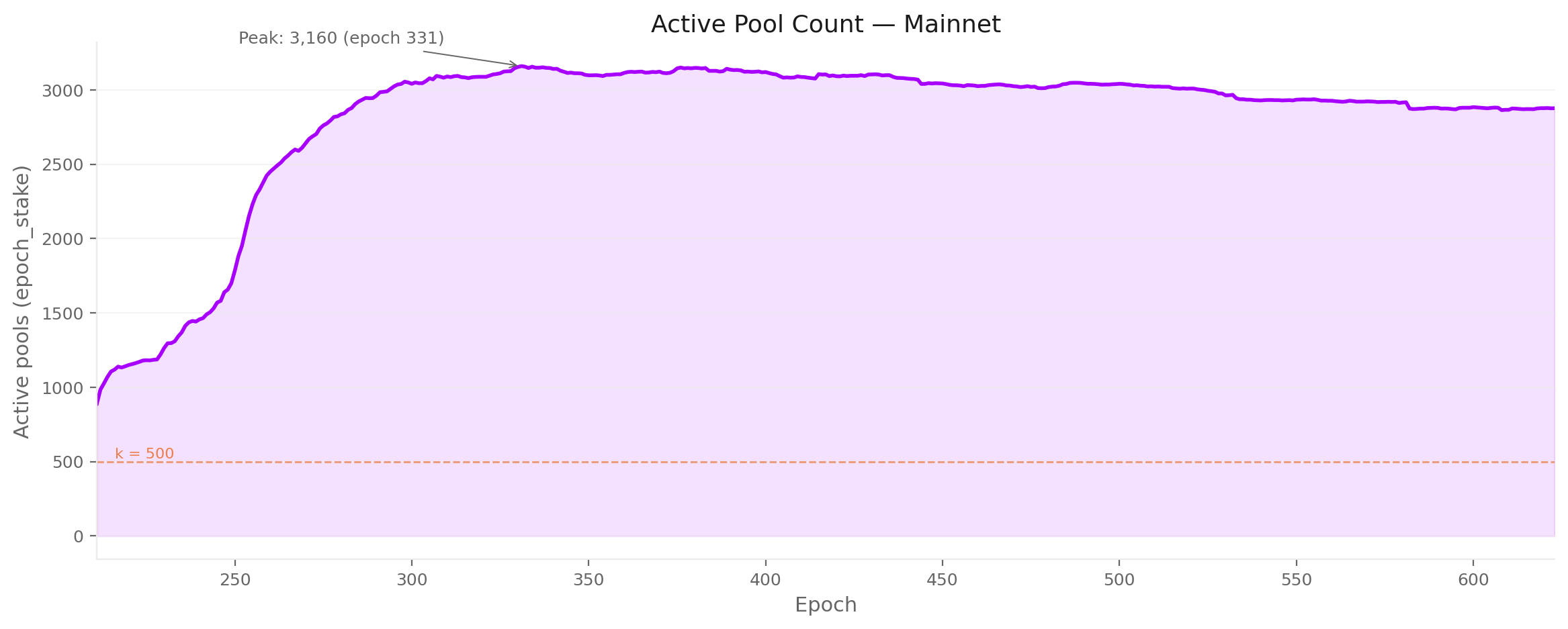

The pool count from epoch_stake peaked at 3,160 (epoch 331) and currently stands at 2,877.

This counts only pools that appear in the staking snapshot with non-zero delegated stake — the registration-certificate count of 5,919 includes 3,042 empty pools and is discarded (see §3.2 — the production-threshold cut for the full rationale).

FigureCEN.3.1Productive pool count from epoch_stake against the k = 500 target across the Shelley era. The cleaned count peaked at 3,160 (epoch 331) and currently stands at 2,877 — discarding the 3,042 empty pools and 2,877 idle registrations that inflate the raw certificate-based count.

The k=500 reference line shows the protocol's target number of pools (the saturation parameter). The actual pool count has been ~5.8× k since epoch 330, though many of these pools carry negligible stake.

3.2. Three quarters of pools earn no blocks — the production threshold cut

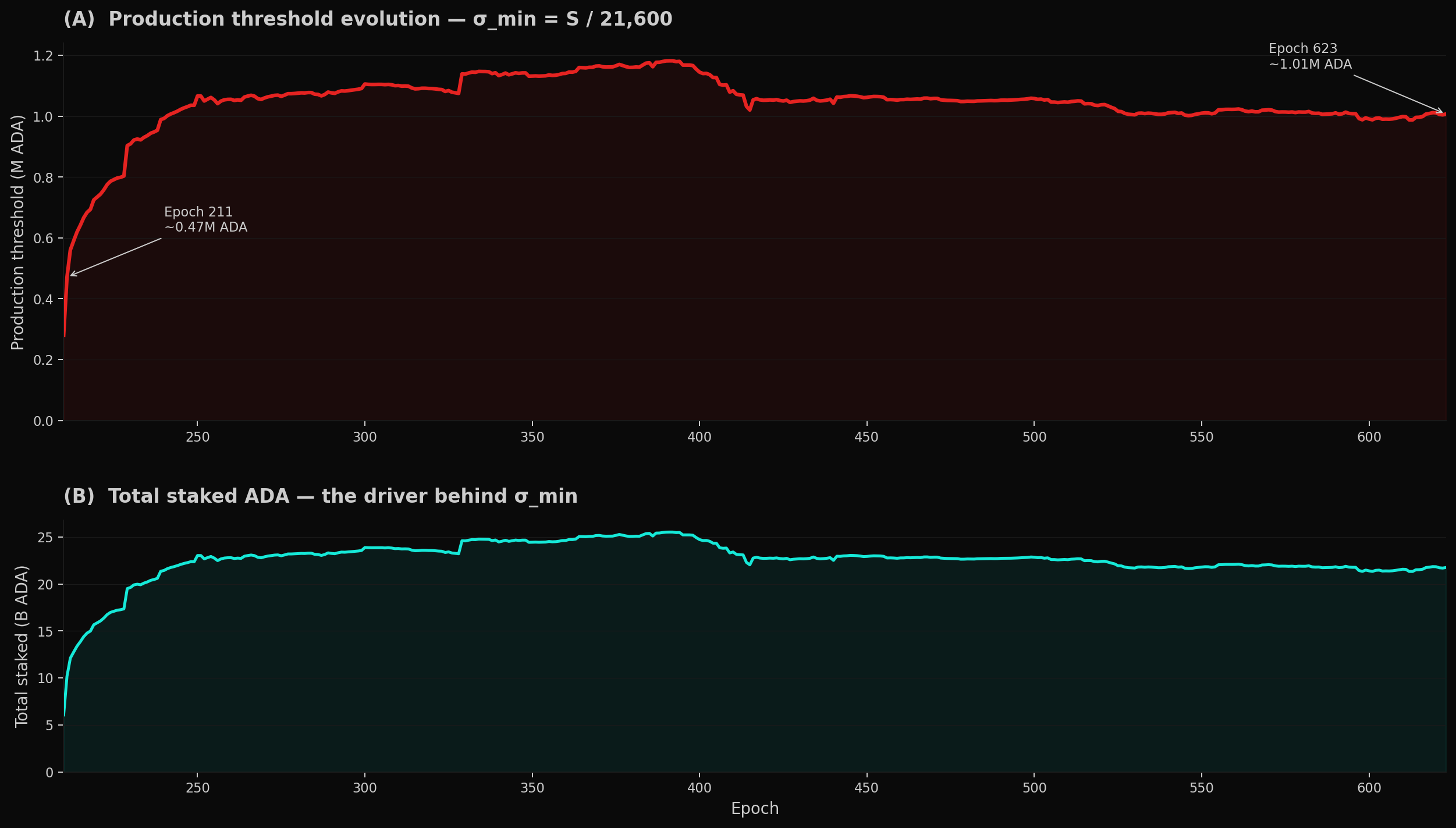

Block production on Cardano is a lottery: each slot, a pool is selected to produce a block with probability proportional to its share of total staked ADA.

With ~21,600 slots per epoch, a pool holding stake σ out of a total S expects to be elected for λ = 21,600 × σ / S blocks per epoch. The number of blocks actually produced follows a Poisson distribution with parameter λ.

A pool that expects fewer than one block per epoch (λ < 1) is unreliable to the consensus protocol. But even at λ = 1, Poisson variance is severe — there is a 37% chance the pool produces zero blocks in a given epoch ($P(\text{zero}) = e^{-\lambda}$), so the operator and delegators face a swingy yield. The cleaner threshold is the stake level at which the pool produces ≥1 block in an epoch with 95% probability — which requires λ ≥ 3 (since \$1 - e^{-3} = 0.95$).

The production threshold therefore corresponds to λ = 3: $\sigma_{\min} = 3 \times S / 21{,}600$. This is a structural property of the protocol — it follows directly from the number of slots per epoch and the total staked ADA, not from any tuneable incentive parameter. (See POL.O3.F1 in the companion Pools Pot Distribution report for the full derivation.)

Because $\sigma_{\min}$ scales linearly with S, the threshold rises as staking participation grows. At epoch 211 (Shelley launch, S ≈ 10B ADA), $\sigma_{\min}$ ≈ 1.4M ADA. By epoch 623 (S ≈ 21.75B ADA), it sits at ~3M ADA.

If total staked ADA continues to increase — whether through higher participation or circulating-supply growth — the threshold will continue to rise, pushing the minimum reliable pool size upward over time.

FigureCEN.3.2Production threshold $\sigma_{\min} = 3S/21{,}600$ across the Shelley era. The threshold first crossed 3M ADA in the early Shelley window once staking participation rose, peaked at ~3.5M ADA at epoch 391 (when total staked ADA reached 25.5B), and currently sits at ~3.0M ADA — a structural property of the slot count, not an incentive parameter.

The threshold is bounded by the total ADA supply. With a maximum supply of 45B ADA, even 100% staking participation would place $\sigma_{\min}$ at ~5–6M ADA at full dilution.

At the current staking rate of ~60%, $\sigma_{\min}$ sits at roughly 3M ADA and will rise or fall only if total staked ADA changes.

Segment

Pools

Share of pools

Stake

Share of stake

Delegations

Above threshold (≥3M ADA — productive)

733

25.5%

21.18B

97.4%

1,227,281 (90.6%)

Sub-reliable tail (1M–3M ADA)

219

7.6%

0.39B

1.8%

67,817 (5.0%)

Sub-block tail (< 1M ADA)

1,925

66.9%

0.19B

0.9%

59,937 (4.4%)

Roughly three quarters of all pools sit below the production threshold. Together they hold less than 3% of staked ADA. Their 127,754 delegators collectively control ~580M ADA — a small share that earns intermittent and unpredictable rewards.

Below-threshold pool breakdown by stake:

Tier

Pools

Stake

Sub-block (< 1M ADA)

1,925

0.19B

— < 1K ADA

778

0.1M

— 1K–10K

394

1.4M

— 10K–100K

323

12.4M

— 100K–500K

286

69.0M

— 500K–1M

144

104.3M

Sub-reliable (1M–3M ADA)

219

0.39B

The median sub-block pool holds just 2,547 ADA; three quarters hold less than 68K ADA. The 219 sub-reliable pools (1M–3M) are block-producing in expectation but face Poisson variance too high to drive predictable returns.

After cleaning: the productive pool count drops from 2,877 to 733 — slightly above the protocol's $k = 500$ target.

FromObservationCEN.O1 — Multi-pool entities flourished (23 → 85 entities, 65% → 76% of productive stake) while single-pool operators struggle (555 → 291 pools, 39% → 24% of stake)

Finding#1→ Three quarters of registered pools are economically irrelevant. 2,144 of 2,877 (75%) sit below the production threshold (~3M ADA): 1,925 sub-block pools (< 1M) and 219 sub-reliable pools (1M–3M) together hold only 0.58B ADA — 2.7% of staked supply. The median sub-block pool holds 2,547 ADA, orders of magnitude below the threshold — these are addresses on the registry, not infrastructure operating in production.

3.3. Behind the pools — 4 entities on-chain become 85 with off-chain attribution

The 733 productive pools are not 733 single-pool operators. Many pools share a controlling entity — detectable on-chain through shared pool_owner keys, and off-chain through metadata, ticker naming patterns, relay DNS, reward addresses, and public disclosures.

This cleaning pass groups pools by entity to reveal the true operator landscape.

Two layers of attribution.

Layer

Signal

Result on the productive set

On-chain only

Shared pool_owner keys across productive pools

4 entities sharing keys across 8 pools; 943 pools appear as single-pool operators. On-chain keys are a lower bound — most multi-pool operators use separate keys per pool, so this layer alone misses the bulk of fleets.

Off-chain layered heuristics

Public brand declarations (tickers, metadata URLs, websites), relay/metadata clustering (shared IPs, identical hashes, co-located infrastructure), on-chain ownership clusters, and manual resolution from community databases

Across all registered pools: 85 named entities controlling 660 pools. Combining the two layers is what catches the off-chain fleet structure that on-chain keys alone don't expose.

FromObservationCEN.O1 — Multi-pool entities flourished (23 → 85 entities, 65% → 76% of productive stake) while single-pool operators struggle (555 → 291 pools, 39% → 24% of stake)

Finding#9→ On-chain attribution alone misses the bulk of fleet structure — 4 entities vs 85, a ~20× jump. The on-chain layer reveals 4 entities sharing keys across 8 pools; everything else appears as single-pool operators. Most multi-pool operators use separate keys per pool, so on-chain ownership clustering catches only the small minority that doesn't separate keys. Any analysis that stops at the on-chain layer treats fleet pools as if they were single-pool operators and materially understates network concentration. The combined-attribution numbers — 85 entities across the registered set, 83 in the productive set — are the foundational inputs for every entity-level claim downstream.

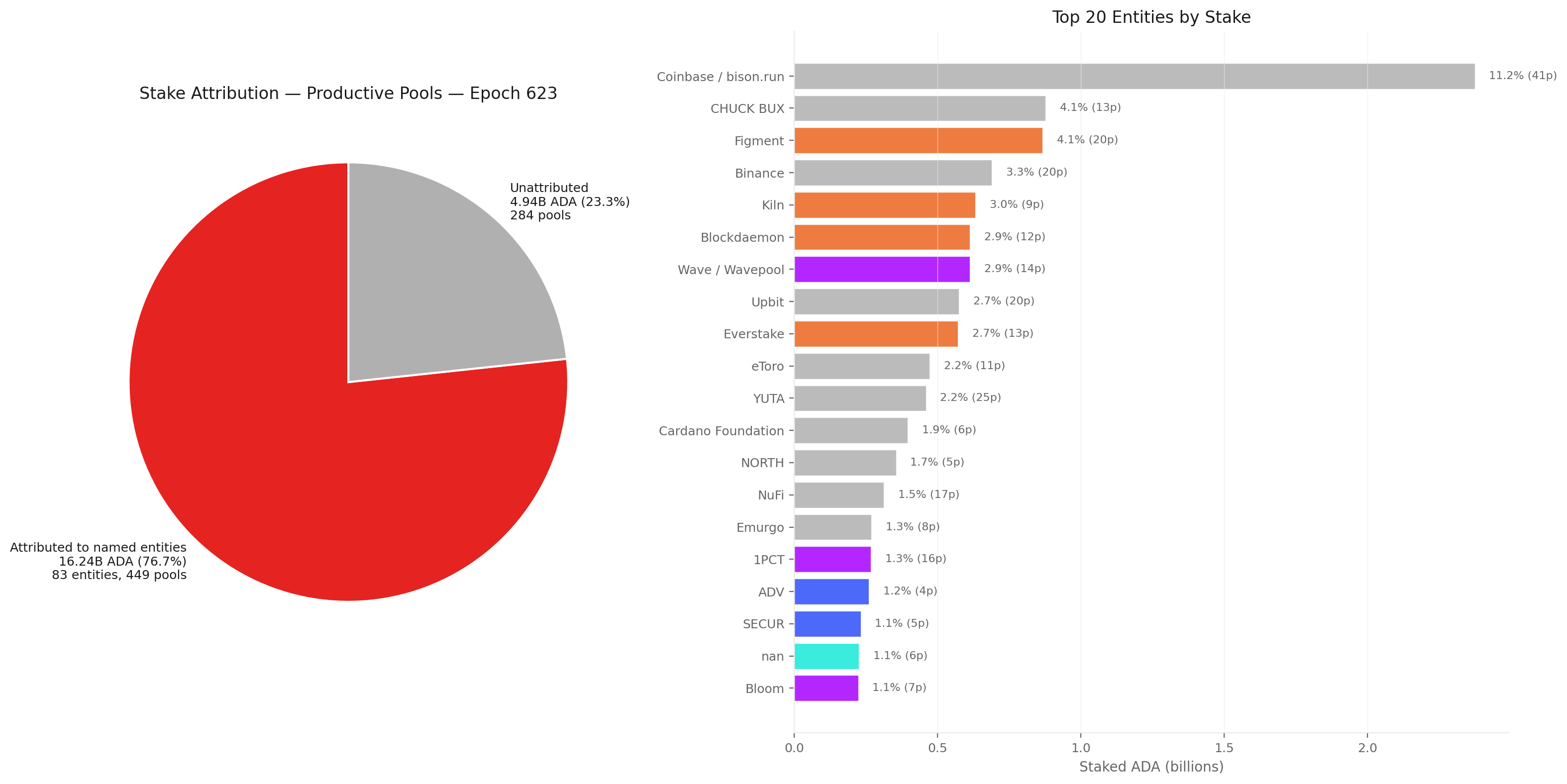

Filtering to the 733 productive pools. From the 85 named entities, 2 disappear entirely (RAID — 7 pools, RockX — 10 pools, all below threshold), and 10 shrink to a single productive pool (reclassified as attributed single-pool operators), leaving 83 attributed entities controlling 449 productive pools (16.24B ADA, 76.7% of productive stake). The remaining 284 productive pools (4.94B ADA, 23.3%) are unattributed single-pool operators.

Segment

Pools

Stake

Share of productive stake

Attributed to named entities

449

16.24B ADA

76.7%

Unattributed (single-pool operators)

284

4.94B ADA

23.3%

The productive landscape splits almost evenly by pool count but is heavily skewed by stake: attributed entities control three quarters of productive stake through half the pools.

FromObservationCEN.O1 — Multi-pool entities flourished (23 → 85 entities, 65% → 76% of productive stake) while single-pool operators struggle (555 → 291 pools, 39% → 24% of stake)

Finding#2→ Three quarters of productive stake sits in 83 named entities. They control 76.7% through 449 productive pools (71 strict multi-pool fleets + 12 attributed single-pool operators). The 284 unattributed single-pool operators are the numerical majority but hold only 23.3% of productive stake. The 83-entity count is a lower bound — operators running entirely separate infrastructure per pool stay invisible to the attribution pipeline.

FigureCEN.3.3Productive-pool stake split between attributed entities and unattributed single-pool operators at epoch 623. 83 attributed entities control 449 productive pools (76.7% of productive stake) through half the pools; 284 unattributed single-pool operators are the numerical majority but hold only a quarter.

3.4. The productive operator landscape — 733 pools, 367 entities, 21.18B ADA at stake

All figures and tables in this section refer to productive pools only — the 733 pools above the production threshold at epoch 623, carrying 97.4% of staked ADA. The 1,925 sub-threshold pools (0.9% of stake) are excluded.

3.4.1. The headline picture at epoch 623

n-MPO is counted on productive pools only. An entity is strict multi-pool when it controls ≥ 2 productive pools (≥ 3M ADA each). An entity that owns several pools but has only one productive pool — even if its nominal fleet is large — is classified as an attributed single-pool operator, because the rest of the fleet sits below the production threshold and is economically inactive. This split is what gives 71 + 12 = 83 attributed entities, not 83 multi-pool operators.

Segment

Entities

Pools

Stake

Share

Productive total

367

733

21.18B

100%

of which:

Identified entities

83

449

16.24B

76.7%

— strict multi-pool (n-MPO ≥ 2 productive pools)

71

437

15.69B

74.1%

— attributed single-pool (n-MPO = 1, even when more pools are owned but sub-threshold)

12

12

0.55B

2.6%

Unattributed single-pool operators

284

284

4.94B

23.3%

The 12 attributed single-pool entities collectively own 58 pools, but only 12 of those are productive; the remaining 46 sit below 3M ADA. The most extreme case is IOG itself: 34 owned pools at epoch 623, only 1 productive. These entities look like multi-pool fleets on paper but contribute only one productive pool each to the network, so they fall in the same productive-set bucket as a pure single-pool operator (see data/mpo_attributed_single_pool_detail.csv for the full list).

The entity attribution is a current-epoch snapshot and a lower bound — entities using entirely separate infrastructure and branding for each pool remain invisible. The real strict multi-pool count is certainly higher than 71 (and the attributed-entity total higher than 83).

3.4.2. The shape of the multi-pool fleet — 12 entities run 41% of the productive stake

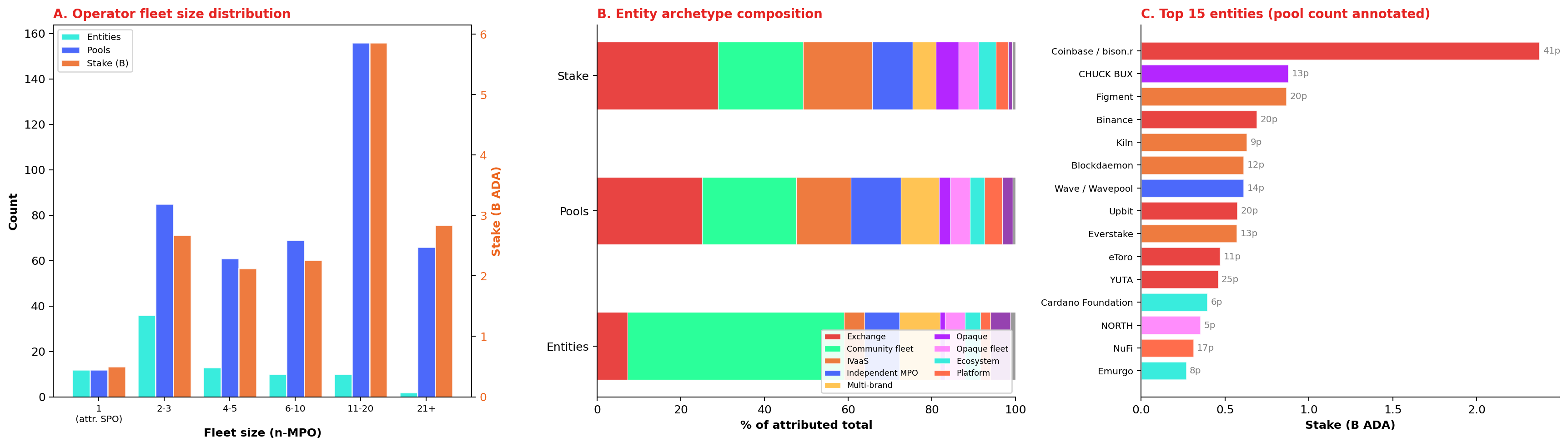

The 83 identified entities are now bucketed by n-MPO — the count of productive pools they control (not the count of pools they own on paper). On this basis, the productive set covers 449 pools spread across fleet sizes from 1 to 41.

FigureCEN.3.4Multi-pool operator fleet-size distribution and entity archetype composition at epoch 623, counted on productive pools only. Fleet size is heavy-tailed: 12 entities with 11+ productive pools control 41.0% of productive stake; CEX and IVaaS together — 10 entities — capture 45.4% of attributed stake at structurally zero pledge.

Fleet size distribution (panel A):

Fleet size (n-MPO, productive pools only)

Entities

Productive pools

Stake (B)

% of productive

1 (attributed single-pool operator)

12

12

0.50

2.4%

2–3

36

85

2.67

12.6%

4–5

13

61

2.12

10.0%

6–10

10

69

2.26

10.7%

11–20

10

156

5.86

27.7%

21+

2

66

2.83

13.4%

Total attributed

83

449

16.24

76.7%

The first row of the table covers the attributed single-pool operators: entities whose nominal fleet may be larger but whose productive footprint is exactly one pool. They are not strict multi-pool operators — even though some of them own dozens of pools — because the rest of those pools sit below the production threshold and produce no blocks. IOG itself sits in this bucket: 34 pools owned, 1 productive.

The 2–3 pool tier is the most populated (36 entities) but each tier above it controls more aggregate stake despite fewer entities.

Two entities alone — Coinbase (41 productive pools) and YUTA (25) — operate 66 productive pools and hold 2.83B ADA (13.4%) of productive stake. Binance, which would have placed a third entity in the 21+ tier under an "owned pools" count, sits in the 11–20 tier on a productive-pool count.

FromObservationCEN.O1 — Multi-pool entities flourished (23 → 85 entities, 65% → 76% of productive stake) while single-pool operators struggle (555 → 291 pools, 39% → 24% of stake)

Finding#4→ Concentration is heavy-tailed: 12 entities run 41% of productive stake. Counted on productive pools only, 12 entities with 11+ productive pools hold 8.69B / 21.18B = 41.0% of productive stake. The mid-range (2–10 productive pools, 59 entities) is the numerical majority but its aggregate weight (33.3%) is smaller than the concentrated top. Stake scales super-linearly with fleet size — a 21+ productive-pool entity holds on average 1.42B; a 2–3 productive-pool entity holds 0.07B.

Entity archetype composition (panel B). Exchanges (CEX: 6 entities, 119 pools, 4.71B) and institutional validators (IVaaS: 4 entities, 62 pools, 2.69B) together account for 10 entities but 45.4% of attributed stake.

Community-branded fleets (43 entities, 3.30B) are the most numerous archetype but hold less stake than the exchange tier alone. The remaining archetypes — independent MPOs, multi-brand fleets, opaque entities, ecosystem actors, and platforms — fill the long tail.

FromObservationCEN.O1 — Multi-pool entities flourished (23 → 85 entities, 65% → 76% of productive stake) while single-pool operators struggle (555 → 291 pools, 39% → 24% of stake)

Finding#5→ Custodial dominance sets a structural pledge floor. CEX + IVaaS together — 10 entities, 181 pools, 7.40B ADA, 34.3% of productive stake — operate at zero pledge by architectural constraint: their delegation source is custodied retail balances and institutional client assets, which cannot legally be pledged by the operator. Their dominance sets a floor on how much of the stake landscape is unreachable by pledge-based incentive mechanisms.

3.4.3. What the productive total looked like before the threshold cut

The production threshold — the stake at which a pool produces a block with 95% probability in a given epoch (λ ≥ 3) — rises mechanically with total staked ADA. At epoch 211 (Shelley launch, S ≈ 10B ADA), σ_min ≈ 1.4M ADA; by epoch 623 (S ≈ 21.75B ADA) it sits at ~3M ADA.

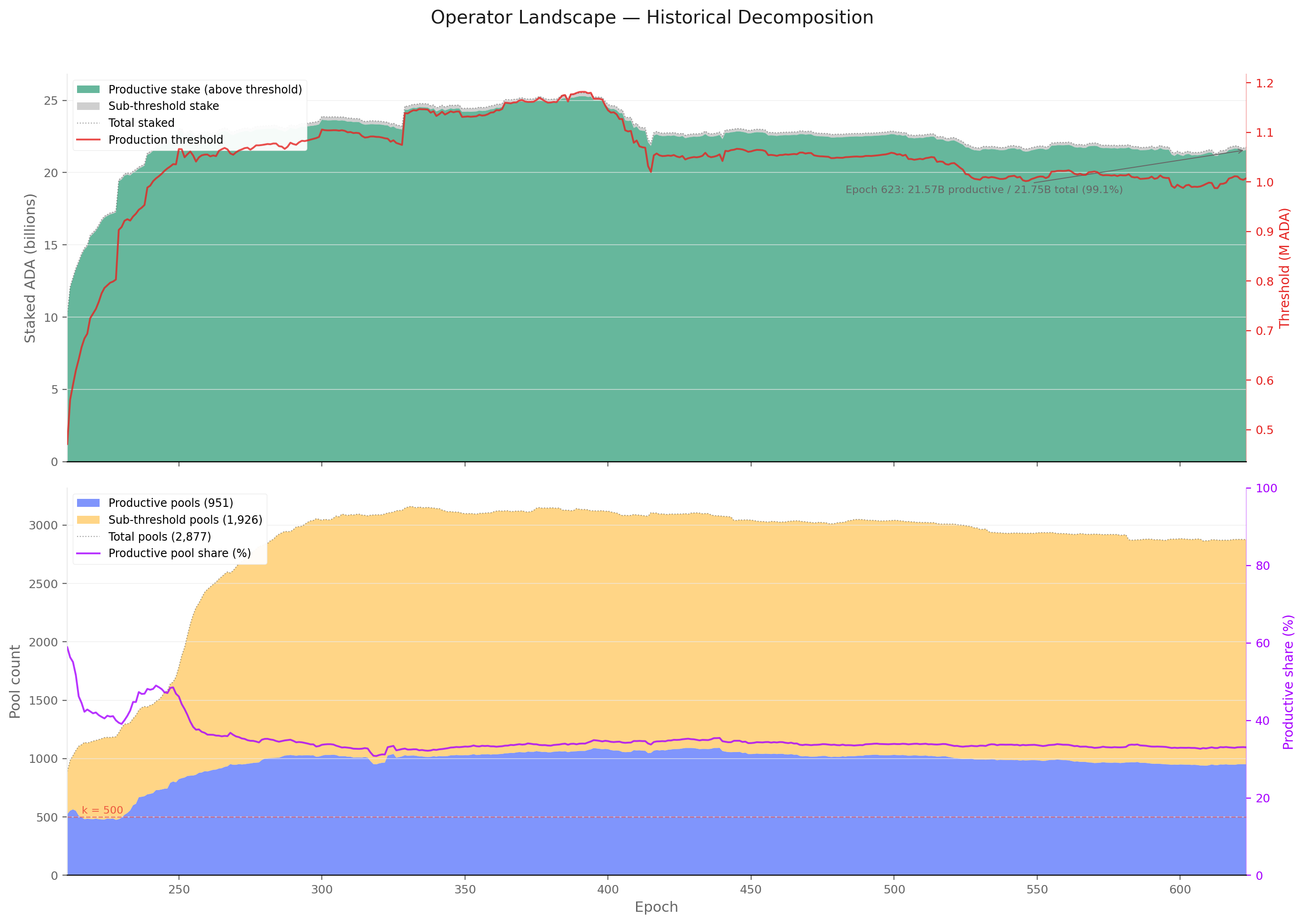

The number of pools clearing this rising threshold has remained remarkably stable in the 700–1,000 band since epoch 300 — historical figures use the time-varying threshold, while the canonical epoch-623 productive set is 733 pools. The sub-threshold tail grew from near zero to over 2,000 pools by epoch 330 and has hovered there since.

The productive share of pools has therefore fallen from near 100% in early Shelley to roughly 25% today — yet productive pools continue to control over 97% of staked ADA throughout the entire history.

FigureCEN.3.5Productive versus sub-threshold pools across the Shelley era — by stake (top) and pool count (bottom). The productive pool count has held at ~900–1,000 since epoch 300 while the sub-threshold tail grew to nearly 2,000; productive pools nonetheless retain over 99% of staked ADA throughout.

The top panel shows the staked-ADA split between productive and sub-threshold pools (left axis) alongside the production threshold itself (red line, right axis).

The bottom panel shows the pool-count decomposition, with the productive share (purple line, right axis) declining as the long tail of sub-threshold pools inflated the denominator without capturing meaningful stake. The k=500 reference line marks the protocol's target pool count.

3.5. The market has crystallised — replacement, not growth

The near-constant stock of productive pools (a 700–1,000 historical band, 733 at epoch 623) masks significant underlying churn. This section decomposes the aggregate into three views:

the entry/exit flow;

the entity-level lifecycle that drives it;

the stake variability that pools experience even while they remain in the productive set.

3.5.1. Pool entries and exits — turnover sustains the stock, not growth

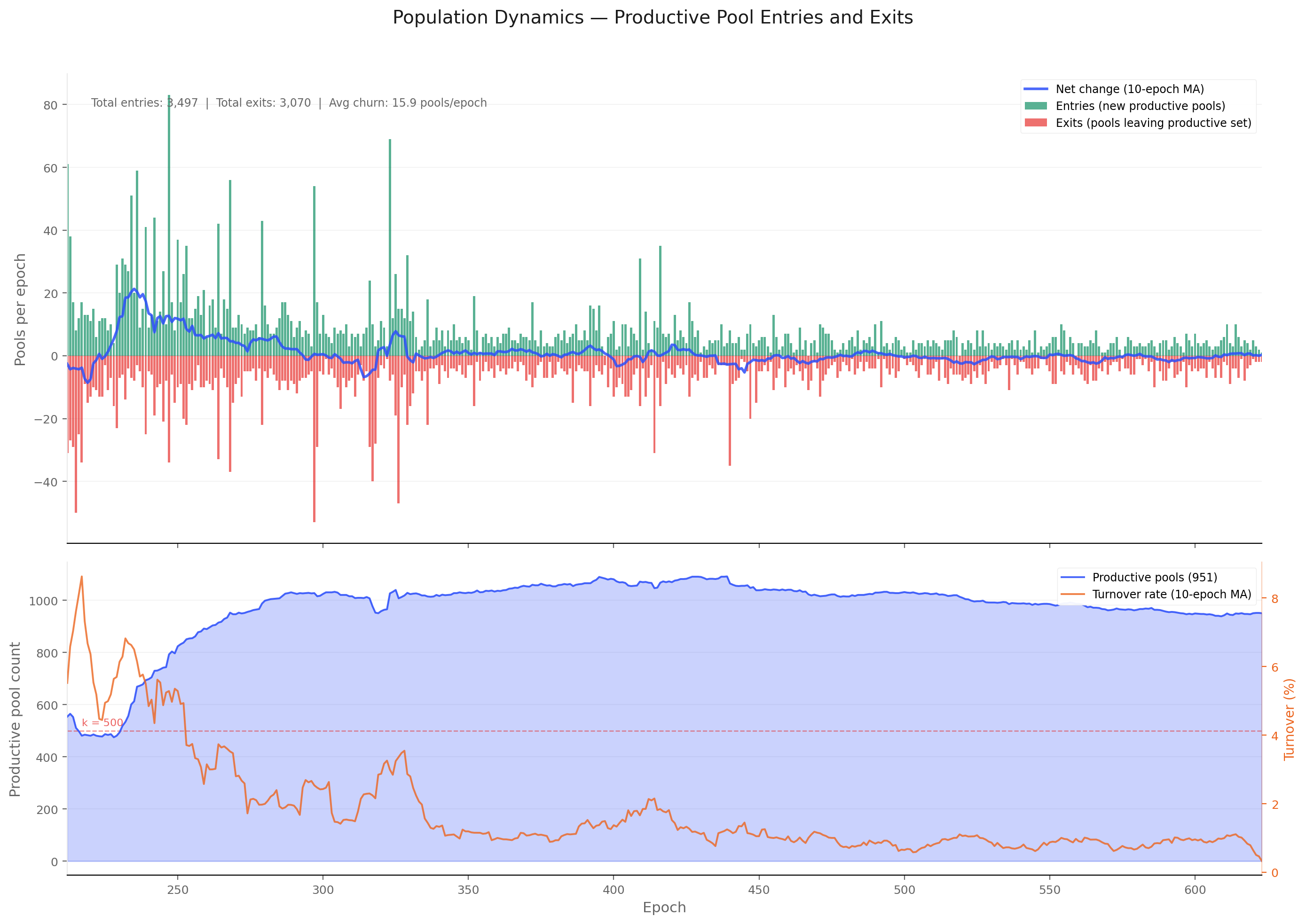

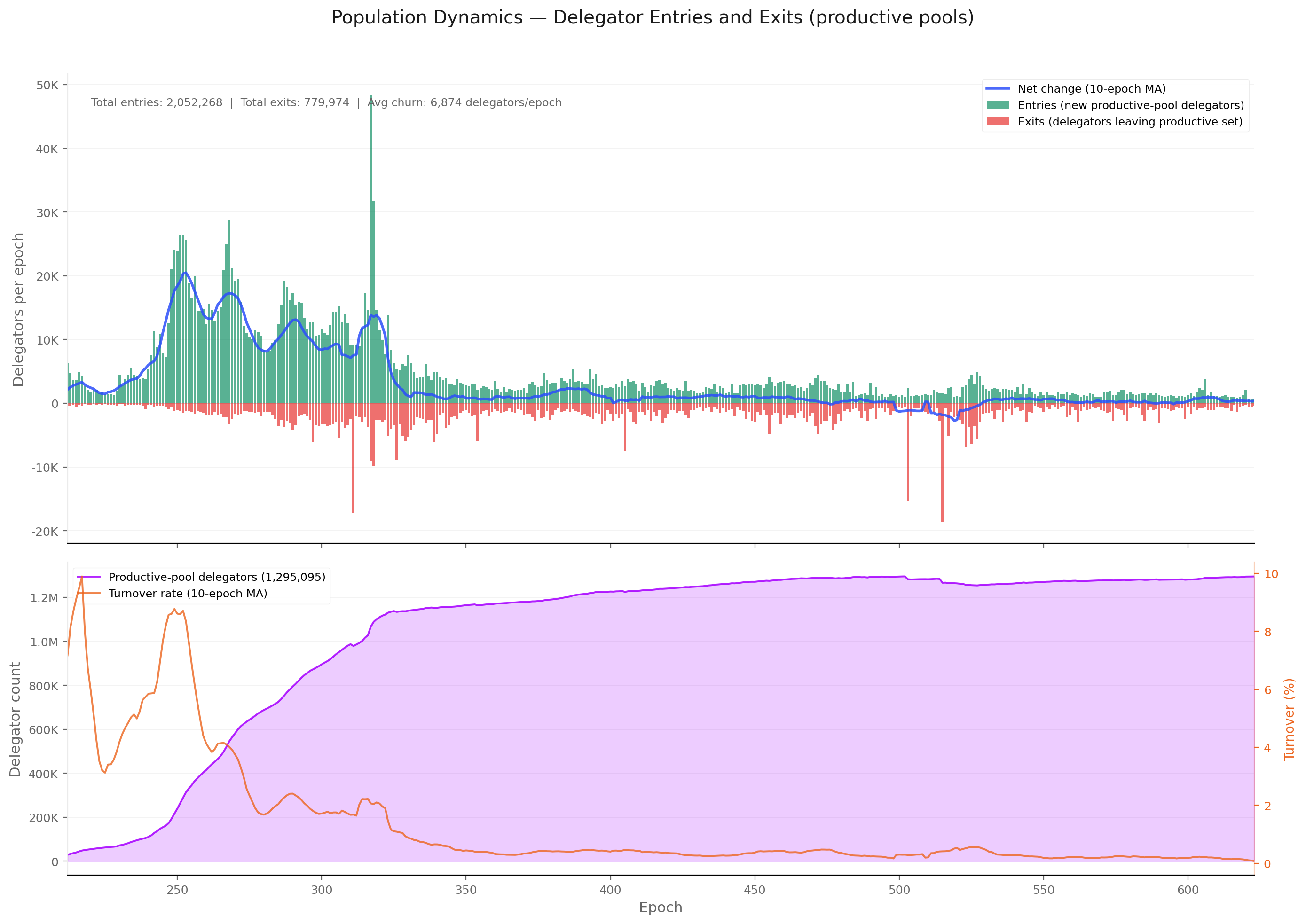

Tracking individual pools across consecutive epochs — counting those that cross the production threshold upward (entries) and those that fall below it or disappear (exits) — reveals the turnover that the aggregate count obscures.

FigureCEN.3.6Productive-pool entries and exits per epoch across the Shelley era. The ~700–1,000-pool quasi-equilibrium since epoch 300 conceals 3,497 entries against 3,070 exits with an average churn of ~15.9 pools per epoch — a 1.7% turnover rate driven by fragility near the production threshold.

The early Shelley period (epochs 212–300) saw rapid net growth as the pool population expanded from ~450 to ~1,000 productive pools. Growth epochs outnumbered decline epochs roughly 2∶1 during this phase.

From epoch 300 onward, the productive population stabilised: net changes per epoch fluctuate around zero, with growth and decline epochs occurring in roughly equal proportion. Over the full history (epochs 212–623), the productive set gained a net +427 pools — but the near-flat trajectory since epoch 300 means the overwhelming majority of that net gain occurred in the first 90 epochs.

The stability of the stock alongside non-trivial per-epoch fluctuation implies a quasi-equilibrium: pools that exit the productive set (falling below the rising threshold, retiring, or losing delegation) are replaced at roughly the same rate by new entrants or returning pools.

Tracking individual pool presence per epoch (05_pool_population_dynamics.sql) confirms this: over the full history the productive set recorded 3,497 entries against 3,070 exits, with an average churn of ~15.9 pools per epoch. The turnover rate (entries + exits as a share of the productive population) averages around 1.7% per epoch — higher than the delegator-side turnover of ~0.5%, reflecting the greater fragility of pool economics near the production threshold.

FromObservationCEN.O1 — Multi-pool entities flourished (23 → 85 entities, 65% → 76% of productive stake) while single-pool operators struggle (555 → 291 pools, 39% → 24% of stake)

Finding#3→ The pool count flat-lined since epoch 300; the equilibrium is replacement, not growth. Across the post-300 window, the productive count tracks a 700–1,000 band as the threshold rises with total stake — landing at 733 pools at epoch 623. 3,497 entries balance against 3,070 exits (~15.9 pools per epoch, 1.7% turnover). The apparent stability of the aggregate conceals a continuous replacement process: pools that fall below the rising threshold or retire are substituted at roughly the same rate by new entrants — but the composition shifts in favour of entity-operated pools (see CEN.O1.F6/F7).

3.5.2. How entities are born, grow, and exit — the lifecycle of the 85 attributed players

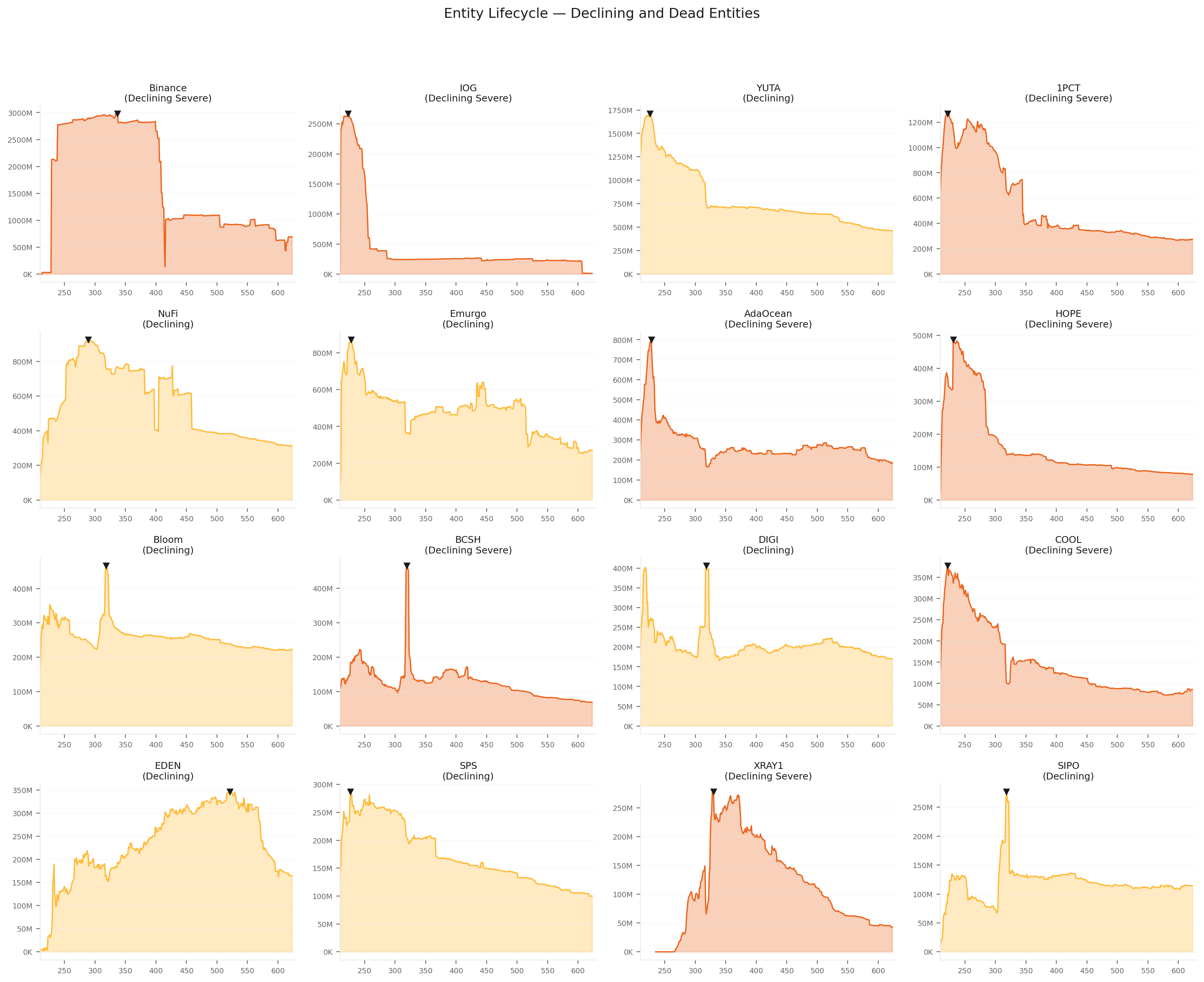

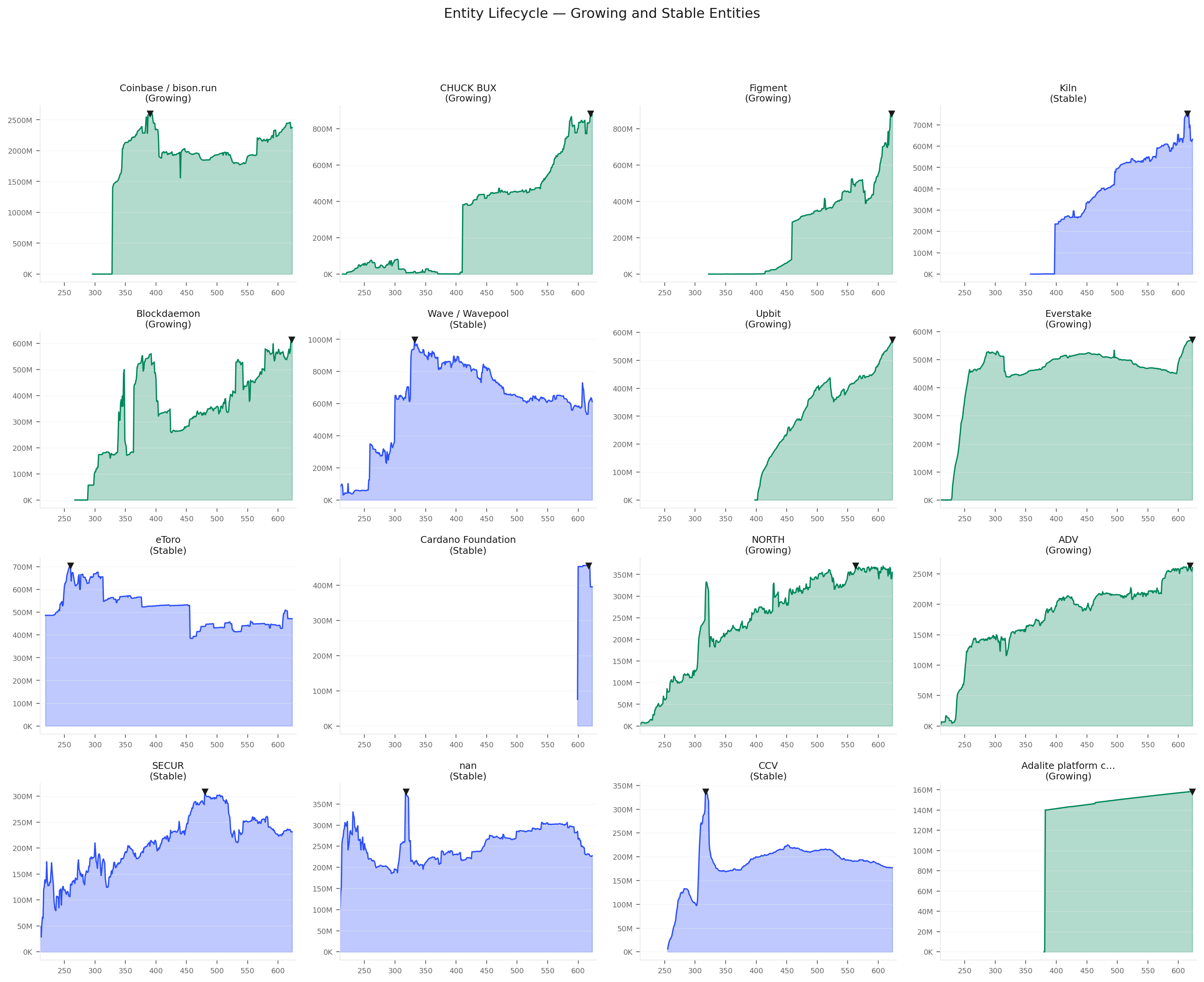

Part of the churn is driven by entity-level dynamics. The entity lifecycle analysis (data/entity_lifecycle_623.csv) classifies the 85 named entities into four phases — dead, declining, stable, and growing — based on their stake trajectory and productive-pool retention.

Declining and dead entities contract their pool fleets, feeding the exit side; growing entities and new single-pool operators feed the entry side. The entity-level decline trajectories are visualised in the figures below.

FigureCEN.3.7Stake and pool-count trajectories of declining and dead entities. These entities contract their fleets and feed the exit side of the productive-pool churn, accounting for a meaningful share of the 3,070 cumulative exits observed across the Shelley era.FigureCEN.3.8Stake and pool-count trajectories of growing entities. These entities feed the entry side of the productive-pool churn — partly offsetting the contraction of declining and dead entities tracked in the prior figure.

3.5.3. Who actually holds the productive set today — and who used to

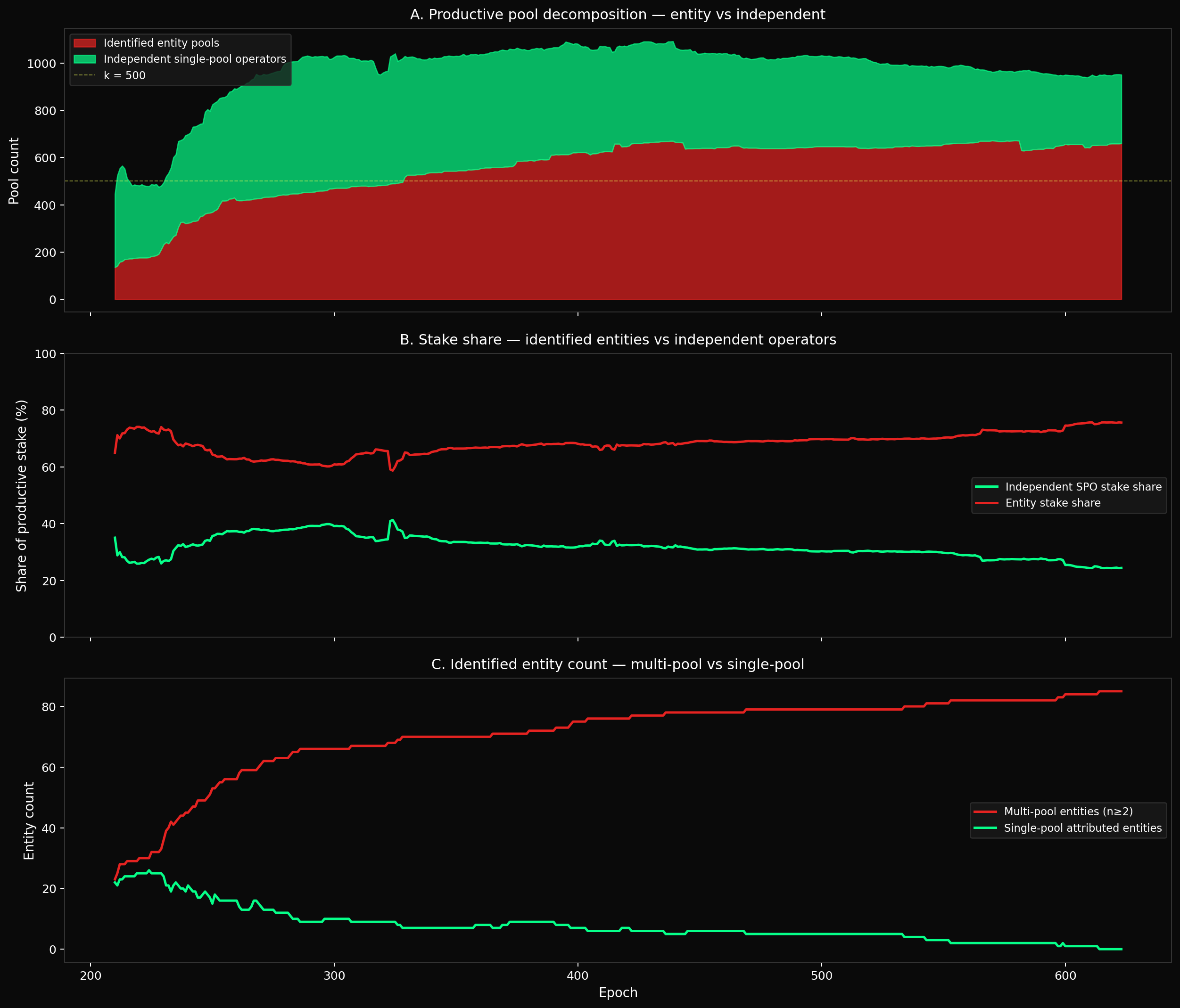

The entries-and-exits view (Entries and exits) treats the productive pool set as a homogeneous stock. This section decomposes it into two populations — pools operated by identified multi-pool entities and single-pool operators — and tracks each cohort's pool count and stake share across the full history.

FigureCEN.3.9Productive-pool cohort decomposition into single-pool operators versus multi-pool entities across the Shelley era. The single-pool cohort peaked at 555 pools (39.1% of stake) at epoch 300 and has contracted to 291 pools (24.4%) — a 48% loss in pool count and 15pp loss in stake share.

The single-pool operator segment is in structural decline.

The independent population peaked at 555 pools and 39.1% of productive stake around epoch 300 — the end of the Shelley expansion phase. Since then it has contracted in every period:

Period

Epochs

Independent pools

Stake share

Change

Shelley expansion

250–300

455 → 555

35.6% → 39.1%

+100 pools, +3.5pp

Early maturity

300–400

555 → 459

39.1% → 31.9%

−96 pools, −7.3pp

Mid maturity

400–500

459 → 385

31.9% → 30.3%

−74 pools, −1.6pp

Recent

500–623

385 → 291

30.3% → 24.4%

−94 pools, −5.9pp

The contraction accelerated in the recent period: 94 pools lost in 123 epochs, with the stake share dropping below 25% for the first time. The independent population has lost nearly half its pool count (555 → 291) and nearly 15 percentage points of stake share since its peak.

FromObservationCEN.O1 — Multi-pool entities flourished (23 → 85 entities, 65% → 76% of productive stake) while single-pool operators struggle (555 → 291 pools, 39% → 24% of stake)

Finding#6→ Independent operators are losing the field — 48% pool-count loss in 323 epochs. The single-pool population peaked at 555 pools / 39.1% of productive stake at epoch 300 and has contracted to 291 pools / 24.4% at epoch 623 — a 48% loss in pool count and 15pp loss in stake share. The contraction is continuous and has accelerated most recently (epochs 500–623). The quasi-equilibrium of Entries and exits masks a composition shift: the replacement pools that maintain the productive total are increasingly entity-operated, not independent.

Identified entities expanded steadily.

The number of multi-pool entities (n-MPO ≥ 2) grew from 23 at Shelley launch to 85 at epoch 623. Their pool count rose from 135 to 660, and their stake share from 65% to 75.6% of productive stake.

The expansion was not driven by a few large entrants — the fleet-size distribution shifted across all tiers:

Fleet size

Epoch 300

Epoch 623

2–3 pools

29 entities (12.4%)

36 entities (14.2%)

4–5 pools

17 entities (15.9%)

16 entities (13.5%)

6–10 pools

11 entities (11.0%)

18 entities (13.2%)

11–20 pools

3 entities (12.8%)

9 entities (30.3%)

21+ pools

6 entities (46.4%)

6 entities (28.8%)

The most striking shift is in the 11–20 pool tier: from 3 entities holding 12.8% of entity stake to 9 entities holding 30.3%.

The 21+ tier declined in share (46.4% → 28.8%) as IOG and Binance contracted, but the mid-tier fleets (6–20 pools) absorbed the gap.

Entity power is not merely growing — it is spreading across a broader fleet-size distribution.

FromObservationCEN.O1 — Multi-pool entities flourished (23 → 85 entities, 65% → 76% of productive stake) while single-pool operators struggle (555 → 291 pools, 39% → 24% of stake)

Finding#7→ Multi-pool entities absorbed the contraction and then some — fleet count nearly quadrupled. From 23 entities / 135 pools / 65% of stake at Shelley launch to 85 / 660 / 75.6% at epoch 623. The mid-tier fleets (6–20 pools) tripled their entity count and nearly doubled their stake share — entity power is not merely growing, it is spreading across a broader fleet-size distribution. The ~700–1,000-pool quasi-equilibrium is increasingly populated by entity-operated pools substituting for departing independents.

3.5.4. The independent operator pipeline has no observable expression in the data

The Cardano reward mechanism was designed to produce a progression path for operators: entry with an initial pledge, delegation-driven growth, and eventually full commitment as an established pool (The Intended Game §3.2).

The single-pool operator segment is the population where this trajectory should be observable — small operators entering, building reputation, attracting delegation, and graduating into established entities.

The data shows the opposite. The independent population contracted from 555 to 291 pools while its stake share fell from 39.1% to 24.4%.

The entity lifecycle analysis (Entity lifecycle, companion document) tracks where the capital went: toward late institutional entrants (IVaaS), exchanges holding ground, and a handful of community operators that grew against the tide. It did not flow toward a cohort of single-pool operators graduating into established entities.

The census cannot track individual single-pool operators over time (they are unattributed by definition), but the aggregate trajectory is unambiguous: the independent segment is shrinking, not graduating.

The absence of evidence for the designed growth path is itself diagnostic. If the mechanism were producing the intended progression — small operators growing into established ones — the independent segment would show either stable pool count (graduates replaced by new entrants) or growing stake share (successful operators attracting more delegation).

It shows neither. The pool count is falling and the stake share is falling faster, which means the independents that remain are also losing average delegation. The replacement process that maintains the productive total is driven by entity fleet expansion, not by new independent entrants.

FromObservationCEN.O1 — Multi-pool entities flourished (23 → 85 entities, 65% → 76% of productive stake) while single-pool operators struggle (555 → 291 pools, 39% → 24% of stake)

Finding#8→ The mechanism's designed progression path is invisible in the data. Entry → growth → established was supposed to feed the independent segment; instead it is contracting in both pool count and stake share, while the replacement pools that sustain the productive total are entity-operated. The growth path described in the formal design (The Intended Game §3.2) exists as a theoretical property of the intended equilibrium but not as an empirical feature of the observed one.

3.6. A pool's stake stability is segment-driven, not random

The entry/exit analysis tracks whether a pool is in the productive set; this section asks how much its stake fluctuates while it stays there.

A pool that survives all 73 epochs of the last year (epochs 551–623) may nonetheless experience large swings in delegation, with consequences for block production regularity and operator revenue predictability.

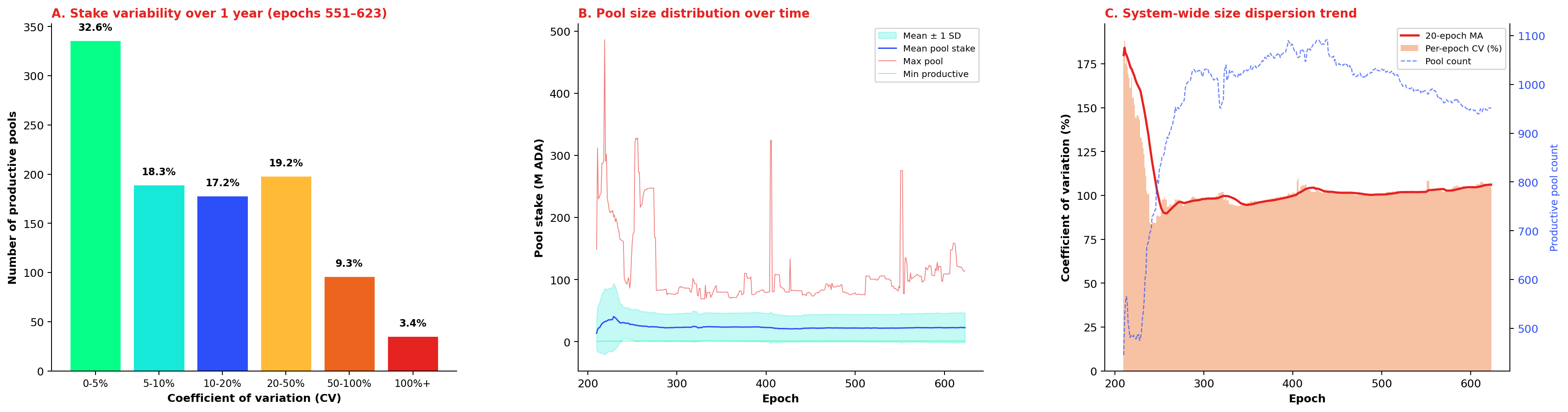

FigureCEN.3.10Pool-stake variability over the trailing 73 epochs. Roughly half the productive set has CV under 10%; 9.3% of pools sit between 50–100% CV and 3.4% exceed 100%. System-wide cross-sectional CV has compressed from >180% in early Shelley to ~105% since epoch 500.

Most productive pools are remarkably stable. Of the 1,032 pools present in at least 10 of the last 73 epochs and above the production threshold, roughly a third (32.6%) have a coefficient of variation (CV) of 5% or less — their stake barely moves from epoch to epoch.

Another 18.3% sit in the 5–10% band. Together, half the productive set operates with stake fluctuations under 10% over a full year.

A long tail of volatile pools exists. At the other extreme, 9.3% of productive pools have CV between 50% and 100%, and 3.4% exceed 100% — meaning their standard deviation is larger than their mean stake.

These are typically pools near the production threshold that oscillate in and out of viability, or pools that experienced a single large delegation event (arrival or departure of a whale) that dominates their variance.

System-wide dispersion has compressed over time. Panel C shows the cross-sectional CV of pool stakes across all productive pools at each epoch.

In the early Shelley era (epochs 210–260), the CV exceeded 180% — a handful of very large pools coexisted with hundreds of small entrants, producing extreme size dispersion.

As the pool population matured and the largest pools approached the saturation cap (~70.8M ADA at k=500), the CV declined steadily to ~105% by epoch 500 and has since plateaued. The remaining dispersion reflects the structural range between pools near the production threshold (~3M ADA) and the largest pools near saturation (~114M ADA) — a 100× ratio that the protocol's incentive design deliberately permits.

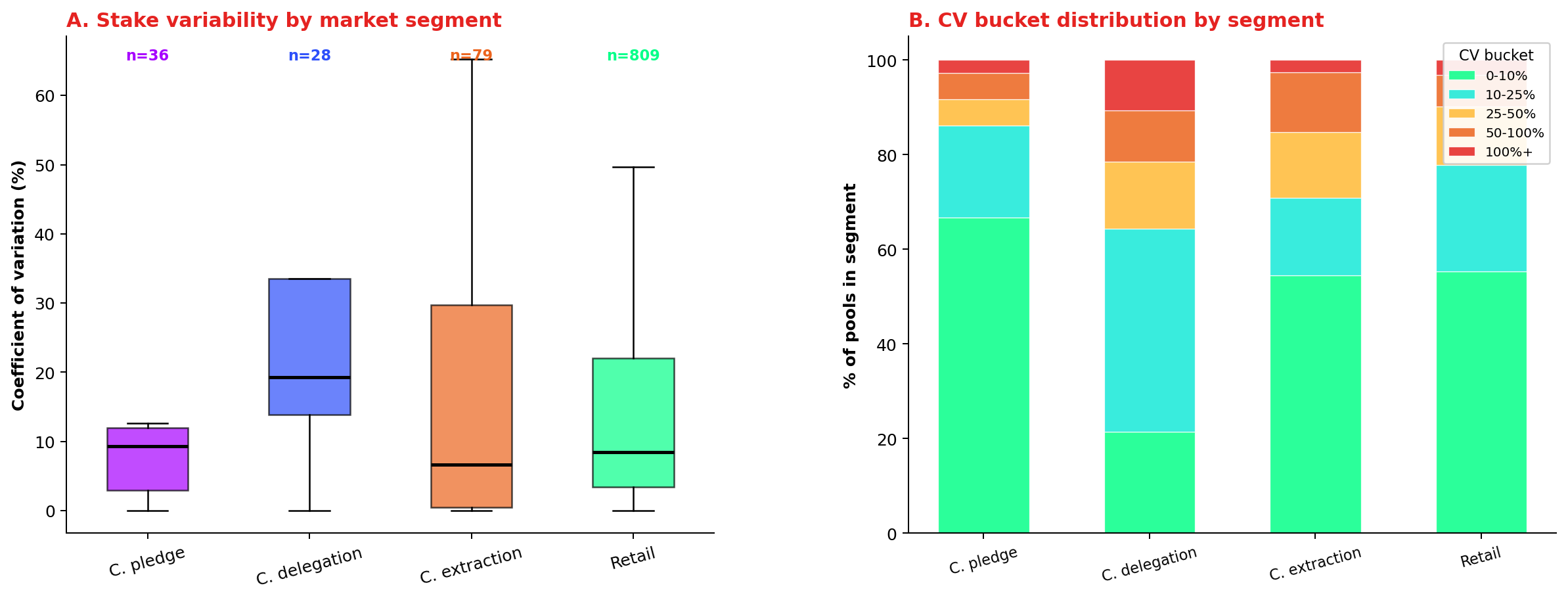

Variability differs across market segments. Crossing the per-pool coefficient of variation with the custodial taxonomy from the companion Operator's Cut reveals that not all segments fluctuate equally.

The custodial classification uses the per-pool median delegation from db-sync epoch_stake — the amount held by the typical delegator in each pool — rather than the mean ADA per delegation, which is inflated by whale addresses by a factor of 50–300,000× (see the companion Operator's Cut for the methodology and rationale).

FigureCEN.3.11Pool-stake coefficient of variation by custodial segment. Custodial-by-delegation pools are most volatile (median 19.3%, mean 43.0%), retail sits at 8.4% median, custodial-by-pledge at 9.3%, and custodial-by-extraction at 6.6% — stagnation, not active management, keeps the latter steady.

Custodial-by-delegation pools (28 pools where the median delegation exceeds 100K ₳) are the most volatile: median coefficient of variation of 19.3%, mean 43.0%, and 21% exceed 50%. These are pools dominated by whale self-delegation — a single address moving capital in or out produces large proportional swings.

By contrast, custodial-by-pledge pools (36 private, self-funded pools) sit at a median coefficient of variation of 9.3% — the operator controls the capital and has little reason to move it, with 67% below 10%.

Custodial-by-extraction pools (79 pools with ≥ 99% margin) sit at 6.6% median, with 54% below 10% — consistent with pools whose delegators are locked in by inertia or institutional constraint.

The retail market (809 pools, median delegation below 100K ₳) lands at a median coefficient of variation of 8.4%, with 55% of pools below 10%. This segment includes the large institutional operators (Coinbase, Binance, Kiln, YUTA) whose pools have high mean ADA per delegation but low median delegation — the majority of their delegators are small retail wallets.

The 10% tail above 50% in the retail segment captures pools that gained or lost a whale delegator — a single large address arriving or leaving a pool with hundreds of small delegators.

FromObservationCEN.O2 — When a Titan delegator switches pools, the whole pool moves with them — whale-funded pools swing ±20% between epochs (1 in 5 swings >50%) while retail pools barely move (±8%)

Finding#1→ When a Titan delegator switches pools, the whole pool moves with them — whale-funded pools swing ~±20% between epochs vs ±8% for retail. In 28 custodial-by-delegation pools (where the typical delegator holds ≥ 100K ₳), stake swings by roughly ±20% between epochs, and 21% of them swing more than 50% — a single Titan-tier address (10M+ ₳) is large enough that its in/out movement dominates the pool's variance, leaving the operator with unpredictable revenue and the remaining delegators with a wobbly block-production rhythm. Retail pools (809, broad small-delegator base) are mostly stable at ±8% between epochs — no single delegator is large enough to move the pool — but a 10% tail above 50% shows that even retail pools are vulnerable to single-whale shocks. Custodial-by-extraction (79 pools, ≥ 99% margin) barely budge (±7% between epochs, 54% below 10%) — stagnation, not active management, keeps their stake steady (delegators are locked in by inertia or institutional constraint). The technical metric used is the per-pool coefficient of variation (standard deviation / mean) over the trailing 73 epochs — see §3.6 — A pool's stake stability is segment-driven, not random for methodology.

Implications for delegators. A pool's stake stability matters because it affects block-production regularity and, by extension, the consistency of epoch rewards.

Delegators in low-CV pools experience smoother returns; those in high-CV pools face more variance. The data in data/pool_size_variability.csv provides per-pool CV, min, max, and range for further analysis; data/pool_cv_by_segment.csv gives the segment-level aggregate.

4. Delegators

4.1. What the raw db-sync shows — 1.85M certificates, half of them ghosts

Two db-sync tables count delegators in different ways:

Source

What it counts

Epoch 623 value

epoch_stake aggregation

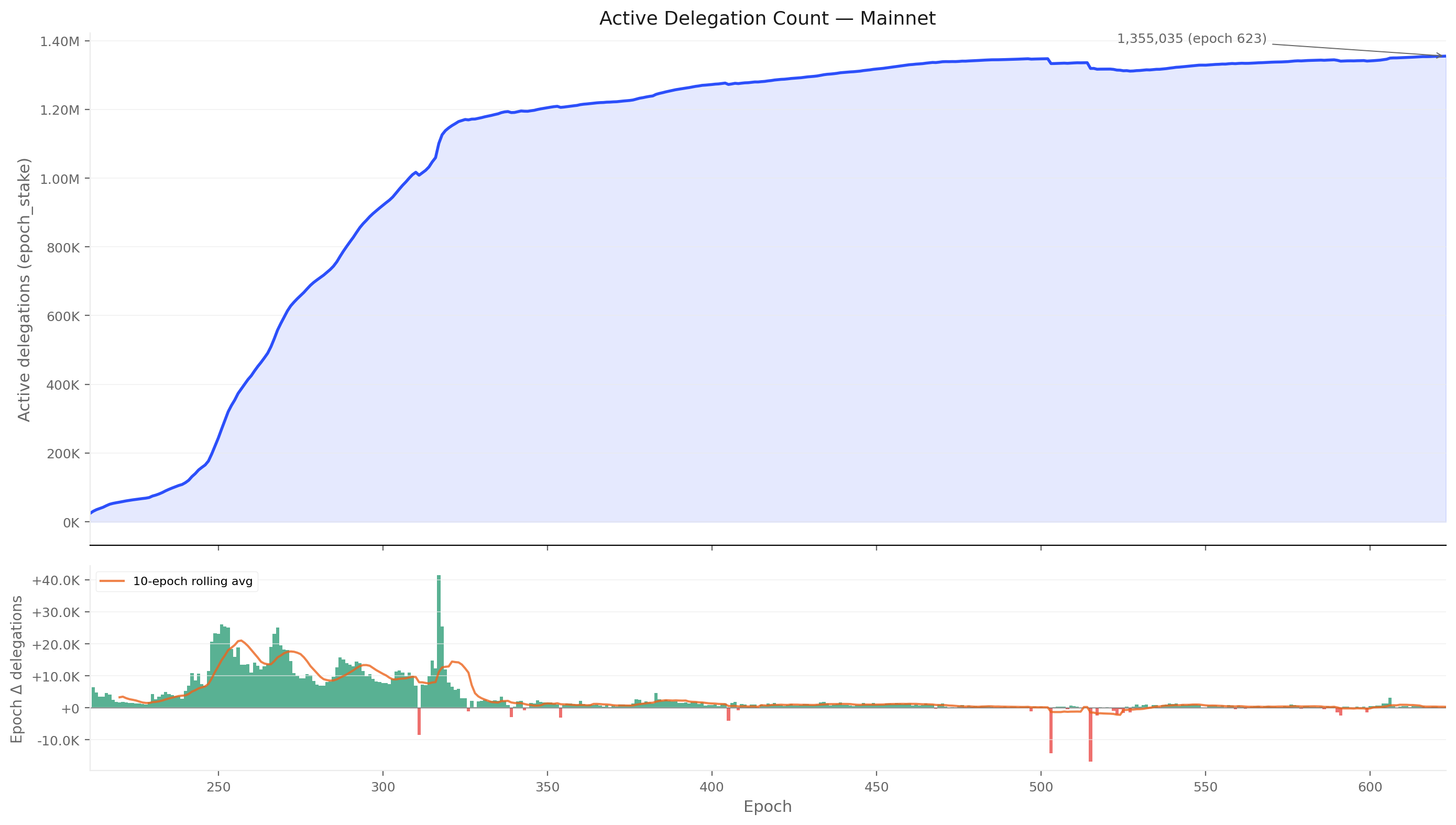

Rows with non-zero stake in the epoch snapshot

1,355,035 delegations across 2,877 pools

delegation table reconstruction

Active delegation certificates (regardless of balance)

1,847,713 addresses across 5,919 pools

The gap: ~493K addresses hold an active delegation certificate but have zero balance in the epoch_stake snapshot. Similarly, ~3,042 registered pools have delegation certificates pointing at them but carry no actual stake.

FigureCEN.4.1Raw versus cleaned delegator count across the Shelley era. The raw delegation table records 1,847,713 addresses and 5,919 pools, but ~493K certificates are zero-balance "ghosts" and 3,042 pools carry no actual stake; cleaning yields 1,355,035 active delegations across 2,877 pools.

4.2. Removing the ghosts — certificates without ADA aren't delegators

A delegation certificate is a declaration of intent: it records on-chain that an address wishes to delegate to a given pool, but it does not lock any funds. The ADA remains freely spendable.

An epoch_stake row, by contrast, is capital at work — it reflects the actual balance present at the snapshot boundary. An address with a certificate but no ADA earns no rewards and does not participate in consensus.

The gap between the two views arises because delegation certificates are never automatically revoked. When an address is emptied — typically because the holder transferred funds to an exchange, moved to another wallet, or simply stopped using Cardano — the certificate persists as a residual record pointing at a pool with zero backing stake. These orphaned records are the "certificate ghosts" removed in this step.

Metric

Raw (delegation table)

Clean (epoch_stake)

Noise removed

Active delegations

1,847,713

1,355,035

492,678 certificate ghosts (26.7%)

Active pools

5,919

2,877

3,042 empty pools (51.4%)

After cleaning: 1,355,035 delegations, 21.75B ADA across 2,877 pools.

4.3. Removing delegations to dead pools — the active set the mechanism actually rewards

The 1,925 pools below the production threshold (The structural floor) carry 59,937 delegations and 0.19B ADA. These delegators earn intermittent and unpredictable rewards. Removing them aligns the delegator population with the productive operator landscape.

After cleaning: 1,227,281 delegations, 21.18B ADA across 733 productive pools.

The 1,227,281 productive pool delegations are the cleaned population handed to the companion Operator's Cut analysis, which decomposes them further into operator self-stake, custodial, and retail segments.

4.4.2. Half the delegator base stakes less than a transaction fee — the wealth is in the top 0.07%

The 1.36M delegations carry 21.75B ADA — but the distribution across individual delegations is extremely unequal.

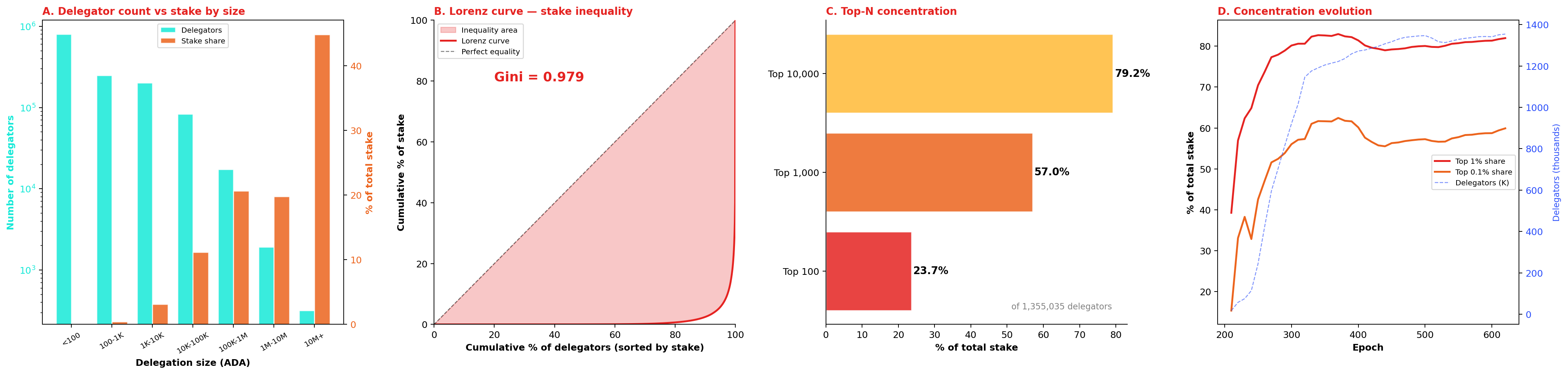

FigureCEN.4.2Delegator stake distribution at epoch 623 with the Lorenz curve. The bottom 59.1% of delegators (under 100 ADA) collectively hold 0.05% of stake; the top 318 delegators (0.02%) hold 44.8%. Gini coefficient: 0.976.

Size buckets:

Size cohort

Delegators

% of delegators

Stake (ADA)

% of stake

Mean (ADA)

< 100

801,067

59.1%

11.2M

0.05%

14

100 – 1K

249,181

18.4%

94.2M

0.43%

378

1K – 10K

201,797

14.9%

679.0M

3.12%

3,365

10K – 100K

83,307

6.1%

2.43B

11.18%

29,188

100K – 1M

17,439

1.3%

4.49B

20.63%

257,327

1M – 10M

1,926

0.14%

4.31B

19.80%

2.24M

10M+

318

0.02%

9.75B

44.80%

30.6M

The bottom 59.1% of delegators (under 100 ADA) collectively hold 0.05% of stake — less than any single delegation in the top tier. The top 318 delegators (0.02%) hold 44.8% of all staked ADA.

FromObservationCEN.O3 — The delegator population is wildly skewed in stake — 1,000 of 1.36M delegators (0.07%) hold 57% of staked ADA, and 9× population growth has not shifted the shape

Finding#1→ Half the delegator base stakes less than a single transaction fee at peak congestion.Median: 32 ADA. Mean: 16,055 ADA. The 500× gap measures the skewness of a power-law distribution — each tier above 10K ADA holds roughly 20% of total stake despite containing exponentially fewer delegators. Below 100 ADA: 801,067 delegators (59.1% of population) holding 0.05% of stake; above 10M: 318 delegators (0.02%) holding 44.8%.

Concentration metrics:

Metric

Value

Gini coefficient

0.976

Top 100 delegators → % of stake

23.7%

Top 1,000 → % of stake

57.0%

Top 10,000 → % of stake

79.2%

Median

32 ADA

P90

5,866 ADA

P99

142,775 ADA

The Lorenz curve (panel B) is nearly flat until the last few percent of delegators, then rises steeply — the classic signature of extreme concentration.

At Gini = 0.976, the Cardano staking distribution is more concentrated than the US wealth distribution (~0.85) and comparable to the most unequal asset distributions observed in financial markets.

FromObservationCEN.O3 — The delegator population is wildly skewed in stake — 1,000 of 1.36M delegators (0.07%) hold 57% of staked ADA, and 9× population growth has not shifted the shape

Finding#2→ The delegator population's stake is concentrated in its top 0.07%. Of the 1.36M active delegators, just 1,000 (0.07%) hold 57% of staked ADA; the top 10,000 (0.74%) hold 79.2%. Gini = 0.976 — more concentrated than US wealth (~0.85) and comparable to the most unequal asset distributions observed in financial markets. The identity of those top few thousand addresses (individual whale, exchange hot wallet, institutional custodian) determines whether the population's aggregate delegation signal reflects genuine preference or operational logistics.

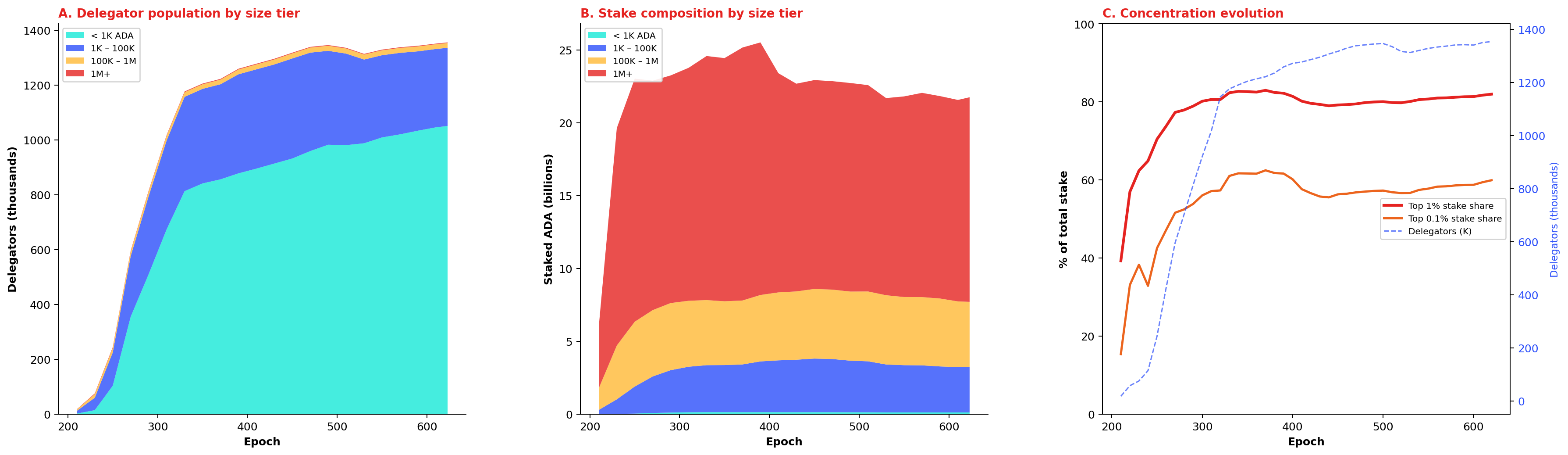

4.4.3. Concentration crystallised by epoch 300 — 9× growth in delegators, no change in the top-1%

FigureCEN.4.3Delegator population growth, stake composition, and concentration evolution from Shelley launch to epoch 623. The micro-delegator tier absorbs 96% of new entrants; the top-1% share rose to 78–82% by epoch 280 and has held there despite a 9× increase in delegator count.

The three panels trace how the delegator population, its stake composition, and its concentration structure evolved from Shelley launch (epoch 210) to epoch 623.

Panel A — Population growth by size tier. The delegator count grew from 17K (epoch 210) to 1.36M (epoch 623). Virtually all growth comes from the micro-delegator tier (< 1K ADA, cyan): this tier expanded from ~1,500 to ~1.05M, absorbing 96% of new entrants.

The 1K–100K tier grew from ~10K to ~285K. The 100K–1M tier plateaued around 17K, and the 1M+ tier barely moved — from ~1,100 at launch to ~2,200 today.

Panel B — Stake composition by size tier. In contrast to population, the stake is dominated by the 1M+ tier (red), which holds 14.1B ADA — 65% of total staked ADA — in just 2,244 addresses.

This tier reached its current level by epoch ~260 and has fluctuated within a narrow band since. The 100K–1M tier (gold) contributes 4.5B, the 1K–100K tier (blue) adds 3.1B, and the <1K tier — despite being 77% of the population — carries just 0.1B (0.5%). Stake composition has been essentially frozen since epoch 300.

Panel C — Concentration evolution. The top-1% share rose rapidly from 39% at Shelley launch to ~80% by epoch 280, then plateaued at 78–82%. The top-0.1% share follows a similar trajectory, stabilising at 48–52%.