The operator's revenue versus the delegator's share — Reward Flow stage 3

Through epoch 623 · 2026/04/09Nicolas Henin · 2026/06/18

This report analyses the third and final stage of Cardano's reward pipeline — the intra-pool split — and traces the structural forces that determine how much of each pool's reward reaches delegators versus operators. It builds on the empirical baseline established in the Analysis of Cardano's Incentive Mechanism (Lopez de Lara, 2025; hereafter the Incentive Mechanism Analysis) and operates downstream of the companion reports Treasury & Pool Pots Distribution (stage 1) and The Pools Pot Distribution Gaps (stage 2).

Every epoch, once the reward curve assigns a total reward to each pool, a second mechanism activates. The pool operator extracts a flat fee (a fixed ₳ amount, on-chain fixed_cost) and a commission (a proportional share, on-chain margin); the remainder is distributed pro-rata among all stake holders. Together the flat fee and commission compose the operator's pricing plan; their sum — the effective price — is the fraction of pool reward that never reaches delegators. This report asks how operators price, what the resulting market looks like, and whether the price-return relationship the mechanism produces can sustain the delegator–operator partnership the protocol depends on.

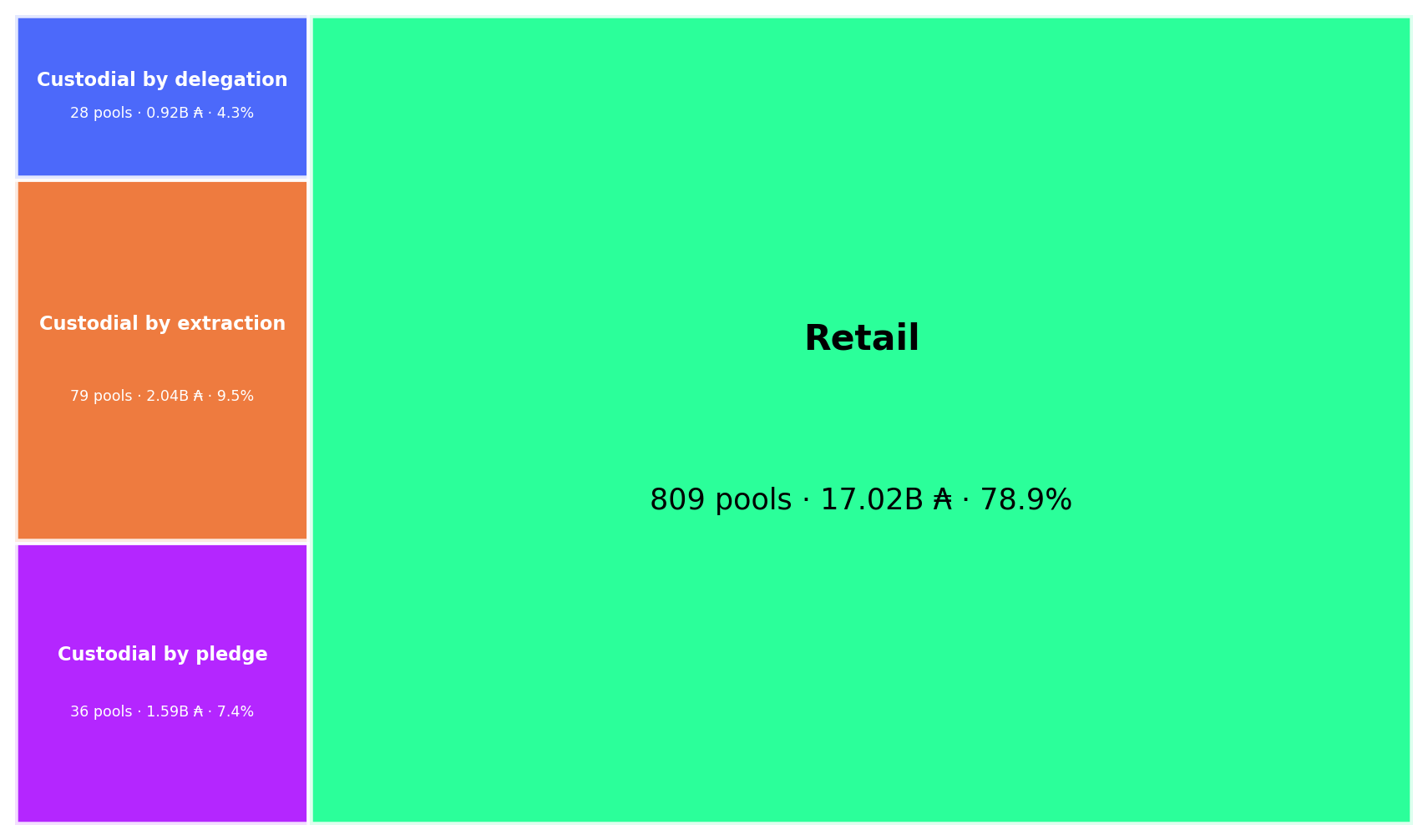

At epoch 623, 733 productive pools process 21.18B ADA of staked capital. After filtering the 21% of stake that is custodial (where the operator controls delegation addresses), the retail market consists of 809 pools, 516 entities, 17.02B ADA, and 1,272,836 delegators — with a median delegation of 87 ₳. This is the population where the pricing plan produces a genuine market outcome.

The flat fee dominates revenue but is frozen. The flat fee delivers 60% of retail operator revenue, yet behaves as a frozen governance artefact: 89.5% of pools pick one of two floor values, and 64% still declare the pre-halving 340 ₳ floor — 178 epochs after governance halved it to 170 ₳. The channel that dominates revenue is the one operators touch the least. Its shape is regressive: a fixed-in-₳ levy on a size-proportional reward produces a $1/\sigma$ hyperbola — 47.5% of pool reward at the sub-reliable tier, 1.5% at near-saturation. No other major PoS protocol uses a flat fee — Ethereum, Solana, Cosmos, and Polkadot all price validators on proportional rules.

The commission market is bimodal with an empty middle.87% of pools set a commission ≤ 10%; 12% set ≥ 99% (privatisation); the 89-percentage-point range between them contains 12 pools. Four discrete bands: no-commission (170 pools, 17.9%), competitive (658, 69.1%), no man's land (12, 1.3%), privatisation (112, 11.8%). No economic attractor exists between competitive pricing and full extraction.

21% of productive stake is custodial through three mechanisms, each with distinct economics.79 entities operating 143 pools (4.55B ADA) are custodial via three on-chain-detectable patterns: by pledge (10 entities self-fund their pools, median 1.76M ₳/yr revenue per entity), by extraction (57 entities charge ≥99% commission on inert delegators, 282K ₳/yr median), and by delegation (15 entities operate pools where the median delegation exceeds 100K ₳ — a single whale's wallet, 29K ₳/yr median). The three mechanisms produce three distinct economic outcomes — only the retail residual exhibits market dynamics.

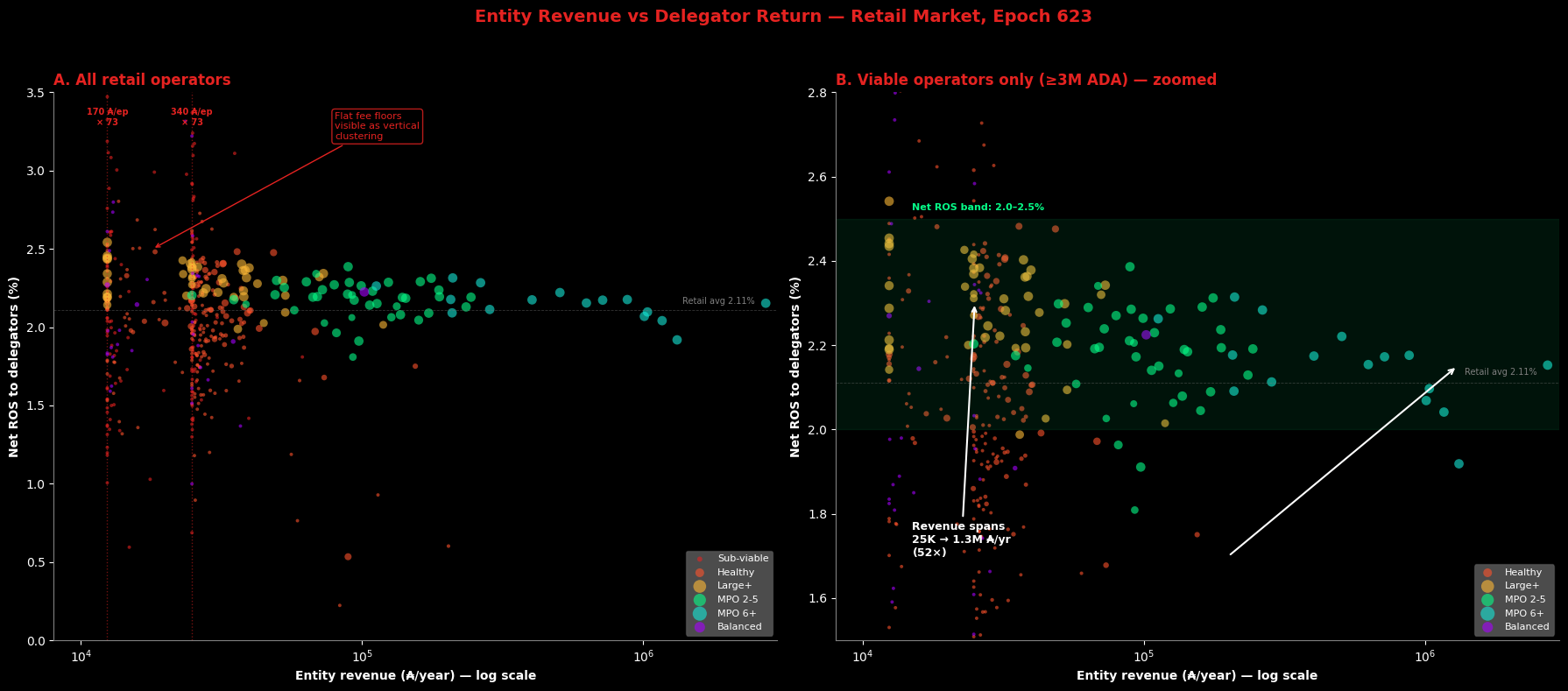

Delegators pay 18× more for the same return. A delegator in a sub-reliable pool pays 48.3% effective price for 2.04% net return; a delegator in a near-saturation pool pays 2.7% for 2.34% — 18× the price for 0.30 percentage points of return. Net return converges to 1.95–2.34% across the entire retail market regardless of effective price, operator type, or pool size. The return signal is too weak to discipline pricing — the discrimination threshold collapses inside block-production noise.

Operators who charge the most earn the least. A sub-reliable single-pool operator absorbs 48.3% of pool rewards but earns 24,820 ₳/yr. An 11+ pool MPO absorbs 7.7% but earns 1,035,496 ₳/yr — 42× more revenue at 6× less effective price. MPO revenue scales horizontally (more pools), not vertically (higher price): the 11+ pool bracket captures 26.5% of retail rewards through 7 entities. No single-pool operator in the retail market earns a competitive wage — the median ~25,000 ₳/yr (\$6,250 at \$0.25/ADA) covers infrastructure but not the 5–15 hrs/month of skilled work; competitive compensation begins only at the 2-pool MPO tier (~68,700 ₳/yr). The single-pool operator subsidises the network — and the flat fee penalises small-pool delegators without compensating small-pool operators.

Delegation follows visibility, not return.65.9% of retail delegators sit in hollow MPO pools at 2.18% net return; hollow single-pool near-saturation pools offer 2.34% — 0.16pp more — yet hold only 2.7% of delegators. The pledge premium is negative in the retail data: balanced median net return 1.98% vs hollow 2.08%, because the flat fee drag (1.06pp for balanced, 0.47pp for hollow single-pool) overwhelms the pledge benefit. The incentive mechanism's core assumption — that delegators can differentiate pools by return — fails in the empirical record.

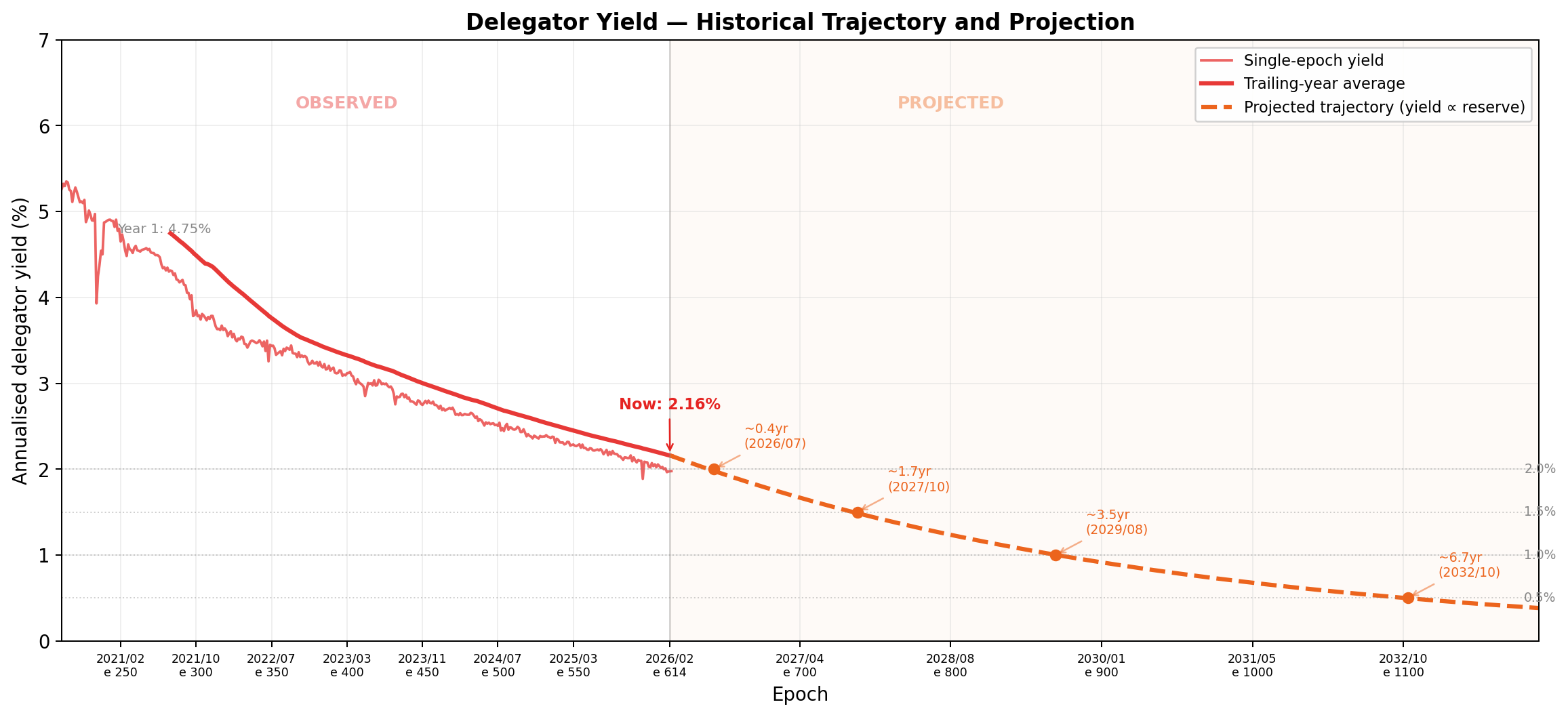

The mechanism is on a structural clock. Reserve depletion compresses the yield surface every epoch. Delegator yield has fallen 5.3% → 2.0% in 413 epochs (5.5 years), tracking reserve depletion with $R^2 = 0.99$; projected sub-1.5% within ~1.7 years, sub-1.0% within ~3.5 years. At 2.0%, Cardano sits below the USD risk-free rate (4.3%) and at the bottom of the PoS landscape. As the epoch pot shrinks, the fixed-in-₳ flat fee consumes a growing share of pool rewards — the confiscatory zone expands upward every epoch — and the 0.39pp retail yield spread compresses proportionally (at 1.0% base yield, the same relative dispersion produces ~0.20pp, indistinguishable from block-production noise). The decline is irreversible without protocol-level intervention: it is built into the monetary expansion formula. The selection ratchet against single-pool operators tightens with every epoch.

The remainder of the report walks the analysis in four parts: the formula presents the SL-D1 split rule in three layers (original notation → residual-split decomposition → reader-friendly rewrite → mainnet parameterisation); the productive population traces the operator and delegator sides from raw certificates to the productive set (≥3M ADA); the pricing plan landscape analyses the flat fee, commission, custodial/retail boundary, operator profitability, and delegator return; the delegator yield traces the trajectory, cross-chain comparison, and structural compression. All counts and amounts use epoch 623. Source data: pool_choice_quality_623.csv, pool_median_delegation_623.csv (db-sync epoch_stake), reward_split_snapshot_623.csv (synthetic, estimated from epoch 614 reward rate), koios_pool_history_mainnet.csv, mpo_entity_pool_mapping_mainnet.csv.

Table of Contents

1. Mainnet Observations

Terminology note. The protocol uses "fixed cost" and "margin" for the two extraction channels. This report adopts pricing-plan terminology: the fixed cost is the flat fee (a fixed ₳/epoch amount), the margin is the commission (a proportional share), and their sum — the operator take — is the effective price the delegator faces. The on-chain parameter names appear in §2 (the formula) and at first use in §4. Everywhere else, the pricing-plan terms apply.

OPE.O1

Observation 01 · 5 findings

The flat fee (fixed cost) dominates operator revenue — but governance sets it, and operators resisted the last cut

5 findings

The flat fee delivers 60% of retail operator revenue — yet operators don't compete on it. 89.5% of pools pick one of two floor values (the ones governance allows), so the parameter is effectively a governance-set price, not a competitive lever. When governance halved the floor from 340 ₳ to 170 ₳ in 2023, only ~36% of operators moved to the new floor — 64% still declare 340 ₳ today, 178 epochs (~1.5 years) after the cut. Operators are slow to follow even governance, and they actively resisted lowering the price the cut was meant to deliver to delegators.

The passive channel dominates the active one — the flat fee delivers 60% of operator revenue, the commission only 40%. Across the retail market, the fixed ₳/epoch flat fee accounts for 60% of operator revenue; the proportional commission accounts for the remaining 40%. The channel that dominates revenue is the one operators almost never touch.

Structural — the passive channel dominates the active one

Governance halved the floor 178 epochs ago — 64% of pools have not moved. The minPoolCost floor was halved from 340 ₳ to 170 ₳ through a successful governance action. 178 epochs later (~1.5 years), 64% of pools still declare 340 ₳ — including most of the largest entities. The price most operators charge is not a pricing decision; it is a governance setting they never revised.

Governance inertia — driven by the largest entities

The flat fee is a binary choice, not a pricing parameter.89.5% of pools declare one of two floor values (170 ₳ or 340 ₳). The "custom" values that exist are mostly near-floor inertia (Binance 345, Everstake 400) or commission-mode extraction. Operators are not pricing — they are picking a floor.

The flat fee is a binary choice, not a pricing parameter

The flat fee is regressive by design — a fixed ₳ levy on a size-proportional reward. Because the pool reward grows roughly linearly with stake $\sigma$ but the flat fee is fixed in ₳, the fee's share of pool reward follows a $1/\sigma$ hyperbola — 47.5% of pool reward at the sub-reliable tier, 1.5% at near-saturation. The same 170 ₳ that disappears in a saturated pool's accounts is a third of all rewards in a sub-reliable pool's accounts

Regressive by design — a fixed-in-₳ levy on a size-proportional reward

No other major PoS protocol uses a flat fee — the fixed-cost model is unique to Cardano. Ethereum (validator-flat reward via the protocol), Solana (commission), Cosmos (commission), and Polkadot (commission) all price validators on proportional rules that scale with stake. The Cardano flat fee has no cross-chain precedent or comparator — meaning the regressive dynamics in F4 are unique to this network

Unique to Cardano — no cross-chain precedent

OPE.O2

Observation 02 · 2 findings

The commission (margin) is doing two unrelated jobs: pricing a service on one side, privatising a pool without pledging on the other

2 findings

The commission was designed as the operator's pricing tool: set a rate, charge it on each reward. On mainnet that role has split in two. 87% of pools use it as intended — commission ≤ 10%, pricing the service. 12% of pools set it ≥ 99%, taking essentially all rewards regardless of who delegates: a private pool funded by delegation, functionally equivalent to a self-pledged pool but without locking any capital. The 89-percentage-point range between the two uses is essentially empty (only 12 pools). The protocol exposes a continuous parameter; operators reduce it to two unrelated economic stances — price a service, or quietly privatise the pool.

The commission distribution is bimodal with an 89pp empty middle.87% of pools set a commission at or below 10%; 12% set ≥ 99% (privatisation). The 89-percentage-point range between 10% and 99% contains only 12 pools. No economic attractor exists between competitive pricing and total extraction — operators either compete or fully privatise their pool, and almost no one in between

No man's land — no attractor between pricing and extraction

The market self-organises into four discrete tiers, not a continuous price distribution. No-commission (170 pools, 17.9% — almost certainly self-pledged), competitive (658 pools, 69.1% — at or below 10%), no man's land (12 pools, 1.3% — between 10% and 99%), privatisation (112 pools, 11.8% — at or above 99%). The four bands are an emergent equilibrium, not a design choice — the formula offers a continuous parameter and operators reduce it to four economic stances.

The market self-organises into discrete tiers

OPE.O3

Observation 03 · 3 findings

21% of productive stake is custodial — three mechanisms, three economics

3 findings

21.1% of productive stake sits in pools where the operator effectively keeps the rewards rather than delivering them to a retail delegation market. The delegation flow exists on-chain, but it isn't doing the work the formula assumes — the operator is. Three on-chain-detectable mechanisms achieve this, with very different per-entity economics:

(i) By pledge — self-funded pools. 10 entities self-stake their own pools (operator owns ≥95% of the delegation). They capture 100% of rewards because they are the delegators. Median: 1.76M ₳/yr per entity.

(ii) By extraction — near-100% commission. 57 entities set the commission ≥ 99%, taking essentially all rewards regardless of who delegates. The pool is funded by delegation, but the operator collects everything (see OPE.O2). Median: 282K ₳/yr.

(iii) By delegation — whale-only pools. 15 entities operate pools where the typical (median) delegation exceeds 100K ADA — meaning the "delegators" are a small circle of whales, not retail. The pool serves an inner circle, not the open market. Median: 29K ₳/yr.

The three mechanisms produce three very different revenue scales (60× spread), but share the same underlying property: the open delegation market is not allocating this stake — the operator is.

A fifth of productive stake is custodial — and it splits into three distinct mechanisms, not one.79 entities operating 143 pools hold 4.55B ADA — 21.1% of productive stake in custodial pools. The split: (i) by pledge (10 entities, 36 pools, 1.59B — operator self-funds the pool); (ii) by extraction (57 entities, 79 pools, 2.04B — high commission on inert delegators); (iii) by delegation (15 entities, 28 pools, 0.92B — typical delegation ≥100K ₳). Each mechanism is detectable from on-chain observables and produces a different operator economics

The median delegation is what separates retail from custodial — not the mean. Custodial-by-delegation flags pools where the per-pool median delegation (db-sync epoch_stake) is ≥ 100K ₳ — i.e., where the typical delegator is a whale, not the average dragged up by one whale. For comparison, a delegation of 50K ₳ is already in the top 1.5% of all delegations on the network. The median measures the delegator's experience; the mean measures capital concentration. They are not the same signal.

Each custodial mechanism produces a different economic outcome — by an order of magnitude. Median operator revenue per entity: custodial-by-pledge: 1,759,252 ₳/yr (operator captures 100% of rewards on self-funded pools); custodial-by-extraction: 281,831 ₳/yr (privatisation commission on inert-delegator pools); custodial-by-delegation: 29,329 ₳/yr (small whale pools, not revenue machines). Treating "custodial" as one population obscures a 60× revenue spread

Each custodial mechanism is its own economy

OPE.O4

Observation 04 · 2 findings

The retail market is 79% of stake and the typical delegator holds 87 ₳

2 findings

Once custodial pools are filtered out, the retail market is 809 pools, 516 entities, 17.02B ADA and 1,272,836 delegators — with a median delegation of 87 ₳ that is remarkably uniform across operator types, from independent single-pool to Coinbase and Binance.

Once custodial pools are filtered out, the retail market is bigger than mean-based estimates suggested — and it includes institutions.809 retail pools, 516 entities, 17.02B ADA, 1,272,836 delegators. The retail-by-median-delegation classification keeps Coinbase, Binance, Kiln and other institutional operators inside the retail market — because their typical delegator is a small holder, even if the institutional brand is large. The retail market is the population the mechanism was designed for; it is the population every reform has to address

The retail market is larger than mean-based estimates

The typical retail delegator holds 87 ₳ — and the median is remarkably uniform across operator types. The median retail delegation across the entire 1.27M-delegator population is 87 ₳. Per-operator-type medians range from 45 to 962 ₳ — a tight 20× span across pool types from independent single-pool to Coinbase. Retail delegators are small, homogeneous, and yield-insensitive at this scale — any reform that prices below 87 ₳/year of incremental yield will not change their behaviour

Retail delegators are small and homogeneous

OPE.O5

Observation 05 · 2 findings

Delegators pay 18× more for the same return

2 findings

A sub-reliable delegator pays 48.3% effective price for 2.04% net return; a near-saturation delegator pays 2.7% for 2.34% — 18× the price for 0.30 percentage points of extra yield. Net return converges to 1.95–2.34% across the entire retail market — a signal too narrow to discipline pricing.

A delegator pays 18× more for 0.30 percentage points of extra yield. A delegator in a sub-reliable pool pays a 48.3% effective price (flat fee + commission as % of pool reward) for a 2.04% net return. A delegator in a near-saturation pool pays 2.7% for 2.34% — 18× lower price for 0.30pp more return. The effective price is a mechanical artefact of pool size (the flat fee's 1/σ regression), not a market signal — operators are not pricing competitively, the formula is pricing them

Net return converges to a narrow 1.95–2.34% band across the entire retail market — the signal is too weak to drive delegation. Regardless of pool size, operator type, or pricing plan, a retail delegator's net yield ends up between 1.95% and 2.34% — a 0.39 percentage point spread across the whole market. At this resolution, the yield signal cannot discipline operator pricing — delegators are not chasing 0.4pp of return; they are picking on visibility, brand, or convenience

Return signal too narrow to discipline pricing

OPE.O6

Observation 06 · 4 findings

Stake pool operator profitability ranges from 24K to 1M ₳/yr — operators who charge the most earn the least

4 findings

Operator revenue scales with fleet size, not price — the sub-reliable single-pool operator absorbs 48.3% of pool rewards for 24,820 ₳/yr, while an 11+ pool MPO absorbs 7.7% for 1,035,496 ₳/yr (42× more revenue at 6× less price). No single-pool operator in the retail market earns a competitive wage.

The operators who charge the most earn the least — and vice versa. A sub-reliable single-pool operator absorbs 48.3% of pool rewards but earns only 24,820 ₳/yr. An 11+ pool MPO absorbs only 7.7% of pool rewards but earns 1,035,496 ₳/yr — 42× more revenue at 6× less effective price. The flat fee penalises small-pool delegators without compensating the operators who run those pools — both sides of the small-pool transaction lose

MPO revenue scales horizontally (more pools), not vertically (higher price). The 11+ pool bracket captures 26.5% of retail rewards through 7 entities. Their per-pool fee is the same 170/340 ₳ floor everyone else uses — they win by running more pools, not by pricing differently. Fleet size, not pricing, drives MPO operator economics — meaning a reform that targets pricing leaves fleet revenue untouched

Fleet size, not pricing, drives operator economics

The retail market is dominated by hollow operators — 95% of revenue, 0% pledge.57 hollow MPOs capture 64.4% of retail rewards; 414 hollow single-pool operators share 31.1%. Together hollow operators absorb 95.5% of retail reward flow through pools that pledge near-zero. The 41 balanced operators (those with meaningful pledge) share only 1.2%. Pledge is not the dominant revenue strategy — neither for fleets nor for single-pool operators

No single-pool operator in the retail market earns a competitive wage for their labour. Median single-pool revenue is ~25,000 ₳/yr (~\$6,250 at \$0.25/ADA) — covers infrastructure (~\$1,300–3,200/yr) but not the 5–15 hours/month of skilled DevOps at any reasonable hourly rate. Competitive compensation begins only at the 2-pool MPO tier (~68,700 ₳/yr). The single-pool operator is economically subsidising the network — sustained by non-economic motivation, not by the reward mechanism

Single-pool operators subsidise the network

OPE.O7

Observation 07 · 2 findings

Delegation follows visibility, not return

2 findings

Delegators do not chase yield — 65.9% sit in hollow MPO pools at 2.18% net return while hollow single-pool near-saturation peers offer 2.34%. The pledge premium is negative once the flat fee drag (1.06pp for balanced vs 0.47pp for hollow) is priced in.

Two thirds of retail delegators sit in pools that pay less than the alternative — yield is not what they are choosing on.65.9% of retail delegators sit in hollow MPO pools at 2.18% net return; hollow single-pool near-saturation pools offer 2.34% — 0.16pp more — and yet hold only 2.7% of delegators. Delegators are not chasing yield — they are picking on visibility, brand, exchange convenience, or default selection. The return signal does not drive delegation

The pledge premium is negative in the retail data — balanced operators deliver less net return than hollow ones. Balanced (genuine pledge commitment) operators deliver a median net return of 1.98%; hollow operators deliver 2.08%. The reason is mechanical: balanced single-pool operators incur a 1.06pp flat-fee drag vs 0.47pp for hollow ones, and that drag overwhelms whatever pledge premium the reward curve is supposed to add. The incentive mechanism's core assumption — that pledge commitment translates to better delegator outcomes — does not hold in the data

The mechanism's core assumption fails

OPE.O8

Observation 08 · 3 findings

Reserve depletion is a structural clock: every epoch, the pot shrinks, the confiscatory zone widens, and yields erode

3 findings

Reserve depletion is a structural clock built into the formula. Yield has fallen 5.3% → 2.0% in 413 epochs (R² = 0.99 with reserve), and the trajectory is irreversible without protocol-level intervention.

Concrete projections (from epoch 623, ~April 2026): ~12 months out (~Q2 2027) — yield at ~1.7%. ~20 months out (~Q4 2027) — yield crosses 1.5%. ~42 months out (~Q3 2029) — yield crosses 1.0%.

Each epoch the pot shrinks, the fixed-in-₳ flat fee consumes a growing share of pool rewards, and the retail yield spread compresses toward block-production noise. The failures documented in §4 don't stay still — they degrade every epoch by the same mechanical clock.

The delegator yield has fallen from 5.3% to 2.0% in 5.5 years and the decline is built into the formula. Yield has tracked reserve depletion with $R^2 = 0.99$ across 413 epochs. Projection from epoch 623 (~April 2026): ~1.7% within ~12 months, sub-1.5% within ~20 months (~Q4 2027), sub-1.0% within ~42 months (~Q3 2029). The decline is irreversible without protocol-level intervention — it is built into the monetary expansion formula. The entire yield surface descends as a unit; no pool-level strategy can offset the macro trajectory

The confiscatory zone expands upward every epoch — the failures in §4 are not static, they get worse mechanically. As the epoch pot shrinks, the flat fee (fixed at 170/340 ₳) consumes a growing share of pool rewards — the confiscatory zone from §4.1 expands upward. The 0.39pp retail yield spread compresses proportionally: at 1.0% base yield (~Q3 2029), the same relative dispersion produces ~0.20pp — indistinguishable from block-production noise. Pools productive today will cross the sub-reliable threshold purely from macro depletion. The failures documented in §4 are not static — they degrade every epoch

The declining yield is a selection ratchet against small single-pool operators. The flat fee is fixed in absolute terms while the epoch pot shrinks — the confiscatory zone expands upward every epoch. Single-pool operators bear the full drag with no fleet to amortise it; multi-pool operators are insulated by horizontal scaling. The structural feedback loop (yield compression → confiscatory expansion → single-pool attrition → delegation migration → fleet concentration) drives the centralisation the mechanism was designed to prevent

The mechanism selects against its smallest operators and reinforces its largest

OPE.O9

Observation 09 · 2 findings

Cardano's yield is no longer competitive — and the case for staking now rests on an ADA appreciation that hasn't materialised

2 findings

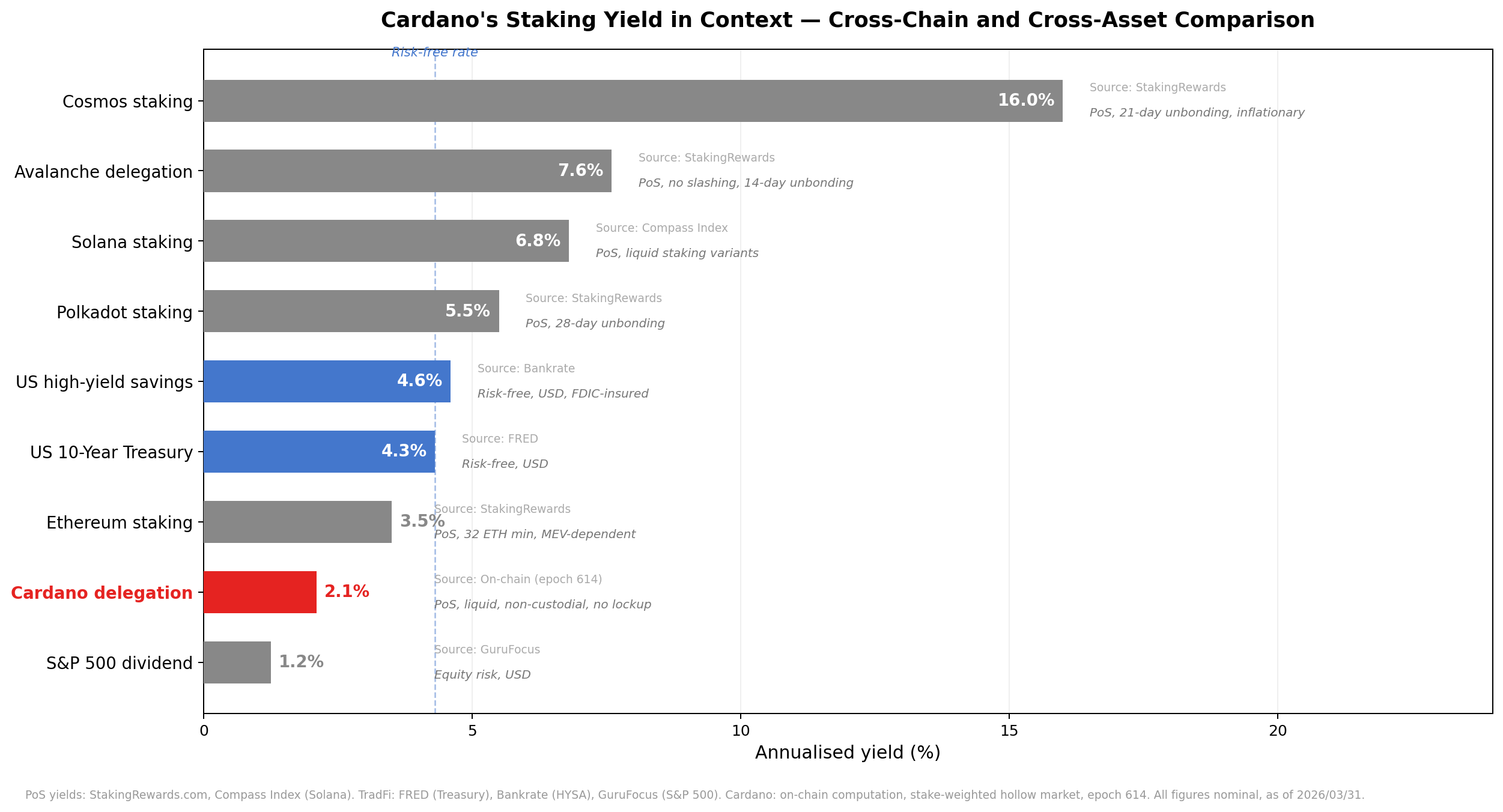

At 2.0%, Cardano's delegation yield sits below the USD risk-free rate (4.3%) and at the bottom of the PoS chains' yield ladder. No other major chain combines this low a yield with liquid, non-custodial, slashing-free design.

The mechanism's design premise was that delegators stake because (i) the yield itself is meaningful and (ii) ADA appreciates in real terms (the formula's monetary design assumes deflation-like behaviour). Both assumptions are now under stress. The yield premise has empirically degraded (OPE.O8); and ADA has not shown the appreciation/deflation behaviour the formula was designed around — the case for delegation now rests almost entirely on a price thesis the protocol cannot guarantee.

If ADA fails to deliver real appreciation, the psychological effect compounds: delegators face low yield AND uncertain price, leaving only conviction-driven holders. The mechanism assumes yield-sensitive delegators; the regime now selects against them.

At 2.0%, Cardano sits below the USD risk-free rate and at the bottom of the PoS landscape. Cardano's current 2.0% delegation yield is below the USD risk-free rate of 4.3% and at the bottom of the PoS chains' yield ladder. No other major chain combines this low a yield with liquid, non-custodial, slashing-free design. The low return is the cost of that design — but the design now asks delegators to accept a yield below the risk-free rate, which only conviction-driven holders will do

The mechanism's premise depends on ADA appreciation that hasn't materialised — and if it doesn't, only conviction-driven holders remain. The reward formula was designed around a monetary regime where ADA itself appreciates (the reserve-depletion design implies deflationary-like behaviour as the supply approaches its cap). In practice, ADA price has not delivered that appreciation, leaving delegators with low yield + uncertain price. The mechanism's assumption — that yield-sensitive delegators allocate based on competitive returns — collapses to a self-selected pool of long-conviction holders, who do not respond to the formula's pricing levers. If the deflation premise fails, the psychological pressure compounds: there is no yield case AND no appreciation case, only a conviction case — which the formula cannot manufacture

Yield + price = double-sided pressure on the conviction case

2. The formula — intra-pool reward sharing

These formulas define how a pool's realized allocation is split between the operator and the rest of the pool participants. The split happens only after the pool-level reward has already been computed and adjusted by apparent performance.

The distribution logic is sequential:

first, the operator flat fee (on-chain: fixed_cost, denoted $c$) is deducted — a fixed ₳ amount per epoch

second, the operator commission (on-chain: margin, denoted $m$) is applied to the remaining amount — a proportional share

finally, the residual reward is distributed proportionally across all stake holders

The sum of flat fee and commission is the effective price (on-chain: pool_fees) — the fraction of pool reward that never reaches delegators.

In this final step, the operator still receives a stake-proportional share through the pledge held inside the pool, while delegators receive the complementary share.

The intra-pool split was specified in Design Specification for Delegation and Incentives in Cardano (Kant, Brünjes & Coutts, IOHK, 2019 — deliverable SL-D1, Implications). The mechanism has been operational on mainnet since the Shelley hard fork on 2020/07/29. The split logic itself has never been modified; the only governance action affecting the intra-pool split was the reduction of minPoolCost from 340 to 170 ADA at epoch 445 (2023/10/27).

2.1. SL-D1 (Original)

The operator and member rewards are two complementary views of the same split rule applied to the realized pool allocation.

Once the pool-level reward has been computed, the split follows the same sequence:

cover the operator fixed cost first

apply the operator margin to the remaining amount

distribute the residual proportionally across stake holders

Under this rule, the operator receives both the explicit operator share and the stake-proportional share attached to the pledge held inside the pool, while each member receives a stake-proportional share of the residual amount.

Operator reward, using the operator stake-share ratio $\frac{s}{\sigma}$ as a single input:

$$

r_{\text{operator}}\left(\hat f,c,m,\frac{s}{\sigma}\right)=

\begin{cases}

\hat f, & \hat f \le c \\

c + (\hat f-c)\left(m + (1-m)\frac{s}{\sigma}\right), & \hat f > c

\end{cases}

$$

Member reward, using the member stake-share ratio $\frac{t}{\sigma}$ as a single input:

$$

r_{\text{member}}\left(\hat f,c,m,\frac{t}{\sigma}\right)=

\begin{cases}

0, & \hat f \le c \\

(\hat f-c)(1-m)\frac{t}{\sigma}, & \hat f > c

\end{cases}

$$

2.2. Residual split decomposition

Before switching to reader-friendly variable names, it is useful to separate the split rule into the two regimes induced by the fixed operator cost $c$. Let

where $\mu(\hat f,c,m)$ is the operator margin extracted from the residual reward and $\psi(\hat f,c,m)$ is the remaining amount to be shared proportionally across stake holders.

This makes the split easy to read: fixed cost first, operator margin second, and proportional sharing of the remainder third.

A fundamental property becomes visible in this form. The operator's reward has two structurally distinct components:

$$

Reward^{\text{operator}} = \underbrace{Cost + Margin}_{\text{extracted from the pool's total reward}} + \underbrace{Share\,\rho^{\text{operator}}_{i}}_{\text{earned exactly as a delegator would}}

$$

The third term — $Share\,\rho^{\text{operator}}_{i}$ — is identical in form to any member's reward: a pro-rata share of the residual, proportional to the stake contributed.

For the capital the operator pledges into the pool, the protocol treats the operator exactly as it treats a delegator. There is no special reward channel for pledge at this stage — the operator earns the same per-ADA yield as every other participant in the pool.

What distinguishes the operator from a delegator is the first two terms: $Cost$ and $Margin$. These are the only channels through which the operator can redirect part of the reward flow that is generated by other participants' stake. The fixed cost is a flat extraction; the margin is a proportional extraction. Both apply to the pool's total reward before pro-rata distribution, and both reduce the yield that delegators receive.

In other words: the operator's own capital is rewarded identically to delegated capital. The operator's privilege — the compensation for running infrastructure, bearing the pledge risk, and maintaining the pool — is expressed entirely through cost and margin.

The split formula does not reward the operator for pledging; it rewards the operator for operating.

The pledge mechanism that makes commitment economically significant lives upstream, in the reward curve (§2 of the main report), not in the intra-pool split.

2.4. Mainnet parameterization

Parameter

Value

Set by

minPoolCost ($c_{\min}$)

170 ADA (reduced from 340 at epoch 445)

Protocol parameter (governance)

Fixed cost ($c$)

Operator-declared, $\geq c_{\min}$

Pool registration certificate

Margin ($m$)

Operator-declared, $\in [0, 1]$

Pool registration certificate

At epoch 623 (hollow-strategy pools): the majority of rewarded hollow-strategy pools declare $c = 340$ ADA (the former minimum). The median declared margin is 2.0%; the entity-level median is 1.0% and the stake-weighted mean is 3.8%.

2.5. Concept glossary

Symbol

Name

Definition

$\hat{f}$

Actual pool reward

Performance-adjusted output of the reward curve (stage 2)

$c$

Declared fixed cost

Operator-declared flat ADA, $\geq c_{\min}$

$c_{\text{eff}}$

Effective fixed cost

$\min(c, \hat{f})$ — the actual ADA deducted

$m$

Margin

Operator's declared share of reward after cost deduction

$c_{\min}$

Minimum pool cost

Protocol-enforced floor on $c$ (currently 170 ADA; formerly 340 ADA)

Operator take

$c_{\text{eff}} + m(\hat{f} - c_{\text{eff}})$

Total declared-fee extraction (= on-chain pool_fees)

Delegator pot

$(1-m)(\hat{f} - c_{\text{eff}})$

Amount entering pro-rata distribution

Effective tax

Operator take / $\hat{f}$

Fraction of pool reward extracted before pro-rata

3. The productive population

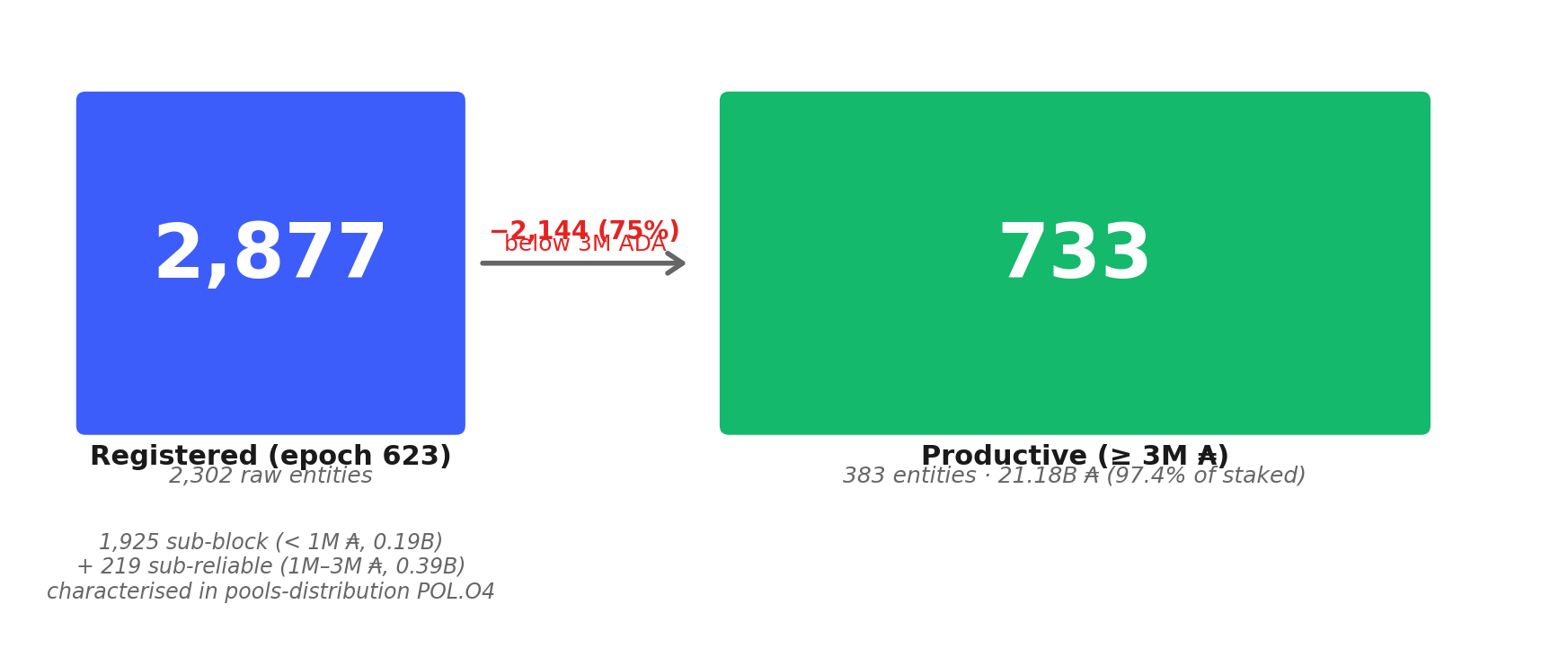

All analysis from §4 onwards operates on the productive population at epoch 623 — the subset of pools, operators, and delegations that clear the production threshold (≥3M ADA): a 95% probability of producing ≥1 block per epoch (λ=3 in the Poisson model — see POL.O3.F1 in the companion Pools Pot Distribution report). Below this threshold, pools produce blocks too sporadically for delegator returns or operator economics to be meaningful — they are dropped from the analysis here, then characterised separately in pools-distribution as the sub-block (< 1M) and sub-reliable (1M–3M) tails.

Figure 3.1From raw to productive population at epoch 623 on both sides of the market. Of 2,302 raw entities and 2,877 raw pools, the productive set (pools ≥3M ADA, the 95%-block-probability bar) retains 383 entities across 733 productive pools holding 21.18B ADA — 97.4% of all staked supply.

3.1. Operators

Segment

Entities

Pools

Stake

Share

Raw total (epoch_stake)

2,302

2,877

21.75B

100%

Sub-block tail (< 1M ADA — noise floor)

1,742

1,925

0.19B

0.9%

Sub-reliable tail (1M–3M ADA — block-producing but economically marginal)

213

219

0.39B

1.8%

Productive total (≥3M ADA)

383

733

21.18B

97.4%

of which:

Identified entities

83

449

16.24B

76.7%

— multi-pool fleets

71

437

15.69B

74.1%

— single-pool attributed

12

12

0.55B

2.6%

Unattributed single-pool operators

284

284

4.94B

23.3%

The 219 sub-reliable pools (1M–3M ADA) are block-producing in expectation but economically marginal: 91% are single-pool operators, 117 still declare the 340 ₳ flat fee, and 9 reach 100% effective price — the flat fee alone consumes the entire pool reward. They are characterised in Pools Pot Distribution — POL.O4 as part of the sub-block tail; they are excluded from the operator-economics analysis here because the pricing-plan signal is dominated by the production-threshold geometry at that scale, not by operator decisions.

Entity attribution is a lower bound — operators using entirely separate infrastructure and branding for each pool remain invisible.

3.2. Delegators

The delegation pipeline starts from 1.85M raw delegation certificates and removes two layers of noise: zero-balance certificates (27% of raw — delegation records with no ADA behind them) and delegations to sub-productive pools.

Segment

Delegations

Stake

Share

Pools

Raw (delegation certificates)

1,847,713

—

—

3,190

Zero-balance certificates (noise)

492,678

0

—

313

epoch_stake total

1,355,035

21.75B

100%

2,877

Sub-block tail delegations (< 1M pools)

59,937

0.19B

0.9%

1,925

Sub-reliable tail delegations (1M–3M pools)

67,817

0.39B

1.8%

219

Productive pool delegations (≥3M)

1,227,281

21.18B

97.4%

733

of which:

Identified entity pools

904,850

16.24B

76.7%

449

Unattributed single-pool operators

322,431

4.94B

23.3%

284

The 1,227,281 delegations in productive pools are where the pricing plan produces meaningful outcomes. The downstream analysis (§4.3 — Custodial versus retail) decomposes this productive population into operator self-stake, custodial, and retail segments.

The companion Staking Census documents the full cleaning pipeline. All counts and amounts reference epoch 623 unless otherwise noted.

4. The pricing plan landscape

The formula gives operators two extraction channels: a fixed cost $c$ (on-chain: fixed_cost, constrained by protocol parameter minPoolCost) and a proportional margin $m$ (on-chain parameter margin). In pricing terms, the fixed cost functions as a flat fee — a fixed ADA amount per epoch, independent of pool size — and the margin functions as a commission — a proportional share of the reward after the flat fee is deducted. Together they compose the operator's pricing plan; their sum, the operator take, is the effective price the delegator faces. This section categorises the pool population along each pricing channel; §4.3 — Custodial versus retail classifies the delegation side (custodial versus retail); and §4.4 — Operator profitability versus delegator return crosses both to measure operator profitability against delegator return.

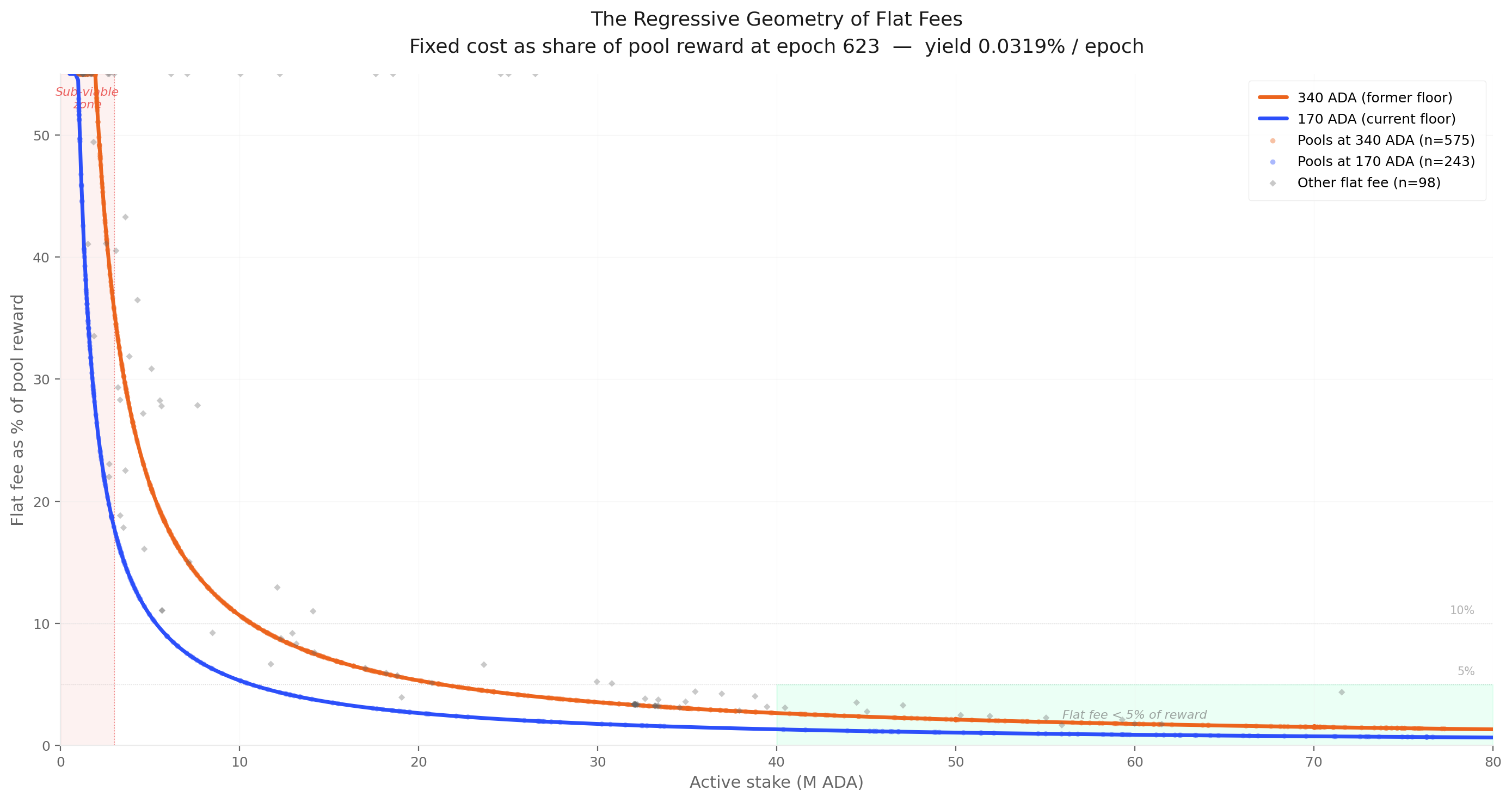

4.1. The flat fee (fixed cost)

The flat fee is the ADA amount deducted from every pool's reward before commission and pro-rata distribution (on-chain: declared fixed_cost $c$, constrained by protocol parameter minPoolCost). It is constrained by the protocol floor $c_{\min}$, currently 170 ₳ (reduced from 340 ₳ at epoch 445, on 2023/10/27).

FromObservationOPE.O1 — The flat fee (fixed cost) dominates operator revenue — but governance sets it, and operators resisted the last cut

Finding#1→ The flat fee delivers 60% of retail operator revenue while behaving as a frozen governance artefact. Across the retail market, the fixed-cost channel — set once and rarely revisited — generates 60% of operator income; the actively priced commission channel generates only 40%. The economic weight runs through the passive parameter, not the active one. The split inverts the usual intuition that operators compete on commission: in practice, the floor value an operator declared at registration dominates what they earn.

No other major PoS protocol uses a flat fee — Cosmos, Solana, Polkadot, Ethereum, and Tezos all use either a single proportional commission or no protocol-level fee at all. The flat fee is unique to Cardano, and its economic weight follows a $1/\sigma$ hyperbola: confiscatory for small pools, invisible for large ones.

FromObservationOPE.O1 — The flat fee (fixed cost) dominates operator revenue — but governance sets it, and operators resisted the last cut

Finding#5→ No other major proof-of-stake protocol uses a flat fee.Ethereum, Solana, Cosmos, Polkadot, and Tezos all price validators on proportional rules — a single commission, or no protocol-level fee at all. The fixed-cost channel is unique to Cardano. There is therefore no cross-chain comparator for the regressive geometry it produces, and no precedent for tuning it. Every observation about its effect on the pool economy is an observation about a single-network experiment.

At epoch 623, 89.5% of the 733 productive pools declare one of the two floor values — 170 ₳ or 340 ₳. The remaining 10.5% (100 pools) declare other values.

Decomposing this population reveals that the "custom" label conceals three structurally distinct behaviours:

Near-floor inertia (Binance at 345 ₳, Everstake at 400 ₳, OCEAN at 500 ₳);

Extraction (11 pools with FC > 500 ₳ and commission ≥ 99%);

A handful of single-pool operators at intermediate values.

Flat-fee strategy

Definition

Pools

Share

Entities

Stake (B)

Stake share

Delegators

Del. share

Adopted

$c = 170$ ₳ (current floor)

244

25.6%

186

5.13

23.8%

223,419

17.2%

Legacy

$c = 340$ ₳ (former floor)

608

63.9%

350

14.38

66.7%

679,158

52.4%

Near-floor

$171 < c \leq 500$, $c \neq 170, 340$

84

8.8%

48

1.82

8.4%

381,652

29.5%

Extraction

$c > 500$

16

1.7%

14

0.24

1.1%

10,869

0.8%

The inertia is structural: 70% of floor-declaring stake remains at 340 ₳, 178 epochs after the reduction, driven by the largest entities (Coinbase, Kiln, Upbit, eToro, Wave) which have not updated.

FromObservationOPE.O1 — The flat fee (fixed cost) dominates operator revenue — but governance sets it, and operators resisted the last cut

Finding#3→ The flat fee is a binary choice, not a continuous pricing parameter.89.5% of productive pools declare one of two floor values (170 ₳ or 340 ₳); the remaining 10.5% are split between near-floor inertia (Binance at 345 ₳, Everstake at 400 ₳) and outright extraction (16 pools above 500 ₳, typically paired with ≥ 99% commission). The "custom value" label conceals two structurally distinct behaviours and almost no genuine pricing in between. Operators do not set a flat fee — they pick one of two floors or signal extraction.

FigureOPE.4.1Flat-fee share of pool reward as a function of pool stake. Because the fee is fixed in ADA but reward scales with stake, the share absorbed follows a $1/\sigma$ hyperbola — 47.5% at the sub-reliable tier shrinking to 1.5% near saturation, a 32× span in effective extraction from the same nominal price.

FromObservationOPE.O1 — The flat fee (fixed cost) dominates operator revenue — but governance sets it, and operators resisted the last cut

Finding#4→ The flat fee follows a $1/\sigma$ hyperbola: 47.5% of pool reward at sub-reliable, 1.5% near saturation. Because $c$ is fixed in ADA but the pool reward scales with stake, the share absorbed by the flat fee falls as $1/\sigma$. At the sub-reliable tier the channel consumes 47.5% of pool reward; at the near-saturation tier it consumes only 1.5%. The same nominal price produces a 32× span in effective extraction. The flat fee is therefore regressive by design — a fixed-in-ADA levy on a size-proportional reward — and the regressivity is the structure, not a calibration error.

Finding#2→ 64% of pools still declare the former floor (340 ₳) — 178 epochs after the governance action halved it. The inertia is not transient. It is driven by the largest entities and reflects a structural feature of the network: the flat fee is a set-and-forget parameter for most operators. Among the 219 sub-reliable pools (1M–3M ADA), the distribution mirrors the productive population (84 adopted, 117 legacy) — but the economic meaning is different. At this tier, a 170 ₳ flat fee absorbs ~27% of pool reward and a 340 ₳ fee absorbs ~54%. The adopted/legacy distinction, which is a governance-responsiveness signal for productive pools, becomes a confiscation-severity signal for sub-reliable ones.

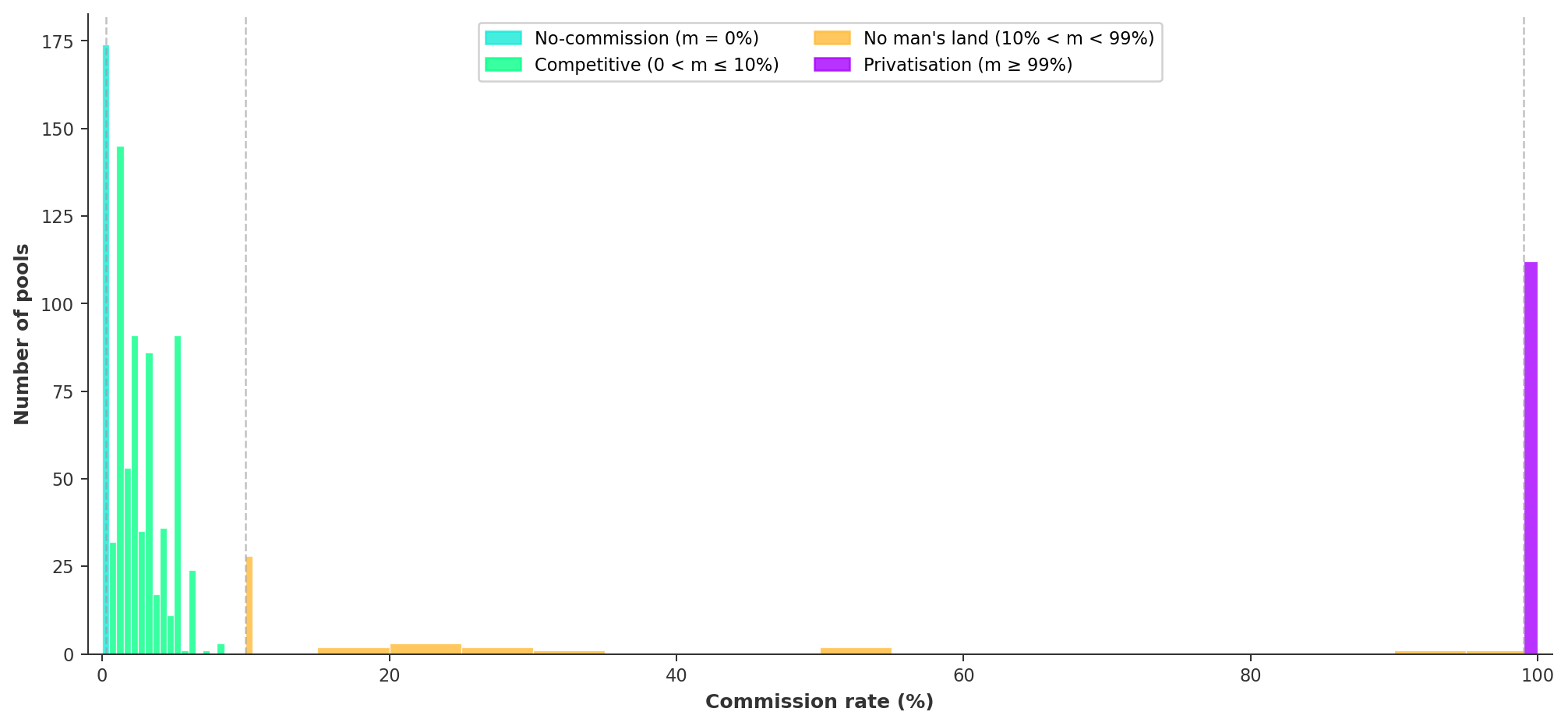

4.2. The commission (margin)

The commission is the operator's proportional share of the reward after the flat fee is deducted (on-chain: margin $m \in [0, 1]$). Unlike the flat fee, which clusters at two protocol-floor values, the commission is continuously variable and has no enforced floor or ceiling. It is the only fully unconstrained parameter in the intra-pool split, and the one that most directly expresses the operator's pricing intent.

The commission distribution is bimodal: the median is 2.0% and has been stable for over 400 epochs. The distribution clusters at round values — 1%, 2%, 3%, 5%, 10% account for the bulk of the competitive band.

Band

Range

Pools

Share

Stake (B)

Stake share

Delegators

Del. share

Economic logic

No-commission

$m = 0\%$

170

17.9%

2.70

12.5%

146,931

11.3%

Flat-fee-only pricing — the operator earns through the flat fee and pro-rata owner share only

Competitive

$0 < m \leq 10\%$

658

69.1%

15.23

70.6%

1,125,795

86.9%

The market norm — operators blend flat fee and commission. The upper end (6–10%) includes institutional operators: Binance, Figment, Blockdaemon, Kiln

No man's land

$10\% < m < 99\%$

12

1.3%

0.09

0.4%

331

<0.1%

Structurally empty — 12 isolated pools scattered across an 89pp range

Privatisation

$m \geq 99\%$

112

11.8%

3.55

16.5%

22,041

1.7%

Total extraction — de facto private operation. Top entities: CHUCK BUX, Upbit, eToro

87% of pools price at or below 10%; density drops to near zero above 10% and resurfaces only at 99–100%.

No man's land makes the bimodality explicit: the 89pp gap between competitive pricing and privatisation is a desert — an operator pricing above 10% is either extracting (and would go to 99%+) or running a niche service (and would not need more than 10%).

FromObservationOPE.O2 — The commission (margin) is doing two unrelated jobs: pricing a service on one side, privatising a pool without pledging on the other

Finding#1→ The commission distribution is bimodal with an 89pp structural gap. 87% of pools sit at or below 10%; 12% sit at ≥ 99%. The range between 10% and 99% contains 12 pools. No economic attractor exists between competitive pricing and total extraction.

Finding#2→ The market self-organises into four discrete commission bands.170 pools (17.9%) charge no commission; 658 (69.1%) sit in the competitive band (0–10%); 12 (1.3%) occupy the 10–99% no-man's-land; 112 (11.8%) declare privatisation (≥ 99%). The bands are not statistical artefacts — each carries a distinct economic logic, from flat-fee-only pricing through the market norm to total extraction. The 89pp gap between competitive and privatisation is the absence of any viable strategy in between.

FigureOPE.4.2Commission distribution at epoch 623. The market self-organises into four discrete bands: 17.9% of pools at no-commission, 69.1% in the competitive 0–10% band, 1.3% in the 10–99% no-man's-land, and 11.8% at privatisation (≥ 99%) — with an 89pp structural gap.

Commission bands × owner-stake strategy. The bands cross-cut the three owner-stake strategies. The hollow segment fills all four bands. Balanced pools concentrate in no-commission and competitive with marginal presence in privatisation. Private pools occupy only competitive (3 pools — Wave and one anonymous) and privatisation — private × no-commission is empty because an operator who funds the pool has no reason to set commission to zero.

4.3. Custodial versus retail

Not all staked ADA is delegated by independent participants choosing a pool on the open market. A significant share is custodial — controlled by operators rather than by the on-chain delegators themselves. Identifying these pools is necessary before the profitability analysis (§4.4 — Operator profitability versus delegator return) can isolate the genuine pricing market.

4.3.1. Clear custodial — by pledge and by extraction

Two mechanisms produce unambiguous custodial outcomes, detectable from a single on-chain observable.

Custodial by pledge — private-strategy entities (owner-stake ≥ 95%) that fund their pools with their own capital. The operator is the delegator. The commission (typically 100%) is self-directed — it never leaves the operator's control.

Custodial by extraction — non-private pools that declare a privatisation commission (≥ 99%). The operator does not fund the pool but captures virtually all rewards through the commission. Delegators earn near-zero yield; whether they remain through inertia, ignorance, or institutional constraint, their delegation is not a meaningful market signal.

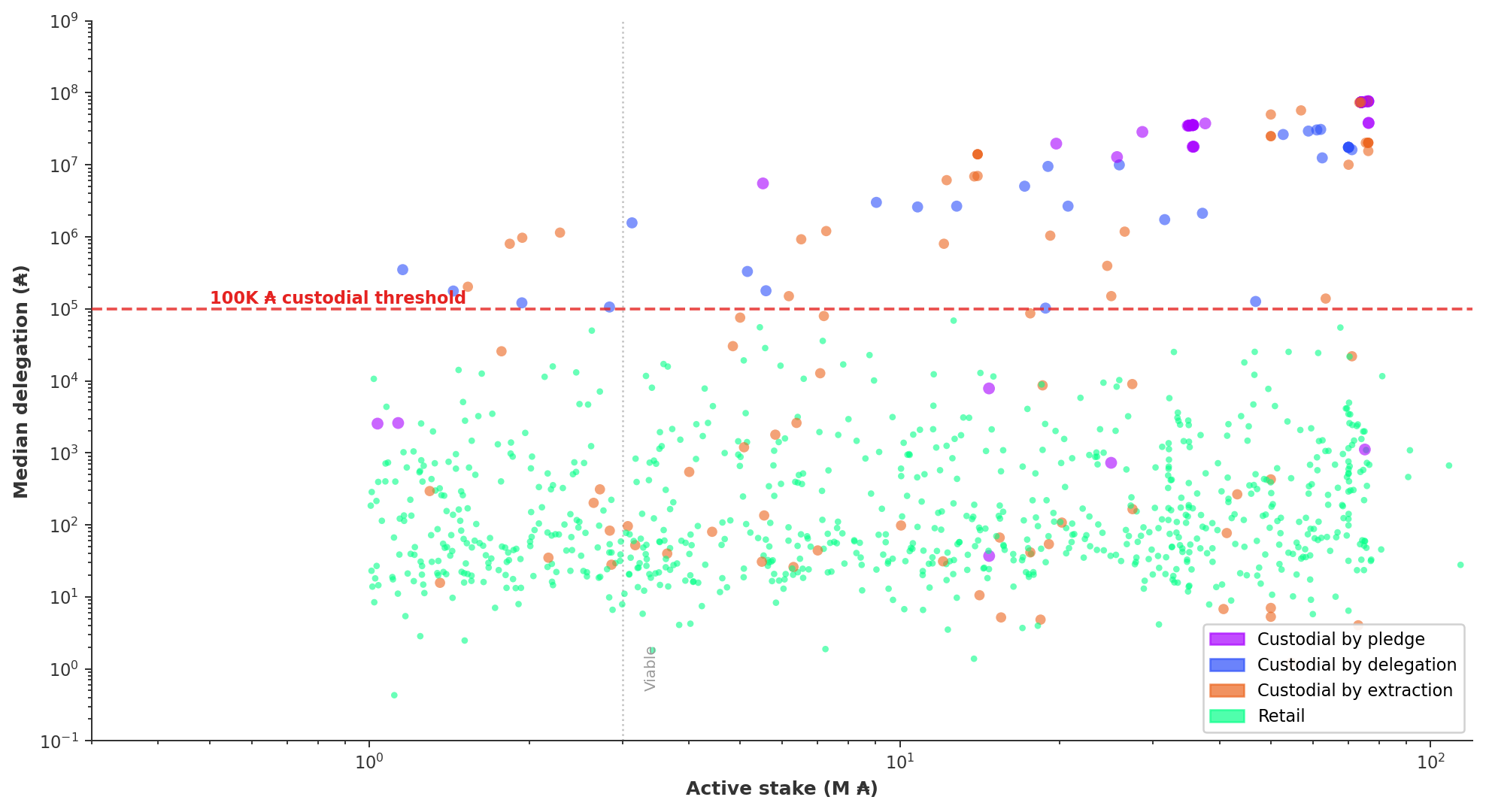

4.3.2. Custodial by delegation — the median delegation signal

The third mechanism is more subtle. Some pools appear hollow to the protocol (low owner-stake, competitive commission) but their delegation is concentrated in few, large addresses — the hallmark of operator-routed capital.

The signal is the median delegation per pool, computed from the full epoch_stake distribution (db-sync, epoch 623). The median measures the amount held by the typical delegator in the pool. When it exceeds 100K ADA — meaning the typical delegator holds more than 100K — the pool is genuinely non-retail. A delegation of 50K ₳ is already in the top 1.5% of the network; a median above 100K indicates that the majority of addresses in the pool hold capital well above any retail threshold.

At epoch 623, 28 pools (across 15 entities) exceed this threshold, carrying 0.92B ADA and 158 delegators. They split into two sub-populations:

Sub-type

Entities

Pools

Stake (B)

Delegators

Profile

Median ≥ 1M ₳

8

20

0.84

68

Whale self-delegation pools with 2–6 delegators each holding millions. Pure capital parking

Median 100K–1M ₳

8

8

0.08

90

Smaller pools where the typical delegator holds 100K–1M — a mix of high-net-worth self-delegation and small custodial arrangements

FigureOPE.4.3Per-pool median delegation against pool stake at epoch 623. 28 pools across 15 entities clear the 100K ₳ median threshold that separates custodial-by-delegation from retail — splitting into whale self-delegation pools (median ≥ 1M ₳) and smaller high-net-worth arrangements.

4.3.3. Summary

The table below continues the population decomposition from §3:

Segment

Entities

Pools

Share

Stake (B)

Stake share

Delegations

Del. share

Median deleg. (₳)

Med. entity revenue (₳/yr)

Productive total

383

733

100%

21.57

100%

1,227,281

100%

116

25,763

Custodial by pledge

10

36

3.8%

1.59

7.4%

122

<0.1%

35,579,368

1,759,252

Custodial by extraction

57

79

8.3%

2.04

9.5%

21,982

1.7%

9,009

281,831

Custodial by delegation (median ≥ 100K)

15

28

2.9%

0.92

4.3%

158

<0.1%

3,008,028

29,329

↳ Median ≥ 1M ₳

8

20

2.1%

0.84

3.9%

68

<0.1%

12,489,163

55,704

↳ Median 100K–1M ₳

8

8

0.8%

0.08

0.4%

90

<0.1%

176,666

25,023

Total custodial

79

143

15.0%

4.55

21.1%

22,262

1.7%

1,038,234

151,744

Retail market

516

809

85.0%

17.02

78.9%

1,272,836

98.3%

87

25,235

FigureOPE.4.4Productive stake decomposed by custodial mechanism versus retail at epoch 623. Custodial holds 21.1% of productive stake (4.55B ADA across 143 pools); retail captures 78.9% (17.02B ADA across 809 pools and 1.27M delegations).

The custodial segment is smaller than the mean-APD estimate suggested — 21.1% of stake, not 49.9% — because most institutional pools (Coinbase, Binance, Kiln, YUTA) are retail by their delegation median. They route large capital through few addresses, but the majority of their delegators are small retail wallets.

FromObservationOPE.O3 — 21% of productive stake is custodial — three mechanisms, three economics

Finding#1→ 21.1% of productive stake is custodial, distributed across three on-chain-detectable mechanisms.79 entities running 143 pools hold 4.55B ADA under operator-controlled delegation: custodial-by-pledge (10 entities, 36 pools, 1.59B ADA), custodial-by-extraction (57 entities, 79 pools, 2.04B ADA), and custodial-by-delegation (15 entities, 28 pools, 0.92B ADA). Each mechanism is detectable from a single observable — owner-stake share, declared commission, or per-pool median delegation — and produces a different economic outcome. Filtering them out is what isolates the genuine retail pricing market analysed downstream.

The retail market — 809 pools, 516 entities, 17.02B ADA, 1,272,836 delegators — encompasses 78.9% of productive stake and 98.3% of delegation relationships.

FromObservationOPE.O4 — The retail market is 79% of stake and the typical delegator holds 87 ₳

Finding#1→ The retail market is larger than mean-based estimates suggested: 809 pools, 516 entities, 17.02B ADA, 1,272,836 delegators. Once the three custodial mechanisms are filtered out, what remains carries 78.9% of productive stake and 98.3% of delegations. The set includes institutional operators (Coinbase, Binance, Kiln) — they qualify as retail by their per-pool median delegation rather than by their headline stake. This is the population where the pricing plan produces a genuine market outcome rather than an internal transfer.

Finding#2→ The median retail delegation is 87 ADA — and remarkably uniform across operator types. Across single-pool operators, multi-pool fleets, and institutional brands like Coinbase and Binance, the median sits in a tight 45–962 ADA band. The typical delegator is small everywhere: the operator type does not select for delegator size. Whatever else differs between hollow MPOs and single-pool operators, the customer they serve is the same person. This homogeneity is what makes the 0.39 pp net-return spread (§4.4) effectively flat for the audience that actually receives it.

FromObservationOPE.O3 — 21% of productive stake is custodial — three mechanisms, three economics

Finding#2→ The median delegation separates custodial from retail by four orders of magnitude. Custodial pools: 1,038,234 ₳ median. Retail pools: 87 ₳ median. A delegation of 50K ₳ is already in the top 1.5% of all delegations on the network.

Finding#3→ Each custodial mechanism produces a different economic outcome. Custodial-by-pledge entities earn 1,759,252 ₳/yr median — they fund their own pools and capture 100% of rewards. Custodial-by-extraction entities earn 281,831 ₳/yr — privatisation commission extracts from pools whose delegators have not re-delegated. Custodial-by-delegation entities earn 29,329 ₳/yr — these are small whale pools, not institutional revenue engines. The three mechanisms share the label "custodial" but produce economics that span two orders of magnitude.

4.4. Operator profitability versus delegator return

The effective price is only meaningful in the retail market — where the operator does not control the delegator addresses. In custodial pools, the "price" is an internal transfer; it carries no information about market competition. This section analyses the 809 retail pools (516 entities, 17.02B ADA, 1,272,836 delegators) identified in §4.3 — Custodial versus retail.

The central question is what the pricing plan produces for each side of the market. The operator earns a revenue (the operator take, annualised in ₳/year); the delegator receives a return (the net ROS, after fees).

If the mechanism worked as intended, these two quantities would be linked: operators who charge more would earn more, and delegators would see a meaningful ROS difference that informs their delegation choice.

The table below tests this assumption.

Operator type

Entities

Pools

Delegators

Del. share

Stake (B)

Median deleg. (₳)

Flat fee

Commission

Effective price

Gross ROS

Net ROS

Med. entity revenue (₳/yr)

Drag (pp)

Reward share

Hollow single-pool

414

414

399,089

31.4%

5.29

78

7.0%

2.1%

9.1%

2.48%

2.08%

24,965

0.47pp

31.1%

↳ Sub-reliable (<3M)

155

155

52,557

4.1%

0.28

72

47.5%

0.8%

48.3%

3.89%

2.04%

24,820

1.59pp

1.6%

↳ Healthy (3–38.5M)

214

214

221,279

17.4%

2.44

74

8.3%

2.9%

11.2%

2.35%

2.03%

26,652

0.32pp

14.3%

↳ Large healthy (38.5–62M)

29

29

91,238

7.2%

1.47

125

1.7%

1.4%

3.0%

2.37%

2.31%

31,757

0.06pp

8.7%

↳ Near-saturation (62–77M)

16

16

34,015

2.7%

1.11

962

1.2%

1.5%

2.7%

2.40%

2.34%

27,244

0.04pp

6.5%

Hollow MPO

57

330

838,593

65.9%

10.95

107

3.0%

3.3%

6.3%

2.33%

2.18%

124,100

0.14pp

64.4%

↳ 2-pool

17

34

102,253

8.0%

1.30

91

2.5%

1.3%

3.9%

2.27%

2.19%

68,667

0.10pp

7.7%

↳ 3–5 pool

24

94

271,460

21.3%

2.77

78

3.3%

1.6%

5.0%

2.33%

2.19%

132,851

0.14pp

16.3%

↳ 6–10 pool

9

67

112,454

8.8%

2.37

67

2.7%

3.8%

6.5%

2.38%

2.18%

263,959

0.15pp

13.9%

↳ 11+ pool

7

135

352,426

27.7%

4.51

292

3.0%

4.7%

7.7%

2.31%

2.15%

1,035,496

0.20pp

26.5%

Balanced

41

42

15,844

1.2%

0.20

45

17.8%

1.4%

19.2%

3.06%

1.98%

23,513

1.06pp

1.2%

↳ Single-pool sub-reliable (<3M)

27

27

5,041

0.4%

0.04

45

49.4%

1.0%

50.4%

3.70%

1.95%

23,513

2.19pp

0.3%

↳ Single-pool healthy (≥3M)

13

13

4,051

0.3%

0.10

56

11.2%

1.1%

12.3%

2.41%

2.14%

17,199

0.43pp

0.6%

↳ MPO

1

2

6,752

0.5%

0.06

25

5.2%

2.0%

7.2%

2.40%

2.22%

101,849

0.17pp

0.4%

Retail total

516

809

1,272,836

100%

17.02

87

4.4%

2.9%

7.4%

2.45%

2.11%

25,235

0.41pp

100%

The table reads left to right: operator type → population → pricing channels (flat fee + commission as % of pool reward) → what the pool produces (gross ROS) → what the delegator receives (net ROS) → what the operator earns (median entity revenue annualised) → the cost to the delegator (Drag (pp)) → share of total retail pool rewards.

Three observations emerge from this decomposition.

Delegators pay 18× more for the same return — and operators who charge the most earn the least. A delegator in a sub-reliable pool pays 48.3% effective price for 2.04% net return; a delegator in a near-saturation pool pays 2.7% for 2.34%. The price differs by 18×; the return by 0.30pp.

On the operator side, the sub-reliable operator absorbs 48.3% of pool rewards but earns 24,820 ₳/yr; an 11+ pool MPO absorbs 7.7% but earns 1,035,496 ₳/yr — 42× more revenue at 6× less effective price.

FromObservationOPE.O5 — Delegators pay 18× more for the same return

Finding#1→ Delegators pay 18× more for the same return. A delegator in a sub-reliable pool pays 48.3% effective price and receives 2.04% net return. A delegator in a near-saturation pool pays 2.7% and receives 2.34%. The effective price varies by 18× across pool tiers; the return varies by 0.30 percentage points. The pricing plan does not produce a signal that delegators can act on.

FromObservationOPE.O6 — Stake pool operator profitability ranges from 24K to 1M ₳/yr — operators who charge the most earn the least

Finding#1→ Operators who charge the most earn the least. A sub-reliable single-pool operator absorbs 48.3% of pool rewards but earns 24,820 ₳/yr. An 11+ pool MPO absorbs 7.7% but earns 1,035,496 ₳/yr — 42× more revenue at 6× less effective price. The flat fee penalises small-pool delegators without compensating the operators who run those pools.

155 sub-reliable single-pool operators absorb 48.3% of their pools' output as effective price but operate on just 1.6% of total retail rewards. Meanwhile, hollow MPOs earn 3–42× more (69k–1M ₳/yr) at a lower effective price (3.9–7.7%) — the scaling is horizontal (more pools) rather than vertical (higher extraction).

FromObservationOPE.O6 — Stake pool operator profitability ranges from 24K to 1M ₳/yr — operators who charge the most earn the least

Finding#2→ Multi-pool operator revenue scales horizontally, not vertically. Adding pools — not raising prices — is the path to higher entity income. The 11+ pool bracket captures 26.5% of all retail rewards through just 7 entities, while the median entity revenue moves from ~25K ₳/yr at the single-pool tier to ~1.04M ₳/yr at the 11+ pool tier. The pricing channels (flat fee, commission) actually fall as fleet size rises. Fleet expansion, not price discovery, is the operating economic strategy in the retail market.

The reward share column makes the structural imbalance explicit:

57 hollow MPOs operate on 64.4% of the retail economy;

414 hollow single-pool operators share 31.1%;

41 balanced operators share 1.2%.

FromObservationOPE.O6 — Stake pool operator profitability ranges from 24K to 1M ₳/yr — operators who charge the most earn the least

Finding#3→ 414 hollow single-pool operators share 31.1% of retail rewards; 41 balanced operators share 1.2%. The bulk of single-pool operators — 414 entities with no MPO fleet and minimal owner-stake — collectively earn less than a third of the retail pool — averaging the ~25,000 ADA/yr floor that does not cover labour at current ADA price. The 41 balanced operators that do pledge meaningfully are the squeezed middle: they bear the flat-fee drag (1.06 pp) without the fleet leverage that compensates hollow MPOs. The reward share is consistent with the operator-distribution shape: a heavy-tailed MPO economy on top, a thin balanced layer in between, and a long flat single-pool tail.

Delegator returns are near-identical regardless of operator type. Net ROS ranges from 1.95% (balanced single-pool sub-reliable) to 2.34% (hollow single-pool near-saturation) — a 0.39 percentage-point spread across the entire retail market. The flat fee creates large differences in effective price without producing corresponding differences in delegator return.

FromObservationOPE.O5 — Delegators pay 18× more for the same return

Finding#2→ Net return converges to a 1.95–2.34% band across the entire retail market. The convergence is independent of effective price, operator type, and pool size: a 18× difference in price and a 42× difference in operator revenue compress to a 0.39 pp spread on the delegator side. A signal that narrow cannot discipline pricing — a delegator who switches across the entire productive retail market gains, at most, three-tenths of a percentage point of yield, well below the noise floor of single-epoch block-production variance. The accountability loop the mechanism assumes does not close.

Sub-reliable pools generate the highest gross ROS (3.70–3.89% — the reward curve is generous per ADA at small pool sizes) but the flat fee erases the surplus: 1.59–2.19pp of drag. Above the production threshold, drag collapses to 0.04–0.43pp. For MPOs, drag rises gently with fleet size (0.10–0.20pp) as the commission channel takes over from the flat fee.

The delegator cannot meaningfully distinguish operators by return.

Delegation concentration does not follow return.65.9% of retail delegators sit in hollow MPO pools at 2.18% net ROS, while hollow single-pool near-saturation pools offer 2.34% — 0.16pp more — and hold only 2.7% of delegators.

The 11+ pool MPOs concentrate 27.7% of all retail delegators (352,426) on 26.5% of rewards. This concentration reflects visibility and wallet-integration defaults, not yield optimisation.

FromObservationOPE.O7 — Delegation follows visibility, not return

Finding#1→ Delegation follows visibility, not return. 65.9% of retail delegators sit in hollow MPO pools despite hollow single-pool near-saturation pools offering 0.16pp more. The return spread across the retail market (0.39 percentage points) is too narrow to inform delegation decisions.

Finding#2→ The pledge premium is negative in the retail data. Balanced pools (genuine pledge commitment) deliver 1.98% median net return vs 2.08% for hollow. The flat fee drag (1.06pp for balanced vs 0.47pp for hollow single-pool operators) overwhelms the pledge benefit from the reward curve. The incentive mechanism's core assumption — that pledge commitment translates to better delegator outcomes — does not hold.

Entity

Type

Pools

Delegators

Stake (M)

Effective price

Net ROS

Drag (pp)

Revenue (₳/yr)

Everstake

11p-MPO

11

264,997

566.6

5.4%

2.17%

0.13pp

717,323

AWP / Atomic Wallet

3p-MPO

3

83,802

47.5

11.5%

2.06%

0.27pp

127,112

BERRY

single-pool

1

22,053

32.9

4.7%

2.48%

0.12pp

35,941

Emurgo

8p-MPO

8

15,334

269.4

3.3%

2.31%

0.08pp

210,097

Everstake dominates the retail market: 264,997 delegators (21% of retail) across 11 pools at 5.4% effective price — a competitive deal. AWP / Atomic Wallet shows the wallet-integration effect: 83,802 delegators routed by the app into 3 pools at 11.5% effective price and the lowest net ROS among top entities (2.06%). BERRY is the counter-example — a single-pool operator that attracts 22,053 delegators at the highest net ROS in the table (2.48%) through community visibility rather than platform integration. The three entities illustrate three delegation mechanisms: institutional routing (Everstake), app defaults (AWP), and community reputation (BERRY).

The figures below synthesise the retail market economics.

FigureOPE.4.5Entity revenue (log scale) against net delegator ROS across the retail market. The productive population (Panel B) shows net ROS in a tight 2.0–2.5% band across a 52× spread in operator revenue — the pricing plan is invisible to the delegator above the production threshold.

Panel A shows the full retail market. The x-axis is entity revenue (₳/year, log scale); the y-axis is net ROS (%). Two vertical clusters are visible at 12,410 ₳/yr and 24,820 ₳/yr — these are the two flat fee floor values (170 ₳ and 340 ₳) annualised (× 73 epochs). Sub-reliable operators (red) are pinned to these floor values: their revenue is almost entirely the flat fee, and the commission adds negligible income. The scatter tail below 2% ROS is exclusively sub-reliable — these are pools where the flat fee absorbs so much of the reward that delegator return degrades visibly.

Panel B removes the sub-reliable population and zooms to the productive market (≥3M ADA). The picture sharpens: net ROS sits in a tight band between 2.0% and 2.5% across the entire revenue range from 25K to 1.3M ₳/yr — a 52× spread in operator revenue for a 0.5 percentage-point spread in delegator return. The pricing plan is invisible to the delegator in the productive market.

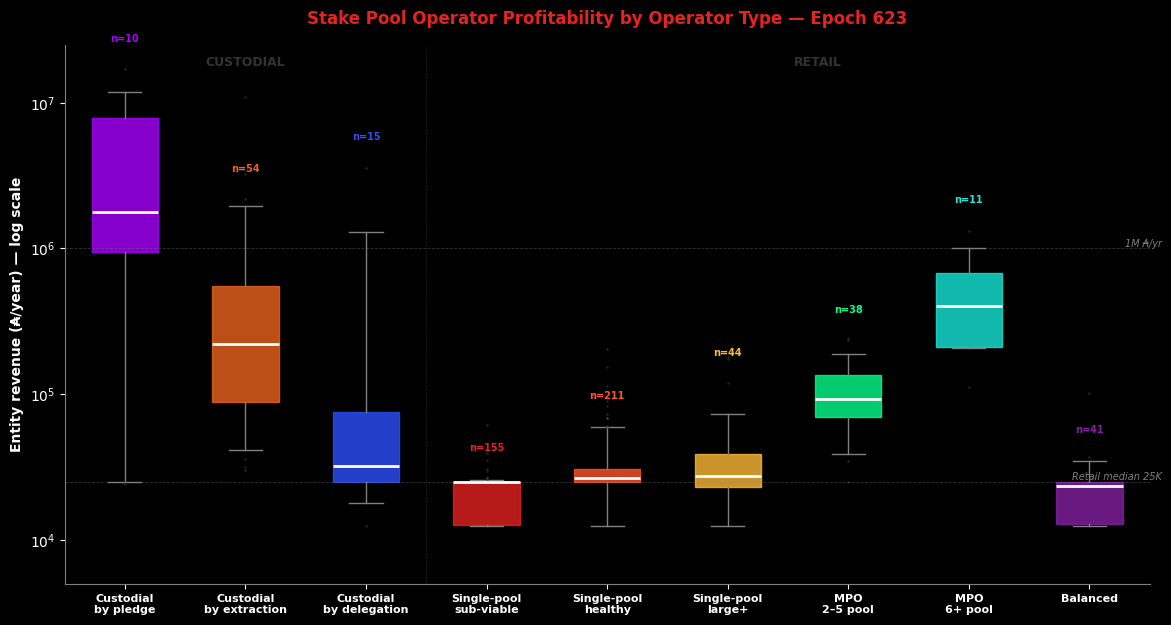

The full profitability distribution. The figure below shows the entity-level revenue distribution across all operator types — custodial and retail — on a logarithmic scale. Each box spans the interquartile range (P25–P75); whiskers extend to P5–P95; dots are outliers.

FigureOPE.4.6Entity-level revenue distribution across operator types on a logarithmic scale. Custodial-by-pledge entities earn ~1.8M ₳/yr median while single-pool retail operators are compressed near 25K ₳/yr regardless of pool size; MPO revenue scales with fleet size from ~94K ₳/yr (2–5 pools) to ~402K ₳/yr (6+ pools).

The visual makes three patterns immediately legible. First, the custodial segment spans three orders of magnitude internally: custodial-by-pledge entities (n=10) earn 1.8M ₳/yr median with a range up to 16.9M, while custodial-by-delegation (n=15) clusters near the retail baseline at 32K. Second, single-pool retail operators (sub-reliable, healthy, large+) are compressed into a narrow band around 25K ₳/yr — regardless of pool size, the revenue barely moves. Third, MPO revenue scales with fleet size: 2–5 pool MPOs earn ~94K, 6+ pool MPOs earn ~402K. The jump from single-pool to 2-pool is the most significant transition in operator economics — it roughly triples entity revenue.

4.5. Is operator revenue competitive? — a market benchmark

A reward mechanism that underpays its operators relative to their costs and opportunity cost will eventually lose them. A mechanism that overpays has room to optimise.

The question is where Cardano's operator economics sit on that spectrum.

4.5.1. The cost of operating a pool — infrastructure and labour

A Cardano stake pool requires, at minimum, one block-producing node and two relay nodes, each running 24/7 with adequate CPU, RAM (16–32 GB), NVMe storage, and bandwidth (~1 GB/hour). The operator is responsible for uptime, security patching, key rotation, and monitoring. The typical deployment uses either bare-metal servers or cloud VPS instances across geographically distinct locations.

Cost component

Monthly estimate (USD)

Annual estimate (USD)

Block producer (VPS or bare metal)

\$40–80

\$480–960

Relay nodes (×2, geographically separated)

\$60–160

\$720–1,920

Monitoring, DNS, backups

\$10–30

\$120–360

Infrastructure total

\$110–270

\$1,320–3,240

Estimates based on common VPS providers (Hetzner, OVH, Contabo, AWS Lightsail) as of Q1 2026. Bare-metal setups at the lower end; multi-region cloud at the upper end. Excludes operator labour.

At ADA ≈ \$0.25 (April 2026), the infrastructure floor translates to approximately 5,300–13,000 ₳/year. This is the minimum a pool must generate to avoid operating at a cash loss — before any compensation for the operator's time.

Infrastructure is the smaller cost. The binding constraint is the operator's time.

Running a pool is not passive income: it demands monitoring, upgrades (node releases, hard forks), security management, community engagement, and — increasingly — governance participation (DRep voting, parameter discussions). The workload varies, but a conscientious single-pool operator reports 5–15 hours per month in steady state, with spikes during hard forks or incidents.

The relevant benchmark is the market rate for comparable skills. A stake pool operator performs a subset of what the industry calls DevOps or Site Reliability Engineering (SRE): infrastructure provisioning, monitoring, incident response, and system upgrades on Linux servers running a blockchain node.

Role

Hourly rate (USD)

Source

DevOps / System Administrator

\$43–67

ZipRecruiter, Salary.com (2026)

SRE / DevOps Engineer

\$64–78

ZipRecruiter, PayScale (2026)

Senior DevOps Engineer

\$72–86

Salary.com (2026)

Even at the lower end of the range (\$43/hr for a junior DevOps role), 10 hours per month of operator labour is worth \$430/month or \$5,160/year — approximately 20,600 ₳/year at current prices.

Combining infrastructure and a conservative labour estimate:

Component

Annual cost (₳, at \$0.25)

Infrastructure (mid-range)

~8,000

Operator labour (10 hrs/mo × \$43/hr)

~20,600

Total cost floor

~28,600

This is a lower bound. It assumes the cheapest infrastructure tier, the lowest market rate for the relevant skillset, and minimal monthly hours. An operator running redundant infrastructure across multiple regions, maintaining a community presence, and participating in governance easily exceeds 20 hours per month — doubling the labour component.

4.5.2. Revenue versus cost — a price-sensitivity view

Infrastructure and labour are denominated in fiat; operator revenue is denominated in ADA. The economic viability of pool operation is therefore a function of two variables: the ₳ revenue (set by the mechanism) and the ADA/USD exchange rate (set by the market). The §4.4 — Operator profitability versus delegator return revenue data maps directly onto this cost framework. The table below holds the first constant — each tier's median ₳/yr from §4.4 — Operator profitability versus delegator return — and varies the second across five price points spanning a 40× range.

Operator tier

Revenue (₳/yr)

@\$0.25

@\$0.50

@\$1.00

@\$5.00

@\$10.00

Sub-reliable single-pool

24,820

\$6,205

\$12,410

\$24,820

\$124,100

\$248,200

Healthy single-pool (3–38.5M)

26,652

\$6,663

\$13,326

\$26,652

\$133,260

\$266,520

Large healthy single-pool (38.5–62M)

31,757

\$7,939

\$15,879

\$31,757

\$158,785

\$317,570

Near-saturation single-pool (62–77M)

27,244

\$6,811

\$13,622

\$27,244

\$136,220

\$272,440

2-pool MPO

68,667

\$17,167

\$34,334

\$68,667

\$343,335

\$686,670

3–5 pool MPO

132,851

\$33,213

\$66,426

\$132,851

\$664,255

\$1,328,510

6–10 pool MPO

263,959

\$65,990

\$131,980

\$263,959

\$1,319,795

\$2,639,590

11+ pool MPO

1,035,496

\$258,874

\$517,748

\$1,035,496

\$5,177,480

\$10,354,960

Reference cost floor: ~\$2,000/yr infrastructure (mid-range) + ~\$5,160/yr labour (10 hrs/mo × \$43/hr) = ~\$7,160/yr. An operator is competitive when revenue covers this floor with meaningful surplus.

The table reveals that the mechanism's economic story changes entirely depending on which column the reader inhabits.

At \$0.25 (April 2026 spot), no single-pool operator covers the cost floor. The median single-pool revenue of ~\$6,500 falls short of the conservative \$7,160 estimate — the operator works at a net loss before accounting for any return on time beyond the bare minimum. The 2-pool MPO tier (\$17,200) is the first to clear the threshold with margin, but the income remains modest. Only the 6+ pool MPOs earn what would qualify as a professional income.

At \$0.50, single-pool operators cross the cost floor comfortably (~\$12,500) but the surplus (~\$5,300 above costs) compensates roughly 10 hours per month at \$43/hr — the operator breaks even on the minimum estimate but earns nothing beyond it. The 2-pool MPO tier (\$34,300) begins to look like a viable part-time income. The 3–5 pool tier (\$66,400) reaches a full-time junior-engineer salary in most markets.

At \$1.00, the picture inverts. Single-pool revenue (~\$25,000) covers costs and leaves ~\$18,000 of surplus — a meaningful part-time income or a modest full-time salary in lower-cost markets. The 2-pool MPO (\$68,700) earns a comfortable full-time salary. The 3–5 pool tier (\$132,900) reaches senior-engineer compensation. Pool operation becomes an economically rational activity at every tier.

At \$5.00, single-pool operation pays ~\$124,000 — a senior professional salary in most geographies. The 2-pool MPO earns \$343,000. The economics are no longer about survival but about whether the mechanism overpays relative to the work required. At this price, the incentive design functions as intended: operators are well compensated, and the market can afford to compete on service quality rather than subsistence.

At \$10.00, even the sub-reliable single-pool tier earns \$248,000 — more than enough to fund a dedicated operations team. The 11+ pool MPO generates over \$10M/yr. The mechanism's revenue distribution remains structurally flat (the sub-reliable pool still earns 24× less than the 11+ pool MPO), but the absolute level renders the flatness tolerable: every tier is profitable, and the question shifts from "can the operator survive?" to "is the mechanism's rent distribution equitable?"

The pattern across columns is stark.

At current prices, no single-pool operator in the retail market earns a competitive wage for their labour. The break-even point for competitive compensation sits at the 2-pool MPO tier — and even there, the income is modest.

But the mechanism itself is not structurally broken; it is structurally contingent. The same ₳ revenue that produces a net loss at \$0.25 produces a professional salary at \$1.00 and a generous one at \$5.00.

The protocol's operator economics are hostage to a single exogenous variable.

4.5.3. Cross-chain comparison — the validator cost spectrum

Cardano's operator economics are unusually lean relative to other PoS networks. The comparison is instructive because it reveals, chain by chain, that the small-operator viability problem is universal — but the binding constraint differs in each design, and so does the structural response.

Network

Infra cost (USD/yr)

Capital / entry requirement

Ongoing fixed costs

Typical small-operator revenue

Viable?

Cardano (single pool)

\$1,300–3,200

None (pledge optional)

None

~\$6,250/yr (25K ₳ at \$0.25)

No — labour uncompensated

Cardano (3–5 pool MPO)

\$4,000–10,000

None

None

~\$33,200/yr (133K ₳)

Marginal — part-time

Ethereum (solo validator)

\$500–2,000

32 ETH locked (~\$64,000)

None

~\$2,000–2,500/yr (yield on 32 ETH)

No — capital-intensive, low return

Solana (validator)

\$10,000–18,000

Stake account recommended

Vote tx ~400 SOL/yr (~\$32,000)

Variable, commission-dependent

Marginal — high fixed costs

Polkadot (validator)

\$3,000–6,000

10,000 DOT self-stake (~\$40,000)

None

10% min commission on nominated stake

Yes — if nominated into active set

Cosmos Hub (validator)

\$2,000–5,000

Self-delegation required