The Shelley-era Delegation and Incentives Design Specification (SL-D1) defined the economic rules that were to guide Cardano toward a stable, decentralised equilibrium of $k$ well-funded stake pools.

Five years of mainnet operation have produced a settled landscape that diverges from that design in specific, observable ways. This document is the empirical record of those divergences.

The goal is to make them explicit and structural — to read each one not as a parameter tuned to the wrong value, but as the predictable outcome of rules whose surrounding context (governance, smart contracts, fee economy, reserve runway) has shifted since 2019.

Every divergence is then named as a structural problem the next reward mechanism must address. The substantive output — the 9 induced problems the diagnostic surfaces — lives on the dedicated Induced Problems page; what follows here is the evidence-and-induction record behind it.

The widget above places this document at Stage 02 of the V2 work — the empirical foundation. Stage 01 is the companion The Intended Game, the normative baseline of what V1 was supposed to produce — the diagnostic measures every divergence against it and inducts the structural problems that:

- Induced Problems (Stage 03) carries forward as proto-CPSs,

- Solution Design (Stage 04) organises into directions and milestones,

- and the CIPs Evaluation (Stage 05) reads the four pre-existing reward CIPs against.

The approach is to walk the SL-D1 reward pipeline stage by stage, applying the same analytical arc at each:

design intent → mainnet confrontation → problem induction → CPS check

Every claim is anchored to a canonical observation code (TRE.O#, POL.O#, OPE.O#, CEN.O#) tied to a specific finding in one of four sub-reports. Theory enters only where the formula or the security model is being characterised; everywhere else, the load is carried by mainnet observation.

The pipeline is read as a single dependency chain rather than a set of independent layers — the epoch budget sets the ceiling, the reward curve allocates within it, and the fee structure determines what actually reaches operators and delegators. A fix at one stage can be undone by a distortion at another.

The four sub-reports that carry the per-stage evidence, threaded into the synthesis below:

- Treasury & Pool Pots Distribution — epoch-pot assembly, reserve trajectory, fee analysis, return-to-reserve mechanism. Threaded into §1.1 — Treasury & Pool Pots Distribution.

- The Pools Pot Distribution Gaps — reward curve formulas, distribution efficiency, pool landscape, entity analysis. Threaded into §1.2 — Pools Distribution.

- The Operator's Cut — intra-pool split formulas, pricing-plan landscape, custodial/retail boundary, operator profitability, delegator-yield trajectory. Threaded into §1.3 — Operator / Delegator Distribution.

- The Staking Census — ADA supply decomposition, operator and delegator landscape, non-participant decomposition, transaction-submitter dynamics. Threaded into §2 The Player Populations.

The synthesis itself follows the pipeline in three movements:

- §1 The Reward Flow decomposes the SL-D1 pipeline stage by stage with the shared analytical arc.

- §2 The Player Populations grounds the pipeline observations in the structural dynamics of operators, delegators, non-participants, and transaction submitters.

- §3 The ₳/Fiat Money Constraint Layer sets the boundary conditions within which any solution must operate.

Table of Contents

1. The Reward Flow

The SL-D1 reward pipeline transforms a finite reserve into per-participant rewards through three sequential stages:

- Epoch-budget assembly (Treasury & Pool Pots Distribution);

- Pool-level distribution (Pools Distribution);

- Operator/delegator split (Operator / Delegator Distribution).

Each stage embeds design choices that constrain the next. The analysis follows a common arc at every stage — design intent, mainnet confrontation, problem induction — so that the structural failures compound visibly across the full pipeline rather than appearing as isolated parameter issues.

The three stages are not independent layers that can be tuned in isolation. The epoch budget (Treasury & Pool Pots Distribution) sets the ceiling; the reward curve (Pools Distribution) allocates within it; the fee structure (Operator / Delegator Distribution) determines how much of each allocation reaches operators and delegators.

A failure at any stage propagates downstream, and a fix at one stage can be undone by a distortion at another.

The pipeline must be read — and ultimately redesigned — as a single system.

1.1. Treasury & Pool Pots Distribution

1.1.1. Flow Overview

Before any individual pool receives rewards, the protocol must first answer one question: how much ADA is available for distribution this epoch?

This stage assembles the epoch pot from three on-chain sources — transaction fees, non-refundable deposits, and a monetary-expansion draw from the reserve — then splits it in two. A fixed share goes to the treasury; the remainder becomes the pools pot, the total budget that Pools Distribution will allocate across individual pools.

Two design choices embedded at this stage matter for the rest of the analysis:

-

Cooperative-behaviour gate. The monetary-expansion draw is scaled by the ratio of blocks actually produced to blocks expected. If pools collectively miss slots, the entire epoch pot shrinks. The rule discourages sabotage but also ties the pot to aggregate network health.

-

Fixed split rule. The treasury-to-pools ratio is a protocol constant ($\tau$), not a function of network activity or reserve level. It does not adapt as the balance between fees and expansion shifts over time.

Formulas. The epoch-pot assembly and treasury/pools split formulas — from the original SL-D1 notation through a reader-friendly rewrite to mainnet parameterisation — live in the dedicated sub-report:

Treasury & Pool Pots Distribution— Flow Overview.

Mainnet behaviour from Shelley through epoch 623 is documented in four observations below. They are structural to the layer itself: no existing CIP targets this stage — every proposal operates downstream — so the evidence here sets the sustainability context within which all downstream reforms must land.

- TRE.O1The epoch pot rests on a single source — and that source has crossed its half-life

- TRE.O2The reserve has crossed its half-life — the budget is on an exponential decay schedule

- TRE.O3Less than half of the pools pot reaches operators and delegators — the rest props up the reserve as a side effect of low participation

- TRE.O4The two parameters that govern this whole layer have never been adjusted

1.1.3. Problem Induction → Funding the Protocol Without a Reserve

Each observation above constrains what the system can do. Read together, they reveal what it cannot do.

The epoch pot is funded almost entirely by monetary expansion from the reserve (TRE.O1). That reserve is finite and has already crossed its half-life (TRE.O2).

Transaction fees — the only sustainable alternative — cover ~0.19% of the pot today, and even at full realistic throughput would reach only ~1.3% (TRE.O1). Closing this gap requires fee revenue to grow by ~100× (two orders of magnitude), which in turn implies a throughput upgrade (Leios), a structural increase in transaction demand, and higher per-tx pricing (tiered or congestion-based) — none of which is on a defined timeline.

Meanwhile, the two parameters governing the draw ($\rho$, $\tau$) have never been reviewed since Shelley launch (TRE.O4), and no governance process exists to do so.

These constraints compose into a single structural problem: the reward system has no viable path from reserve-funded to fee-funded sustainability.

The reserve is depleting on a known schedule, the only alternative revenue source is orders of magnitude too small, and the parameters governing the transition have never been subject to governance.

This is not a failure of any individual parameter — it is a design gap at the epoch-budget layer. No protocol-level or governance-level instrument currently exists to manage this transition.

TRE.O3 — the ~44% distribution efficiency — is not a problem at this layer. It is a consequence of participation levels, which are shaped by incentives defined downstream (Pools Distribution, Operator / Delegator Distribution).

But it interacts directly with the sustainability problem: activating inactive ADA would improve distribution efficiency while accelerating reserve consumption. Any solution to the epoch-budget problem must account for this tension — and any change to the downstream incentive structure (Pools Distribution, Operator / Delegator Distribution) that affects participation will feed back into reserve dynamics here.

CPS identified. No Cardano Problem Statement (CPS) has been formally written for this problem. The CIP governance process requires that solutions (CIPs) be scoped against a well-defined problem statement (CPS). This foundational sustainability problem has remained formally unstated.

This analysis identifies the gap and names the missing problem statement — Funding the Protocol Without a Reserve — derived from the mainnet evidence in the dedicated Treasury & Pool Pots Distribution sub-report.

The epoch budget sets the ceiling for everything that follows. But how that budget reaches individual participants — and whether the distribution mechanism itself works as intended — is a separate question. That is the subject of Pools Distribution.

1.2. Pools Distribution

1.2.1. Flow Overview

This stage takes the pools pot ($PoolsPot^{\text{epoch}}$) produced by Treasury & Pool Pots Distribution and distributes it across individual pools. The output is a per-pool allocation ($PoolPot^{\text{actual}}_i$) that feeds into Operator / Delegator Distribution.

For each pool $i$, the protocol performs three steps:

-

Saturation clipping. Both total stake ($\sigma_i$) and pledge ($s_i$) are capped at the saturation threshold $z_0 = 1/k$. The cap prevents any single pool from capturing a disproportionate share.

-

Reward-curve evaluation. A reward function $f$ computes the pool's optimal allocation from its clipped stake and pledge. The curve has two components — a base stake term (proportional to delegation) and a pledge-bonus term (nonlinear, governed by $a_0$) — the latter intended to reward operator commitment ("skin in the game").

-

Performance adjustment. The optimal allocation is scaled by apparent performance $\bar{p}_i$ to produce the actual allocation. Pools that miss blocks receive less. If the registered pledge is not met, the allocation is zeroed entirely.

Any rewards not distributed — because $\sum_i \hat{f}_i < R$ — return to the reserve, the mechanism behind TRE.O3 in Treasury & Pool Pots Distribution.

Two design choices matter for the rest of the analysis:

-

Pledge sensitivity via $a_0$. The parameter $a_0$ controls how much additional reward a pool can earn through pledge. At $a_0 = 0.3$, the pledge bonus represents at most ~23% of the optimal allocation. Whether this is sufficient to meaningfully incentivise pledge is a central question at this layer.

-

Uniform saturation threshold. All pools share the same cap $z_0 = 1/k$. No mechanism differentiates saturation by pledge level or pool characteristics.

Formulas. The pool-level reward formulas — from the original SL-D1 reward curve through the normalised saturation-coordinates rewrite to mainnet parameterisation — live in the dedicated sub-report:

The Pools Pot Distribution Gaps— Problem Induction → Closing the Consensus Incentive Gap.

Mainnet behaviour over epochs 208–618 (latest complete reward epoch at 616) is documented in seven observations below, organised in two arcs.

POL.O1–POL.O4 are structural to the layer itself — distribution efficiency, pledge unfairness, the three thresholds, and the sub-block tail. POL.O5–POL.O7 characterise the entity landscape and the incentive-responsive arena that the reward curve actually addresses. The participation gap (POL.O1) and the capital constraint (POL.O5) trace back to the same upstream conditions documented at Treasury & Pool Pots Distribution — they set the playing field within which the reward curve operates.

- POL.O1Participation gap and unused pledge-incentive budget return 54% of the pool pot to reserve

- POL.O2Pledge is unused at scale and structurally unfair across pool sizes

- POL.O3Three structural thresholds shape pool space: production (physics), viability (economics), saturation (formula)

- POL.O4A 73% sub-block tail (useless to consensus) and a 27% productive segment (unreadable without entity-level investigation)

- POL.O583 multi-pool operators control 76.7% of productive stake — and almost none of them pledge

- POL.O6Only 284 productive single-pool operators remain — and almost none of them pledge (like MPOs)

- POL.O7The pledge mechanism reaches only 36% of stake — and the 64% outside it splits into three populations no single parameter can pull back in

1.2.3. Problem Induction → Closing the Consensus Incentive Gap: The pledge paradox & Non-Participant problem

The reward curve is the protocol's only tool for shaping the operator ecosystem that secures consensus, and on Cardano mainnet it is doing that job — but not as optimally as it was designed to.

Its purpose is to produce an incentive-compatible equilibrium: rational operators and delegators reproducing decentralisation, Sybil resistance, and accountability without being told to.

The chain runs, blocks are produced, rewards flow — but the equilibrium the participants have settled into is not the one the curve was designed to converge toward.

Three headline numbers measure the size of the gap:

- 54% of the pool pot returns to reserve unused — POL.O1.

- The incentive-responsive field holds only 36% of active stake — POL.O7.

- The dominant operator strategy is to minimise pledge, not maximise it — POL.O2.

Two structural failures stack underneath those numbers.

Failure 1 — The playing field is half the size $k = 500$ assumed. At 56.5% participation, only 282 pools could ever saturate, and the saturation cap binds for just 8 of them (POL.O3). No formula change at this layer can close that gap; it requires upstream intervention to bring inactive ADA into delegation.

Failure 2 — Inside that smaller field, the game does not converge toward the intended equilibrium. The curve's theoretical optimum is a fully-pledged private pool with no delegator (POL.O2) — economically irrational versus passive delegation. On the way there, the progression that should reward growing commitment fails on two layers:

- The pledge signal is invisible — the bonus adds ~0.006% at median pledge, undetectable to delegators (POL.O2).

- Entry is a cliff, not a ramp — the viability threshold sits at ~3M ADA, and below it 73% of pools sit unviable (POL.O3).

The dominant strategy at every level — entry, progression, endgame — is therefore the opposite of what consensus security requires.

The formal game-theoretic properties of the mechanism were established in Reward Sharing Schemes for Stake Pools (Brünjes, Kiayias et al., 2020), which proves that $k$ pools is a Nash equilibrium under stated assumptions, and translated into protocol-level formulas in SL-D1. Neither document, however, provides a narrative description of the game as it should play out — the players, their motivations, how they enter and progress, and the equilibrium they should converge toward — without which evaluating whether the mechanism works means guessing at what working would look like. That narrative description is produced in the dedicated companion document The Intended Game, and the operator-perspective trajectory in Divergence with intended equilibrium follows it step by step.

The visible damage is consistent with this diagnosis: 95.6% of the pledge-bonus budget returns to reserve unused (POL.O1), the single-pool operator base has collapsed to 284 productive single-pool operators once MPO fleets are removed (POL.O6), and structural populations totalling 7.4B ADA cannot pledge by architectural constraint (POL.O5) — the dominant capital pool sits outside the incentive arena entirely.

CPS identified. No Cardano Problem Statement (CPS) has been formally written for this problem. CIP-0050 and CIP-0037 both propose modifications to the reward curve at this layer — but they were designed without a shared, formal problem definition to scope them against.

This analysis identifies the gap and names the missing problem statement — Closing the Consensus Incentive Gap — derived from the mainnet evidence in the dedicated Pools Pot Distribution Gaps sub-report.

The evaluation of proposed solutions (CIP-0050, CIP-0037, and the downstream CIPs that interact with them) is deferred to a future synthesis section, after the operator/delegator distribution analysis in Operator / Delegator Distribution and the population analysis in §2 complete the picture.

1.2.4. Divergence with intended equilibrium

The observations above document what the reward curve produces. This section examines why — by following an operator through the trajectory the mechanism promises (entry → progression → endgame) and identifying the point at which the reward curve stops rewarding the intended strategy.

The baseline for this analysis is The Intended Game, which describes the game as it should play out.

1.2.4.1. Entry — below 3M ₳, too committed to just delegate, too small to operate

An operator registers a pool, pledges what they can — say 50K ADA — and starts looking for delegators.

The promise (The Intended Game §1.3.2) is clear: pledge commitment is the competitive dimension, and increasing it should produce visible, measurable advantages that attract delegation. The game should feel like a ramp — each step forward in commitment unlocking the next level of reward and reputation.

The first step is high.

1.2.4.1.1. The structural floor

Block production on Cardano is a Poisson process: with ~21,600 slots per epoch and total active stake $S$, a pool of stake $\sigma$ expects $\lambda = 21{,}600 \times \sigma / S$ blocks per epoch. The number actually produced is $\text{Poisson}(\lambda)$, with variance equal to the mean — meaning that at small $\lambda$, yield is dominated by noise rather than by stake.

Two regimes follow from this:

- At $\lambda < 1$ (~< 1M ADA at today's active stake) the pool expects less than one block per epoch — most epochs produce zero blocks, and reward variance overwhelms the signal entirely. Yield is noise.

- At $\lambda = 3$ (~3M ADA at today's active stake) the pool produces ≥ 1 block per epoch with 95% probability (\$1 - e^{-3} = 0.95$). Yield becomes a usable signal — for the operator's economics, and for delegators choosing pools.

The production threshold is the second of these — the 95%-block-probability bar at λ=3, ~3M ADA today. This is the boundary used throughout the analysis (POL.O3.F1, CEN.O1.F1) and the one delegators can actually act on. It is a hard structural floor set by the physics of the consensus protocol, not by a tuneable parameter.

A separate, volatile concept — the viability threshold — is the stake level at which an operator can pay themselves enough to cover real fiat-denominated costs (infrastructure + DevOps labour). At today's ADA/USD price the viability threshold and the production threshold roughly coincide, so we treat the production threshold as the operative entry barrier and discuss viability as a separate ADA-price-dependent concept (POL.O3.F2).

The production threshold is the irreducible boundary — the floor every operator must clear.

1.2.4.1.2. A gate with no sign

Crucially, the mechanism does not communicate this floor. Nothing in the protocol tells a prospective operator "do not register a pool below ~3M ₳ — it will not produce blocks reliably." Registration is open at any amount.

The game lets participants in, takes their operational costs, and gives nothing in return.

The result is visible on mainnet: 2,144 of 2,877 pools (75%) sit below the production threshold and together hold only 2.7% of stake (CEN.O1.F1, POL.O4.F1). They are sub-block (λ < 1) or sub-reliable (1 ≤ λ < 3) — both noise-dominated, neither a usable yield signal.

These pools have no reason to exist — not from a consensus perspective (they contribute negligibly to block production), not from an investment perspective (they destroy value for their delegators), not from any perspective.

And the damage extends beyond the pools themselves. They pollute the landscape for every other participant.

- Delegators browsing a pool explorer must navigate hundreds of sub-reliable pools that look superficially legitimate but cannot deliver reliable yield.

- Wallet developers building staking features must decide how to present a pool set where the majority are economically inert.

- Viable operators must compete for visibility in a catalogue diluted by pools that the mechanism should never have admitted.

The signal-to-noise ratio of the entire pool marketplace degrades — making delegation decisions harder, accountability less effective, and the competitive environment less legible for everyone.

They are artifacts of a mechanism that defines a structural floor but does not signal it. The protocol silently accepts participants it cannot serve — and in doing so, degrades the experience for those it can.

1.2.4.1.3. Capital over competence

Below the structural floor, the rational move is to delegate — not operate. An operator can still accumulate the deflationary asset, but as a passive participant.

Delegation earns yield, but it does not earn the leverage that comes with consensus participation. The skin in the game is capital; it is not commitment to the network.

A prospective operator may have exceptional technical knowledge — capable of running a reliable, performant node — but the mechanism does not value knowledge. It values capital at scale.

An operator with deep expertise and 100K ₳ is invisible to the reward curve. A capital holder with no expertise and 5M ₳ can hire the expertise.

The game's entry filter selects for capital, not for the operational competence the protocol actually needs.

1.2.4.1.4. The sub-threshold problem — what Rocket Pool tells us

The preceding sections establish a structural contradiction: the protocol allows anyone to register a pool, but the physics of block production imposes a floor (~3M ₳ at today's active stake — the 95%-block-probability bar) below which operation is noise, not signal. Below ~1M ₳ a pool produces less than one block per epoch in expectation; between ~1M and ~3M it produces blocks but with too much Poisson variance to drive predictable yield. Either way, the pool destroys value for its delegators and serves no consensus function.

Between registration and the production threshold lies a corridor that the mechanism does not bridge — an open door that leads to an empty room.

This is not unique to Cardano. Ethereum's consensus layer requires exactly 32 ETH (~€55K at current prices) to activate a validator — an explicit production threshold enforced at the protocol level. The design acknowledges that consensus participation has a minimum scale, and makes that minimum legible rather than leaving participants to discover it through economic loss.

Cardano's production threshold is implicit — emergent from Poisson statistics, not declared as a parameter. The result is a marketplace where 2,144 sub-threshold pools (75% of pools with stake) carry only 2.7% of stake and serve no consensus function. They dilute the pool marketplace, mislead delegators, and impose a cost (in operator time, in delegator lost yield) that the protocol could avoid by making the threshold explicit.

The more interesting question is what lies on the other side of enforcement.

Ethereum's explicit threshold created demand for pooling services that allow sub-threshold participants to contribute capital toward consensus participation without operating a validator themselves. Rocket Pool — the largest decentralised liquid staking protocol on Ethereum (~4,000 independent node operators, ~800K ETH staked) — fills exactly this gap.

A participant bonds as little as 4 ETH alongside pooled capital from passive stakers, and the protocol assembles a full 32 ETH validator. The operator runs the infrastructure; the stakers provide the capital; a smart contract enforces the split. Permissionless entry, transparent commission, and a collateral bond (RPL tokens, 10–150% of operator ETH) as skin-in-the-game.

The parallel to Cardano is instructive but not direct. Rocket Pool exists because Ethereum requires 32 ETH — the structural need for pooling is baked into the protocol. Cardano has no minimum stake to register a pool, so the need is different: it is not access to consensus that is blocked, but economic viability.

A Cardano equivalent would not pool capital to meet a protocol-level gate; it would pool commitment to cross the emergent viability threshold — combining the operational competence of a technically capable participant with the capital of delegators who want to support the network at a level above passive delegation.

The design space this opens is explored in Enforce the production threshold — build a Rocket Pool for Cardano.

1.2.4.1.5. Analytical scope — pools above the production threshold

The preceding sub-sections establish that pools below the production threshold (~3M ₳ — the 95%-block-probability bar from POL.O3.F1) are structural artefacts: they cannot produce blocks reliably, they destroy value for their delegators, and they dilute the legibility of the pool marketplace for every other participant.

Including them in the downstream analysis — strategy classification (Progression — balanced as intended, but private by design), mainnet landscape (Endgame — the hollow strategy is the dominant one), intra-pool split (Operator / Delegator Distribution) — would contaminate every aggregate with noise from a population that the mechanism cannot serve and that has no bearing on the incentive dynamics the analysis evaluates.

At epoch 623, the production threshold partitions the rewarded pool set as follows:

| Below 3M ₳ (sub-block + sub-reliable) | Above 3M ₳ (productive) | Total | |

|---|---|---|---|

| Pools | 2,144 (74.5%) | 733 (25.5%) | 2,877 |

| Active stake | 0.58B ADA (2.7%) | 21.18B ADA (97.4%) | 21.75B ADA |

| Delegations | 127,754 (9.4%) | 1,227,281 (90.6%) | 1,355,035 |

The 2,144 sub-threshold pools carry 2.7% of active stake and 9.4% of delegations. They add noise to entity counts but contribute nothing to the structural picture; their inclusion would inflate the entity count and compress the strategy distributions without changing any finding.

All analysis from Progression — balanced as intended, but private by design onward restricts the pool set to rewarded pools above the production threshold (active stake ≥ 3M ₳). The companion sub-reports — The Pools Pot Distribution Gaps, The Operator's Cut — apply the same filter.

Where the sub-threshold population is relevant (Entry — below 3M ₳, too committed to just delegate, too small to operate), it is analysed in its own right.

1.2.4.2. Progression — balanced as intended, but private by design

An operator has crossed the production threshold. The pool produces blocks, earns rewards, and the deflationary accumulation thesis from The Intended Game §1.2.2.1 is finally in play.

The question becomes: how does the operator grow?

The mechanism's answer (The Intended Game §1.3.2.2) is pledge. Increasing personal commitment should produce a measurable competitive advantage — visible to delegators, economically meaningful to the operator — creating a legible progression from "new pool" to "established pool" to "fully committed pool".

Before examining what the pledge mechanism delivers in practice, it is worth mapping the strategic landscape it creates.

1.2.4.2.1. The three strategies

Every entity that crosses the production threshold enters a game defined by two structural facts:

- a shared endgame that all entities converge on;

- a single degree of freedom that separates their paths.

Together, these two facts define the full strategic landscape.

1.2.4.2.1.1. The common endgame — saturate, then become an MPO

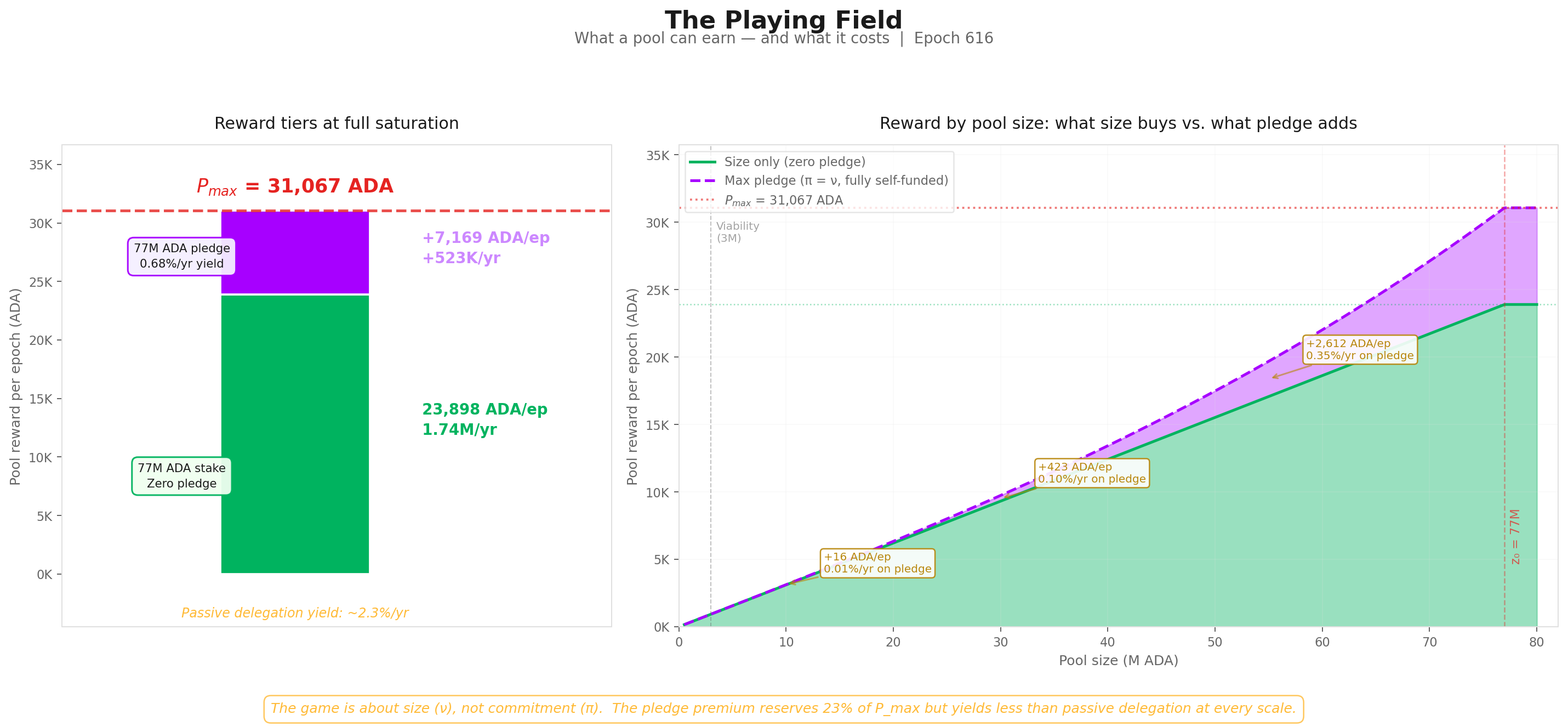

The reward formula caps individual pool rewards at $P_{\max}$: once a pool reaches the saturation point ($\sigma = z_0 \approx$ 77M ₳), every additional ADA of stake produces zero marginal reward. Worse — it dilutes the per-ADA yield for every existing participant, operator and delegator alike. The saturation cap is a hard ceiling, not a soft one.

An entity whose capital or delegation-attracting capacity exceeds $z_0$ therefore faces a binary choice: stop growing, or register a second pool. Since the entity's motivation for entering the game — the deflationary accumulation thesis (The Intended Game §1.2.2.1) — is driven by continuous compounding, stopping is irrational.

The mechanism's natural growth path is not deeper commitment to a single pool; it is fleet expansion: becoming a multi-pool operator (MPO). Saturate the current pool, register a new one, repeat.

This endgame is strategy-independent. Whether an entity fills pools with personal capital, with external delegation, or with a mix of both, the saturation cap forces the same MPO trajectory. The distinction between entities lies not in the destination but in how they staff each pool along the way.

And it is worth noting that the mechanism says nothing about this transition — there is no special reward for operating a single pool, no penalty for splitting across many. The formula evaluates each pool independently. The entity-level strategy that spans multiple pools is invisible to the protocol.

1.2.4.2.1.2. The degree of freedom

Within the shared endgame, an entity retains one strategic variable per pool: the ratio between owner commitment (pledge and self-delegation) and third-party delegation.

This ratio defines the entity's posture — the answer to the question "who funds this pool, and therefore who benefits from it?"

The spectrum is continuous. At one extreme, the operator funds the entire pool with personal capital — no delegator plays any role. At the other, the operator contributes nothing but infrastructure and a registration certificate — every ADA in the pool belongs to someone else. Between these poles lies every possible split.

The reward formula is sensitive to this ratio through the pledge bonus ($\lambda_{\text{pledge}} \cdot A(\nu, \pi)$), which depends on the within-pool pledge ratio $\pi = s/\sigma$. In principle, the bonus should pull operators toward higher commitment. Whether it does so in practice — with sufficient force to overcome the costs it imposes — is the question the rest of this section examines.

Three archetypes capture the essential strategic postures along this spectrum. They are not discrete options — real operators occupy every point on the continuum — but they define the poles and the centre in terms that map cleanly onto the security properties the protocol depends on.

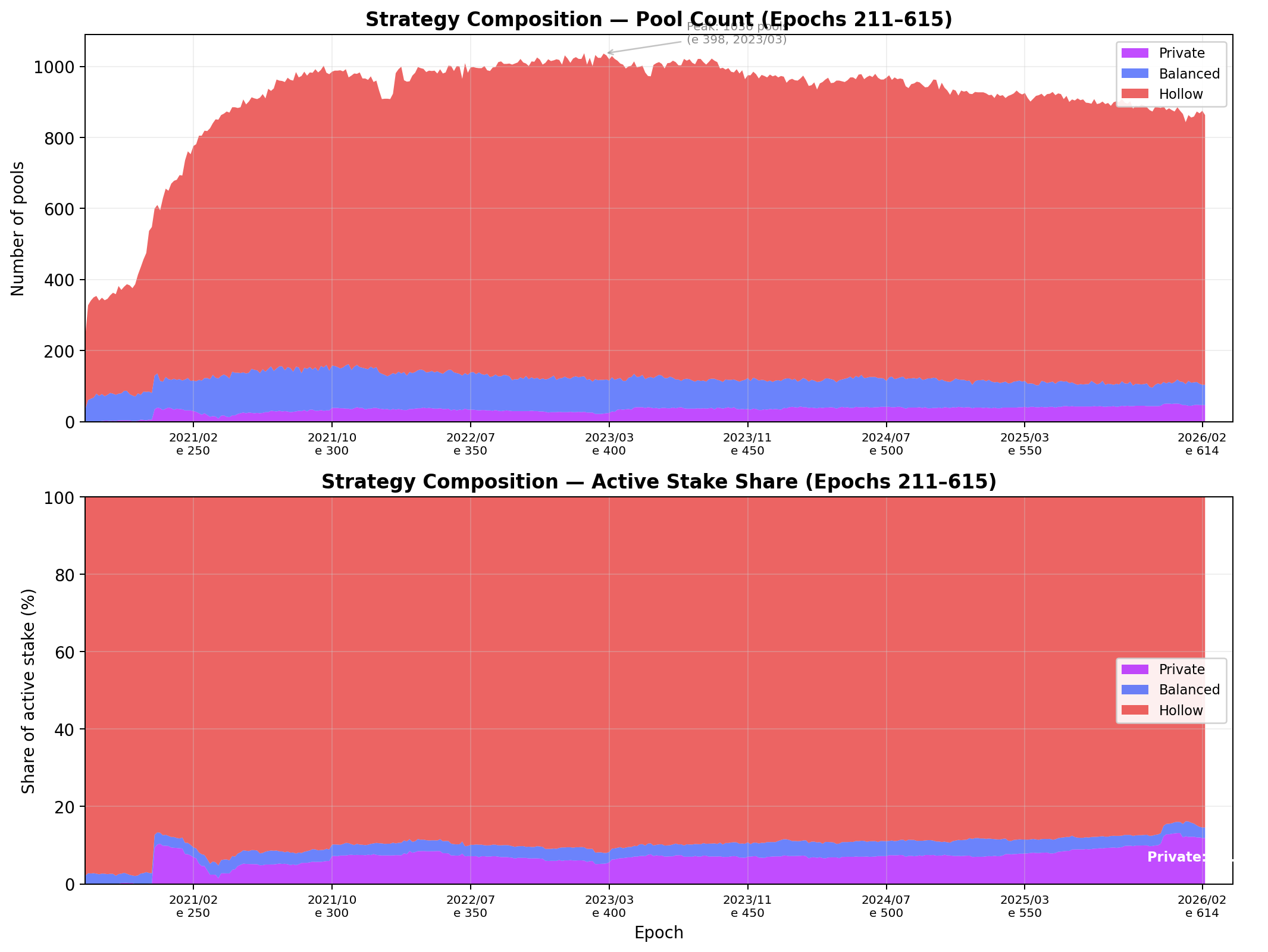

1.2.4.2.1.3. Strategy stability over time

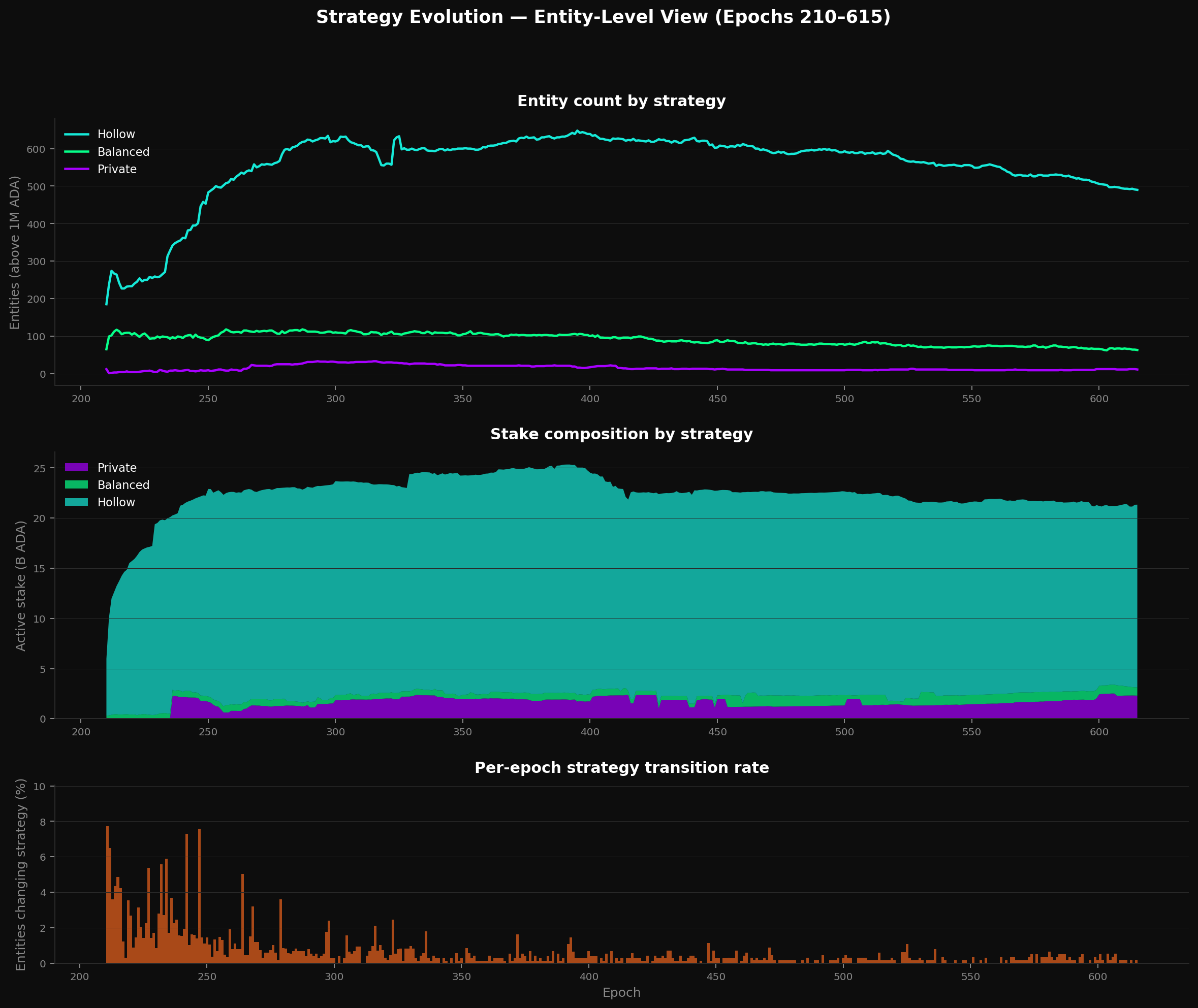

The three strategies described below are not transient labels. A natural question is whether entities migrate between postures over time — i.e. whether the archetypes are stable structural features or shift as delegation flows.

The figure tracks three panels across 405 epochs:

- Top panel — entity counts by owner-stake strategy (restricted to pools above the 3M ADA production threshold): hollow entities have grown steadily from ~200 to ~500, balanced has peaked around 300 and declined to ~200, and private has remained flat at ~50.

- Middle panel — the corresponding stake composition: hollow has dominated throughout, rising from ~8B to ~21B.

- Bottom panel — the per-epoch strategy transition rate: the fraction of entities whose dominant owner-stake strategy changed from one epoch to the next.

The transition rate is remarkably low. The median per-epoch rate is 0.28% — meaning that in a typical epoch, fewer than 2 entities out of ~600 change strategy. The margin-band transition rate is even lower at 0.16% per epoch.

Over the full 405-epoch span, 446 of 1,830 entities tracked (24.4%) changed strategy at least once. But the nature of these transitions reveals that nearly all of them are boundary drift rather than genuine strategic pivots: 89% of the 1,431 total transition events are hollow ↔ balanced oscillations (652 balanced→hollow, 621 hollow→balanced).

These occur when an entity's delegation fluctuates around the 10% owner-stake threshold — the entity's behaviour does not change, only the label assigned by the classification boundary. Transitions involving the private strategy are rare: 78 private→balanced, 52 balanced→private, 28 involving hollow↔private.

Among entities active for at least 200 epochs (n=612), 37.9% experienced at least one label change — but the overwhelming majority are threshold oscillations, not deliberate repositionings.

The margin landscape confirms this stability. The median margin across all pools has held at 2.0% since the early Shelley era. The rising stake-weighted mean (4.2% → 18.9%) is driven entirely by the growing weight of declared-private and functionally private pools in the overall stake distribution, not by fee inflation in the competitive market.

The per-epoch strategy transition rate is 0.28% (median) — fewer than 2 entities per epoch. Over 405 epochs, 89% of all transitions are boundary drift between hollow and balanced, not genuine regime changes. The three strategies are durable features of the network's economic structure, not artefacts of a single snapshot. Margin competition in the hollow market has been stable at a median of 2.0% for the entire Shelley era — the apparent rise in the stake-weighted mean is a compositional effect from the growing weight of private-strategy pools.

1.2.4.2.1.4. The balanced strategy

The balanced strategy maintains a meaningful owner-stake ratio while leaving substantial room for delegation. Both the operator and external delegators contribute to the pool's stake. The exact split — whether 20/80, 50/50, or 80/20 in favour of owner commitment — varies across entities, but the defining characteristic is that neither party fills the pool alone.

The economic logic is partnership: the operator commits personal capital and operational infrastructure; delegators provide the remaining stake that carries the pool toward saturation. The operator earns the fixed fee, the margin, and a share of the pool's size-based reward on their own stake, plus whatever the pledge bonus adds. Delegators earn the residual yield after the operator's cut.

Both parties have a reason to remain — and both have a credible exit option that the other must respect.

This is the posture the mechanism was designed to encourage. The operator's progression described in The Intended Game §1.3.2 — build reputation, attract delegation, deepen pledge, compound — presupposes a balanced configuration where increasing commitment produces a measurable competitive edge.

1.2.4.2.1.5. The private strategy

The operator pledges and self-delegates the majority or totality of the pool's stake, minimising or eliminating external delegation. The pool operates as a closed vehicle: the operator funds it, produces blocks, and collects the full reward.

The economic logic is self-sufficiency: the operator needs no one else. There is no margin to set (the operator captures everything), no delegator to attract (or lose), no reputation to build in the marketplace. The pool's competitiveness is a function of one variable — the operator's treasury size.

The reward formula explicitly endorses this posture. The maximum pool reward $P_{\max}$ is defined at $\pi = 1$ and $\nu = 1$: the operator pledges the entire saturation amount, the pool is full, and the operator is the sole beneficiary. This is not an incidental corner case — it is the designed optimum of the reward curve. The formula's "dream" is a pool where the operator funds everything and needs nobody.

Private pools are therefore not deviations from the mechanism's intent — they are its literal target. The tension this creates with the security properties the protocol depends on (which require delegation to be present and pledge to be an active competitive dimension, not a wealth filter) is the subject of Why balanced should be the intended equilibrium.

1.2.4.2.1.6. The hollow strategy

The operator pledges nothing or near-nothing and fills the pool entirely through external delegation. The pool operates at zero or near-zero owner commitment — block-production rewards are generated almost entirely from third-party stake.

The economic logic is leverage: the operator contributes infrastructure and a registration certificate, then captures the fixed fee plus margin on other people's capital. In the current parameter regime (340 ₳ fixed cost, typical margins of 1–5%), this means the operator extracts a guaranteed income stream without committing personal capital to the pool.

The opportunity cost is zero — the operator's own ADA can be delegated elsewhere, used as collateral, or held liquid. The only "pledge" is whatever token amount the operator registers to satisfy the certificate requirement.

This is the rational response when the pledge bonus is too small to justify the costs it imposes (liquidity lock-up, pledge-unmet risk — detailed in Endgame — the hollow strategy is the dominant one). If deepening commitment earns nothing detectable, the dominant move is to minimise commitment and maximise the capital base over which the operator extracts fees.

It is also the only available strategy for custodial operators (exchanges, staking-as-a-service providers) who cannot pledge the capital they manage for legal and fiduciary reasons — a population examined in The current design incentivises the private strategy.

These three archetypes span the full spectrum of the pledge/delegation ratio. They are not equally desirable. A network of balanced pools and a network of hollow pools may look similar on a pool explorer — both have delegation, both produce blocks — but their security properties are fundamentally different. The section that follows evaluates each against the invariants the consensus layer depends on.

1.2.4.2.2. Why balanced should be the intended equilibrium

The consensus layer does not care which strategy operators prefer. It cares whether the resulting equilibrium preserves a set of structural properties without which the security model breaks down.

The Intended Game §1.3.4 derives four such properties from the formal literature and the SL-D1 specification:

- Accountability — block producers must bear a real economic cost for misbehaviour.

- Delegation as counter-power — delegators must have the leverage to discipline operators through credible exit.

- Sybil resistance — creating additional block-producing identities must carry a cost that scales through the mechanism, not merely through wealth.

- Decentralisation — the entry barrier must admit diverse, single-pool operators rather than concentrating production among the capital-rich or the brand-dominant.

These properties are not independent — accountability requires delegation to have an enforcer, delegation requires accountability to have consequence, Sybil resistance and decentralisation must be jointly calibrated — and the structural requirement they impose is that each pool must combine meaningful operator commitment with meaningful external delegation (The structural requirement).

The three strategies defined above map directly onto this framework. The question is which, if any, produces an equilibrium that satisfies all four properties simultaneously.

What happens if the equilibrium is not balanced

The argument is sharpened by examining the alternatives as systemic outcomes — not as individual pool strategies, but as the equilibrium the entire network converges toward.

If the equilibrium is all-private: every pool is funded entirely by its operator. The operator landscape shrinks to the few dozen entities with enough capital to saturate a pool (~77M ₳ each). Delegators are excluded from consensus entirely — they can still delegate, but no pool needs their stake.

The accountability mechanism collapses: operators answer only to themselves. The network is secure against external Sybil attacks (the capital barrier is enormous) but has no defence against collusion among the small set of plutocratic operators. Consensus power is concentrated by construction. The protocol has produced a permissioned system with extra steps.

If the equilibrium is all-hollow: every pool operates at zero or near-zero pledge. Registering a new pool costs nothing beyond infrastructure — the Sybil defence is gone. A well-capitalised attacker can register hundreds of pools, attract delegation through marketing or exchange integration, and accumulate consensus power without committing personal capital.

The accountability mechanism is formally present (delegators can exit) but economically inverted: the operator has nothing at risk, so the "consequence" of delegator exit is that the operator loses a revenue stream they can rebuild by registering another pool. Delegation concentration follows brand and convenience, producing the concentrated market structure visible on mainnet today. The protocol has produced a system where the entities with the most consensus power are the ones with the least to lose.

If the equilibrium is balanced: operators commit meaningful personal capital (the bond exists), delegators provide the growth path and the continuous oversight (the enforcement mechanism exists), fragmentation is costly because it dilutes pledge across pools (the Sybil tax operates), and the entry barrier is calibrated to admit operators of moderate means (the operator set is diverse).

All four properties hold simultaneously. The balanced equilibrium is not a compromise between private and hollow — it is the only configuration in which the dependency chain described in The Intended Game §1.2.4 functions as designed.

Evaluation against the four properties

The following table evaluates each strategy against the security properties. Each cell contains the reasoning, not just the conclusion.

| Property | Balanced | Private | Hollow |

|---|---|---|---|

| Accountability | Operator commits meaningful capital — a legible bond that is costly to abandon. The bond exists independently of delegator attention, providing a baseline cost of misbehaviour even when oversight is imperfect. | Maximal capital exposure, but self-referential. The operator is accountable only to themselves. In a system without slashing, self-accountability has no enforcement mechanism — the operator both commits the offence and decides the penalty. No external interest is at risk. | Eliminated. Zero pledge means zero cost of exit. The operator can abandon a misbehaving pool and register a new one without forfeiting anything. The accountability structure exists on paper but has no economic content. |

| Delegation as counter-power | Delegators are present and their departure is costly to the operator — the pool shrinks, rewards drop, competitive position degrades. The feedback loop is intact: delegator exit is a credible threat because the operator depends on delegation for a material share of pool stake. | No delegators, no exit threat. The pool is a closed system. The operator can degrade performance, raise margin to 100%, or go offline — the only consequence is self-inflicted. The disciplinary mechanism has no input. | Formally present but inverted. Delegators provide all capital, but the operator has nothing at stake. If delegators exit, the operator loses a revenue stream — but can rebuild it by registering a new pool at near-zero cost. The exit cost falls on the delegator (search cost, epoch delay) more than on the operator. The power asymmetry runs the wrong way. |

| Sybil resistance | Real cost of fragmentation: splitting into $n$ pools requires dividing pledge across $n$ certificates, diluting the bonus per pool and reducing competitiveness in each. The Sybil tax operates through the mechanism — it is the pledge bonus that makes fragmentation suboptimal. | High capital cost per pool, but the constraint is wealth, not the pledge mechanism. An entity with enough capital can operate as many saturated pools as their treasury permits. The pledge bonus is negligible relative to the capital deployed; what prevents fragmentation is running out of money, not forfeiting a bonus. The mechanism's Sybil defence is irrelevant — raw wealth does the work. | Near zero. Registering a new pool requires only infrastructure and a certificate fee. The 83 attributed entities on mainnet — some operating dozens of pools with minimal or zero pledge — demonstrate that fragmentation is cheap when no pledge is required. The mechanism's Sybil defence is absent. |

| Decentralisation | Capital is shared between operator and delegators — the entry barrier admits operators of moderate means. Operators compete on commitment and community trust, not on treasury size alone. The competitive field is wide enough for diverse, single-pool operators to coexist. | Concentrated among the capital-rich. The effective entry barrier is the saturation cap (~77M ₳ per pool). The operator set is bounded by the number of entities with eight-figure treasuries — a vanishingly small population. Block production is permissioned by wealth. | Entry barrier near zero, but delegation flows to the most visible, not the most committed. Exchange pools, custodial services, and brand-driven fleets attract delegation through convenience. Concentration emerges through market dynamics: 83 attributed entities control 76.7% of productive stake. The long tail of single-pool operators is structurally starved. |

The balanced strategy is the only one that satisfies all four properties simultaneously — not as a theoretical possibility, but as a stable configuration in which each property reinforces the others.

- Private preserves accountability in a narrow, self-referential sense but eliminates the delegation feedback loop, renders the Sybil mechanism redundant, and concentrates production among the capital-rich.

- Hollow preserves the appearance of delegation but strips it of disciplinary power, removes every cost that the consensus layer depends on, and produces concentration through market dynamics rather than capital barriers.

The question that follows — and that the rest of this section examines — is whether the current mechanism actually produces this balanced equilibrium, or whether its parameter regime drives rational actors toward one of the alternatives.

1.2.4.2.3. The current design incentivises the private strategy

The maximum pool reward $P_{\max}$ is defined at $\pi = 1$ and $\nu = 1$: the operator pledges the entire saturation amount ($z_0 \approx$ 77M ₳) and the pool is fully saturated. Since pledge counts as stake, this means the operator funds the entire pool with personal capital. There are no delegators.

The reward curve's global maximum is a closed vehicle where the operator is the sole funder, the sole block producer, and the sole beneficiary.

This is not an incidental corner case or a mathematical artefact. It is the explicit target of the reward function — the point toward which the formula's gradient pulls any rational operator. The entire reward surface is oriented so that increasing $\pi$ and increasing $\nu$ both increase the reward, and the global maximum sits at the intersection of both maxima: full pledge, full saturation, zero delegation.

The endgame the mechanism defines — reached by every operator who follows the formula's gradient to its conclusion — requires ~77M ₳ (~30M USD) of personal capital, locked. The total yield on a fully-pledged saturated pool is ~2.95%/yr, of which only +0.68%/yr comes from the pledge bonus above the ~2.27%/yr base.

The mechanism's ideal operator is not the committed community member who grew from a modest start; it is a solitary whale who locks a fortune for a marginal uplift to run a pool that no one else participates in.

This creates a direct contradiction with the security requirement established in Why balanced should be the intended equilibrium. The equilibrium the formula optimises for — $k$ private pools, each fully funded by a single wealthy operator, with no delegator participation — is precisely the all-private scenario that eliminates delegation as counter-power, restricts participation to the capital-rich, and concentrates consensus among a small plutocratic set.

The formula's designed optimum breaks two of the four security properties it was supposed to preserve.

The formula says: the best pool is a private pool. The security model says: the best pool is a balanced pool.

The mechanism's two requirements pull in different directions.

1.2.4.3. Endgame — the hollow strategy is the dominant one

The formula points toward private (The current design incentivises the private strategy). Mainnet converges on hollow. This section explains the gap — not as a single failure, but as a series of compounding factors that make hollow the rational outcome at every decision point an operator faces.

The argument builds in layers:

- First, what the network actually looks like.

- Then, why the game's structure favours delegation over pledge before any reward calculation enters the picture.

- Then, why the reward formula reinforces rather than counteracts this default.

- Finally, why the resulting dynamic is self-reinforcing.

1.2.4.3.1. What mainnet reveals

The three archetypes defined in The three strategies — hollow, balanced, private — are conceptual. To confront them with five years of mainnet data, a single observable criterion is needed: the owner-stake ratio (owner active stake / pool active stake).

Computed at the entity level — averaged across all pools in an entity's fleet — the ratio captures who funds the pool. It is orthogonal to fee policy: a hollow entity can charge high margins; a balanced entity can charge nothing. What the ratio measures is the funding structure, not the pricing decision.

The spectrum divides into three populations:

- Hollow (owner-stake ratio < 10%): entities that depend entirely on external delegation.

- Balanced (10–95%): entities with genuine capital at stake alongside delegators.

- Private (≥ 95%): operator-funded entities where external delegation is negligible.

The entity-level strategy profiles, population breakdowns, and consistency data that follow are drawn from The Operator's Cut, a companion analysis of the intra-pool reward split (Operator / Delegator Distribution) that applies this classification across all 502 entities operating rewarded pools above the production threshold at epoch 614 (Analytical scope — pools above the production threshold).

1.2.4.3.1.1. Three operator strategies, one dominant

The distribution is not ambiguous.

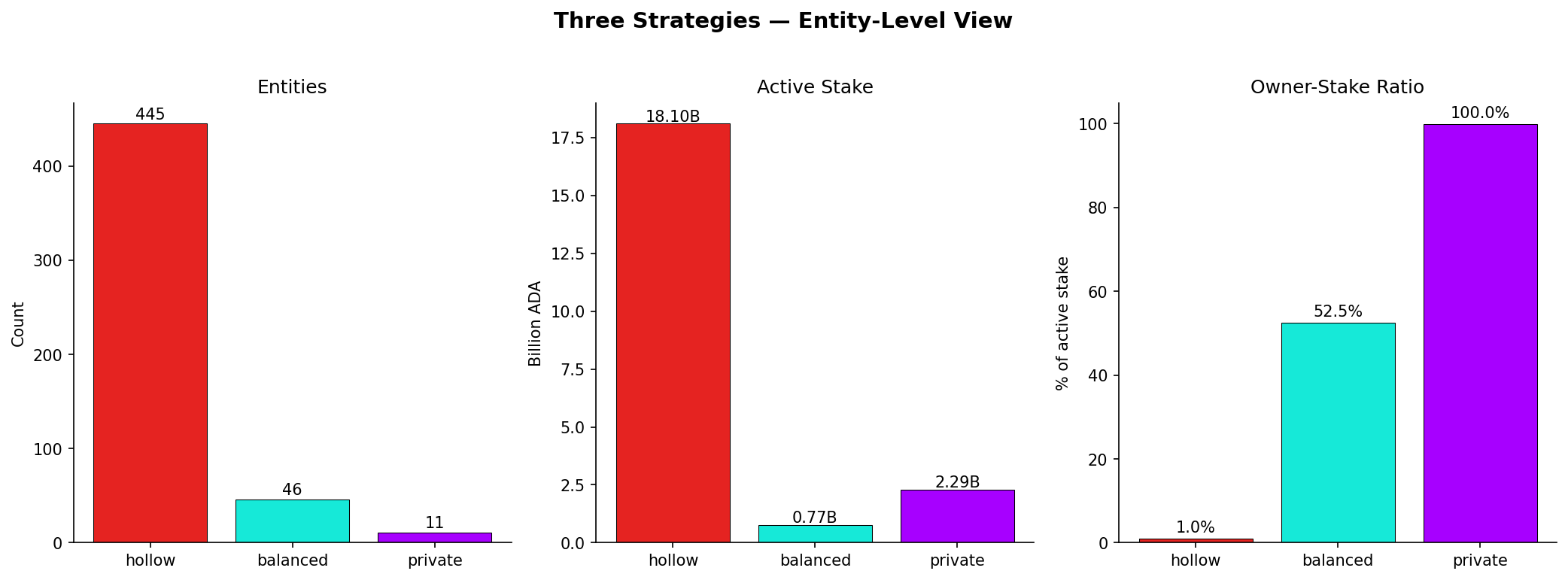

| Hollow | Balanced | Private | All | |

|---|---|---|---|---|

| Entities | 445 (88.6%) | 46 (9.2%) | 11 (2.2%) | 502 |

| Pools | 771 | 60 | 44 | 875 |

| Active stake | 18.10B ADA (85.6%) | 0.77B ADA (3.6%) | 2.29B ADA (10.8%) | 21.16B ADA |

| Owner stake | 0.18B ADA (1.0%) | 0.40B ADA (52.5%) | 2.29B ADA (100.0%) | 2.87B ADA (13.6%) |

- Hollow entities control 18.10B ₳ (85.6% of active stake) with a collective owner-ratio of 1.0% — for every 100 ADA staked in hollow pools, about 1 ADA comes from the operator.

- Private entities control 2.29B ₳ (10.8%), almost entirely self-funded.

- Balanced entities hold 0.77B ₳ (3.6%) — the smallest segment but the only one where the pledge mechanism produces genuine alignment.

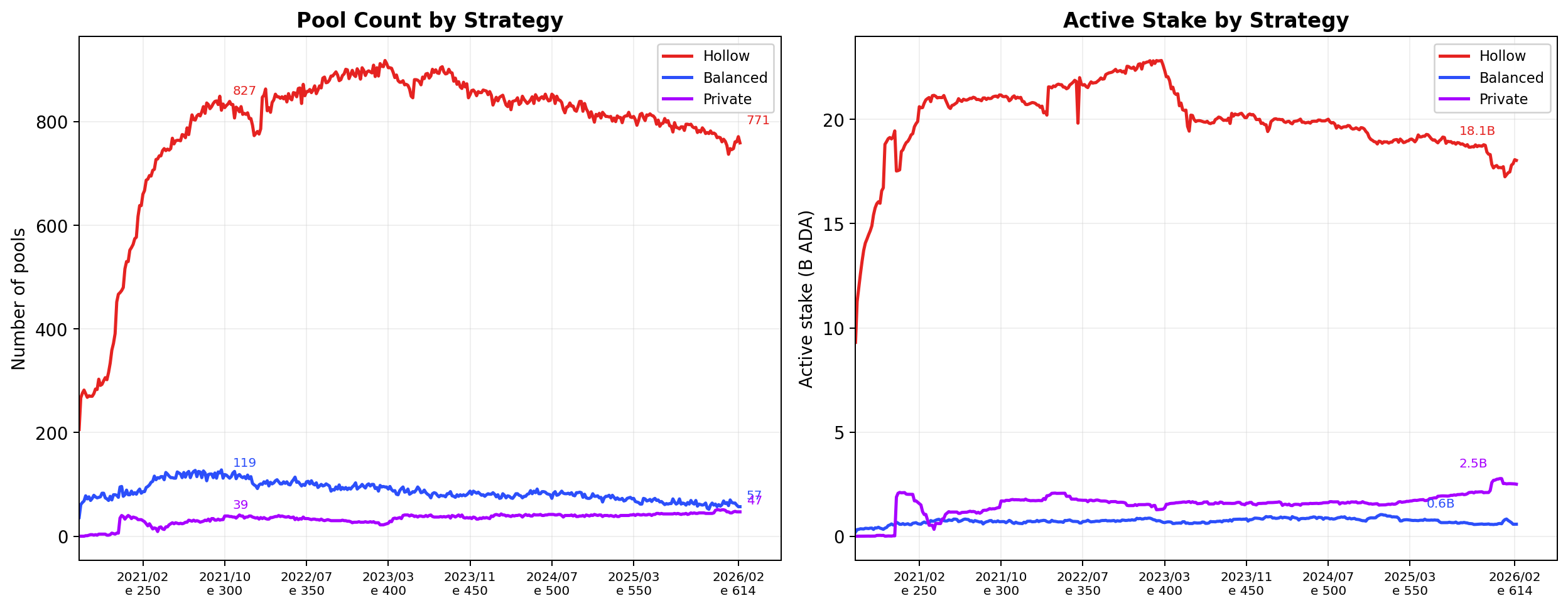

This snapshot captures the end-state of a trajectory that has been remarkably stable since the early Shelley era. The figures below track both pool counts and active stake per strategy across 405 epochs (2020–2026).

The hollow strategy established dominance within the first 50 epochs of Shelley and has held 85–92% of active stake ever since. Pool count peaked at 904 around epoch 400 (2023/03) and has since declined to 771 — a 15% contraction — as the shrinking epoch pot makes marginal pools unprofitable.

Balanced pools have thinned more sharply: from a peak of 119 (epoch 300) to 57 today, a 52% drop. Their stake share has fluctuated between 2.1% and 3.9% without a clear trend — the balanced strategy has neither grown nor consolidated.

The most visible shift is in the private segment. Private pool count has risen from zero at genesis to 47, and their stake share has nearly doubled from ~7% to 11.9% over the last 200 epochs. This growth is driven by exchange and custodial operators internalising staking rather than delegating to third-party pools — a structural trend that the reward formula neither encourages nor penalises.

1.2.4.3.1.2. Strategies are entity-level commitments, not pool-level accidents

A critical empirical finding validates the entity-level framing: strategy choice is highly consistent across pool fleets.

| Count | Percentage | |

|---|---|---|

| Pure-strategy entities | ||

| Hollow only | 438 | 87.3% |

| Balanced only | 44 | 8.8% |

| Private only | 13 | 2.6% |

| Subtotal pure | 495 | 98.6% |

| Hybrid entities | ||

| Mixed (spanning 2+ bins) | 7 | 1.4% |

| Total | 502 | 100% |

495 of 502 entities (98.6%) operate pools that all fall into a single strategy bin. Only 7 are hybrid — spanning two strategy bins — and they cluster at or near the threshold boundaries (owner-stake ratios around 10% or 95%), suggesting measurement noise or near-threshold entities rather than deliberate multi-strategy positioning.

Examining the 7 hybrid entities reveals that most sit near decision boundaries (owner-ratios 8–12% or 93–97%), several have very small secondary-strategy pools suggesting pilot or transitional operations, and none blur the distinction meaningfully.

This matters for the analysis in two ways.

First, entity-level strategy grouping is not a modelling convenience — it reflects a real structural choice. An entity does not run one hollow pool and one private pool; it commits to a strategy and applies it coherently across its entire fleet. The three strategies are game-theoretic choices, not artifacts of pool-level composition.

Second, counting by pool systematically overcounts the number of independent strategic decisions on the network. The 445 hollow entities operate 771 pools, but most fee-policy and capital-allocation decisions are made per entity, not per pool. Analysing the staking landscape per pool rather than per entity inflates the apparent diversity of the system while masking the concentration of strategic decision-making.

1.2.4.3.1.3. The hollow strategy dominates at every level of aggregation

The dominance is not a pool-count artifact — it holds across every meaningful aggregation dimension. Hollow entities comprise 88.6% of the entity population, control 85.6% of active stake, and operate 88.1% of above-threshold pools.

For every 100 ADA staked in hollow pools, about 1 ADA comes from the operator — a collective owner-stake ratio of 1.0%. These 445 entities command 18.10B ₳ in third-party delegation while committing only 0.18B ₳ of their own capital: a leverage ratio of roughly 100:1.

The pool-level pledge data reinforces the picture. Of 2,718 pools with active stake, 2,262 (83.2%) pledge less than 100K ₳. The median pledge-to-stake ratio across healthy pools is 0.14% — the median pool pledges roughly one ADA for every 700 it manages. 226 pools declare zero pledge outright. The hollow strategy is not adopted by a fringe — it is the norm, and the pledge mechanism has not altered this.

Among multi-pool operators — entities that have scaled beyond a single pool and thus revealed a deliberate growth strategy — the skew is sharper still. Of 75 MPOs: 67 (89.3%) are hollow, 3 (4.0%) operate as balanced, and 5 (6.7%) as private.

The entities that have chosen how to grow have overwhelmingly chosen to grow through delegation, not pledge. Fleet expansion dilutes any per-pool pledge commitment: an entity operating ten hollow pools spreads its pledge budget across ten certificates, each one negligible relative to the pool's total stake. The mechanism imposes no cost on this fragmentation — the formula evaluates each pool independently, so the entity-level strategic choice is invisible to the protocol.

1.2.4.3.1.4. The pledge bonus is a dead letter

The pledge bonus mechanism — the formula's entire budget for making the degree of freedom identified in The degree of freedom consequential — captures 1.0% of its theoretical allocation.

At the median pledge level, the bonus adds approximately 0.006% to pool rewards — a quantity undetectable against normal reward variance.

The budget that goes unclaimed is not negligible: 3.43M ADA per epoch (~250M ADA per year), representing 22.1% of the entire pools pot, returns to the reserve unused (Why pledge matters — and why this is not zero-sum).

This is the single largest addressable inefficiency in the reward pipeline — unlike the participation gap (unstaked ADA, outside the formula's control), the pledge-bonus waste is entirely within reach of parameter or formula reform.

The bonus fails not because operators are unaware of it, but because the cost of capturing it exceeds its value at every realistic operating point. Pledging imposes a liquidity lock, a binary penalty risk (pledge-unmet → zero rewards for the entire pool), and an opportunity cost relative to passive delegation — and the reward it offers in return is too flat, too small, and too dominated by the base stake term to shift behaviour (Delegating is inherently less constraining than pledging–The pledge bonus is inoperative at realistic scale).

The mainnet outcome — 445 hollow entities controlling 85.6% of stake with a collective owner-ratio of 1.0% — is the rational response to a bonus that the formula has priced below the threshold of economic relevance.

1.2.4.3.2. Delegating is inherently less constraining than pledging

Before examining the reward formula, a prior question must be settled: if two operators hold the same amount of ADA and face the same pool, and the only difference is whether they pledge that ADA or delegate it, which action is less costly?

The answer is unambiguous, and it holds regardless of any bonus the formula may attach to pledge.

Liquidity. Pledged ADA must remain in the operator's wallet for the duration of the pool's operation. It is registered on-chain as a commitment to the pool certificate and cannot be redeployed, used as collateral, lent, or moved to another pool without modifying the certificate.

Delegated ADA, by contrast, remains fully liquid. The holder can redirect it to another pool at any epoch boundary, use it in DeFi protocols, or sell it — the delegation is a preference signal, not a capital lock.

For an operator managing a treasury, pledging transforms a liquid asset into a frozen one. Delegating does not.

Reversibility. Delegation is revocable within a single epoch boundary — the delegator signs a new delegation certificate and the redirect takes effect at the next snapshot. De-pledging is formally possible but operationally fraught: the operator must update the pool certificate to lower the declared pledge, and the change takes effect at the next epoch boundary.

During the transition, any fluctuation in the pledged UTxO set that brings the balance below the still-active declared amount triggers the pledge-unmet penalty. The act of reducing commitment is itself a risk event. Delegation carries no equivalent penalty for changing one's mind.

Risk profile. The protocol imposes a binary, catastrophic penalty on pledge shortfalls: if the on-chain pledge balance drops below the declared amount at any snapshot during an epoch — due to a transaction, a wallet synchronisation issue, or any fluctuation — the pool's entire reward for that epoch is zeroed.

Not the pledge bonus — the entire reward, size component included, for the operator and every delegator in the pool. The penalty is not proportional to the shortfall. One ADA below threshold triggers the same total loss as a complete withdrawal.

Delegation carries no protocol-level penalty of any kind. A delegator who withdraws or redirects ADA does not trigger any penalty — neither for themselves nor for the pool.

The asymmetry is structural: the more an operator pledges, the larger the balance that must remain untouched, and the more catastrophic the penalty if anything goes wrong. The upside is a small, linear bonus; the downside is a total, binary wipe.

Pledging is the only action in the Cardano staking protocol where the risk profile is inversely proportional to the reward. Delegating has no risk profile at all.

Opportunity cost. ADA delegated to a pool earns the same base yield as the pool delivers to all participants — and the holder retains all other options. ADA pledged to a pool earns the same base yield plus a marginal pledge bonus — but the holder forfeits every other use.

In a protocol ecosystem with growing DeFi activity, lending markets, and liquidity provision opportunities, the opportunity cost of locking capital as pledge is real and increasing. The bonus would need to exceed not just zero, but the best alternative return available to that capital — a threshold that rises as the ecosystem matures.

Custodial exclusion. A significant class of operators — exchanges, custodial wallets, institutional funds, staking-as-a-service providers — manages capital that is not their own. For these entities, pledging is not a question of incentive but of legal possibility.

Pledged capital must remain in the operator's wallet; capital held on behalf of clients must be returnable on demand. The constraint is categorical: custodial operators cannot pledge the capital they manage, regardless of how attractive the mechanism makes it.

They are not choosing to ignore pledge — they are architecturally excluded from it. The reward formula asks them to play a game whose rules they cannot legally follow.

On mainnet, these entities — exchanges like Coinbase, Binance, Upbit, eToro; institutional validators like Figment, Kiln, Blockdaemon, Everstake — collectively manage billions of ADA in pools with near-zero pledge. Their strategy is hollow not by choice but by constraint.

The rational default. Each of these asymmetries — liquidity, reversibility, risk, opportunity cost, legal constraint — pushes independently toward delegation over pledge.

Taken together, they define a prior: before any reward is calculated, before any bonus is evaluated, the rational default for any ADA holder deciding how to participate in a pool is to delegate rather than pledge.

Pledging is the strictly more constrained action. It carries costs that delegation does not, risks that delegation does not, and restrictions that delegation does not. The only reason to pledge rather than delegate is if the reward formula compensates for all of these asymmetries — if the pledge bonus is large enough to overcome the liquidity cost, the reversal risk, the cliff penalty exposure, and the opportunity cost of locking capital.

The question that follows is whether the formula actually provides this compensation. The answer, as the following sub-sections show, is that it does not — and not by a narrow margin.

1.2.4.3.3. The reward structure weights size, not commitment

The degree of freedom — the pledge/delegation ratio — is governed by a single component of the reward formula: the pledge bonus ($\lambda_{\text{pledge}} \cdot A(\nu, \pi)$). Everything else in the pool's reward is sensitive to size ($\nu$), not to commitment ($\pi$).

The structural weight tells the story:

- The size-only component ($\lambda_{\text{size}} \cdot \nu$, where $\lambda_{\text{size}} \approx 76.9\%$ of $P_{\max}$) represents ~77% of the maximum reward.

- The pledge component ($\lambda_{\text{pledge}} \cdot A(\nu, \pi)$, where $\lambda_{\text{pledge}} \approx 23.1\%$) represents the remaining ~23%.

A pool that grows from 5M to 30M ₳ in total stake sees its per-epoch reward climb from ~2,000 to ~12,000 ADA — entirely from the size fraction, entirely insensitive to pledge.

The right panel of Figure 1 makes this visible. The green area — reward earned from stake size alone, with zero pledge — dominates at every scale. An operator who pledges nothing and one who pledges everything earn the same green area. The only strategic variable that moves this component is delegation attraction — and delegation responds to yield, brand, and convenience, not to pledge.

The signal the mechanism sends is unambiguous: ~77% of the maximum reward is reserved for growing the pool; ~23% for deepening commitment within it.

Given the inherent asymmetry established in Delegating is inherently less constraining than pledging — that pledging is the strictly more constrained action — the formula needed to weight commitment more heavily than size to overcome the natural gravitational pull toward delegation.

Instead, it weights size more than three to one. The formula does not counteract the prior; it reinforces it.

1.2.4.3.4. The pledge bonus is inoperative at realistic scale

The 23% allocated to the pledge component is the mechanism's entire budget for making commitment matter. Whether the degree of freedom is real or illusory depends on whether this budget produces detectable economic differences between strategies at the scales operators actually operate.

The following tables trace the pledge bonus across three pool sizes above the production threshold — from a small productive pool through full saturation — for five allocation strategies within a pool of fixed total size. Pools below the production threshold (3M ₳) are excluded from the analysis: they are noise-dominated and do not represent the population the mechanism is supposed to incentivise.

At 20M ₳ (ν ≈ 0.26):

| Strategy | Pledge | Self-delegation | Pool reward | Pledge bonus | Total yield | Bonus yield on pledge | Yield uplift |

|---|---|---|---|---|---|---|---|

| Hollow (0/100) | 0 | 20M | 6,208 ADA/ep | — | 2.27%/yr | — | baseline |

| Healthy delegation (20/80) | 4M | 16M | 6,291 ADA/ep | +82 ADA/ep | 2.30%/yr | 0.15%/yr | +1.3% |

| Balanced (50/50) | 10M | 10M | 6,361 ADA/ep | +152 ADA/ep | 2.32%/yr | 0.11%/yr | +2.5% |

| Healthy pledge (80/20) | 16M | 4M | 6,366 ADA/ep | +158 ADA/ep | 2.32%/yr | 0.07%/yr | +2.5% |

| Private (100/0) | 20M | 0 | 6,334 ADA/ep | +126 ADA/ep | 2.31%/yr | 0.05%/yr | +2.0% |

The bonus becomes visible but reveals a structural inversion: Private earns less bonus than Healthy pledge and Balanced. The operator who pledges everything — the strategy the formula's global maximum endorses — earns +126 ADA/ep, while the one who pledges 80% earns +158 ADA/ep. Beyond the concavity peak ($\pi^* \approx 0.68$ at this saturation level), each additional ADA pledged reduces the total bonus.

The formula punishes the very commitment its optimum was designed to incentivise.

At 40M ₳ (ν ≈ 0.52):

| Strategy | Pledge | Self-delegation | Pool reward | Pledge bonus | Total yield | Bonus yield on pledge | Yield uplift |

|---|---|---|---|---|---|---|---|

| Hollow (0/100) | 0 | 40M | 12,416 ADA/ep | — | 2.27%/yr | — | baseline |

| Healthy delegation (20/80) | 8M | 32M | 12,766 ADA/ep | +350 ADA/ep | 2.33%/yr | 0.32%/yr | +2.8% |

| Balanced (50/50) | 20M | 20M | 13,151 ADA/ep | +735 ADA/ep | 2.40%/yr | 0.27%/yr | +5.9% |

| Healthy pledge (80/20) | 32M | 8M | 13,369 ADA/ep | +953 ADA/ep | 2.44%/yr | 0.22%/yr | +7.7% |

| Private (100/0) | 40M | 0 | 13,422 ADA/ep | +1,006 ADA/ep | 2.45%/yr | 0.18%/yr | +8.1% |

The concavity peak has moved past $\pi = 1$ at this saturation ($\pi^* \approx 1.04$), so Private no longer loses to Healthy pledge in absolute bonus. But the bonus yield per pledged ADA continues to decline: from 0.32%/yr (Healthy delegation) to 0.18%/yr (Private). The total yield spread from Hollow to Private is 0.18%/yr — for locking 40M ₳ as pledge.

At saturation (77M ₳, ν = 1) — the theoretical ceiling:

| Strategy | Pledge | Self-delegation | Pool reward | Pledge bonus | Total yield | Bonus yield on pledge | Yield uplift |

|---|---|---|---|---|---|---|---|

| Hollow (0/100) | 0 | 77M | 23,898 ADA/ep | — | 2.27%/yr | — | baseline |

| Healthy delegation (20/80) | 15.4M | 61.6M | 25,332 ADA/ep | +1,434 ADA/ep | 2.40%/yr | 0.68%/yr | +6.0% |

| Balanced (50/50) | 38.5M | 38.5M | 27,483 ADA/ep | +3,585 ADA/ep | 2.61%/yr | 0.68%/yr | +15.0% |

| Healthy pledge (80/20) | 61.6M | 15.4M | 29,634 ADA/ep | +5,736 ADA/ep | 2.81%/yr | 0.68%/yr | +24.0% |

| Private (100/0) | 77M | 0 | 31,068 ADA/ep | +7,170 ADA/ep | 2.95%/yr | 0.68%/yr | +30.0% |

Only at full saturation does $A(1, \pi) = \pi$ become linear, eliminating the concavity penalty. The bonus yield stabilises at 0.68%/yr per pledged ADA regardless of allocation. This is the best case the mechanism offers — and it requires 77M ₳ (~30M USD) of personal capital. The total yield from Hollow to Private moves from 2.27% to 2.95%: a +0.68%/yr uplift for locking the entire saturation cap.

Reading the four tables together, the pattern is clear:

- Below the production threshold, the bonus does not exist.

- As the pool grows past the threshold, it emerges but remains small, concave, and — below saturation — inverted at the extreme the formula was designed to optimise.

- Only at the unreachable limit of full saturation does the bonus behave as intended, and even there the uplift is modest.

1.2.4.3.5. The size-visibility-delegation loop

The preceding sub-sections explain why an operator would not pledge. The mechanism the formula does not model explains why an operator would invest in delegation instead.

Delegators choosing a pool observe yield, reliability, and brand — all of which are functions of pool size, not pledge. A large hollow pool and a large pledged pool deliver nearly identical yields to their delegators (the pledge bonus is ~23% of the reward weight, split across all participants). From the delegator's perspective, pool size is the signal; pledge is noise.

This creates a self-reinforcing loop: large pools attract more delegation, which makes them larger, which makes them more visible and more reliable, which attracts more delegation. Pledge is orthogonal to this dynamic.

An operator who invests effort in delegation attraction — through brand, exchange partnerships, or multi-pool infrastructure — enters this virtuous cycle. An operator who invests capital in pledge does not.

The result is not that pledging is a bad investment in the traditional sense — the bonus is positive. It is that pledging is a dominated strategy: the same capital and effort, deployed toward delegation attraction, generate returns that compound through the size-visibility-delegation loop, while the pledge bonus remains flat, small, and constrained by costs the formula ignores.

1.2.4.3.6. The inversion

The mechanism was designed to reward commitment: pledge more, earn more, compound the advantage. The intended arc runs from Hollow toward Balanced — with the formula's gradient pointing beyond, toward Private (The current design incentivises the private strategy).

The actual incentive arc runs in the opposite direction.

- Foundation. Delegating is inherently less constraining than pledging — the rational default before any reward enters the picture (Delegating is inherently less constraining than pledging).

- Formula weight. The formula reinforces this default by weighting size over commitment by more than three to one (The reward structure weights size, not commitment).

- Inoperative bonus. The 23% it allocates to pledge is inoperative at every realistic scale (The pledge bonus is inoperative at realistic scale).

- Compounding. The size-visibility-delegation loop turns the initial advantage of delegation into a compounding one (The size-visibility-delegation loop).

A competing operator who pledges nothing and deploys that capital toward marketing, multi-pool infrastructure, or exchange partnerships will enter the snowball dynamic: more delegation → more size → more visibility → more delegation. An operator who pledges the same capital earns a small, flat bonus that does not compound and does not attract anyone.

The mechanism has inverted its own logic. The formula points toward private (The current design incentivises the private strategy); the game converges on hollow.

The strategy the formula was supposed to make suboptimal — capital deployed outside the pledge mechanism toward delegation growth — is the one that dominates.

The mainnet data in What mainnet reveals is not a failure of adoption. It is the rational response to a mechanism whose reward gradient and security requirement point in different directions.

1.2.4.4. Conclusion

The purpose of the reward formula is not to reward operators. It is to preserve the security properties the consensus layer depends on — accountability, delegation as counter-power, Sybil resistance, and decentralisation (Why balanced should be the intended equilibrium).

The formula is a tool in service of consensus integrity; the incentive structure it creates for operators is the means, not the end.

The order of priorities matters: the mechanism must first ensure that consensus retains its structural properties, and it does so by aligning the rational self-interest of operators with the equilibrium those properties require.

The analysis in Divergence with intended equilibrium surfaces three areas where the current design can evolve. Each corresponds to a different stage of the operator lifecycle, and each requires a distinct — though interconnected — response.

1.2.4.4.1. Enforce the production threshold — build a Rocket Pool for Cardano

The analysis in Entry — below 3M ₳, too committed to just delegate, too small to operate reveals a structural contradiction: the protocol allows anyone to register a pool, but the physics of block production imposes a floor (the 95%-block-probability bar at ~3M ADA) below which operation is unviable.

At epoch 614, 2,144 sub-threshold pools (< 3M ₳) carry 2.7% of active stake — they serve no consensus function, dilute the pool marketplace, and mislead delegators into pools that cannot produce reliable yield.

Step one: make the threshold explicit. Ethereum's Beacon Chain requires exactly 32 ETH to activate a validator — an explicit production threshold enforced at the protocol level. The design acknowledges that consensus participation has a minimum scale and makes that minimum legible.

Cardano's threshold is implicit, emergent from Poisson statistics. Making it explicit — preventing pool registration below a declared minimum active stake — would eliminate the sub-threshold noise that the current design tolerates.

The threshold need not be rigid: it could be a governance parameter ($\sigma_{\min}$), initially calibrated to the structural production boundary (~3M ₳, the 95%-block-probability bar — The structural floor), and adjustable as protocol economics evolve. The effect is not to close the game — it is to stop the game from misleading participants about its rules.

The protocol's minPoolCost floor is a separate, fee-policy concern at the intra-pool split layer (A gate with no sign). Whether fee-structure reform can keep the operator's entry experience legible once $\sigma_{\min}$ is enforced is examined in Problem Induction.

Step two: build a pooling service for the sub-threshold space. On Ethereum, the explicit 32 ETH threshold created structural demand for a protocol-level solution to sub-threshold participation.

Rocket Pool fills this gap: a permissionless, decentralised liquid staking protocol where an operator bonds as little as 4 ETH alongside pooled capital from passive stakers, and a smart contract assembles a full 32 ETH validator. The result is ~4,000 independent node operators and ~800K ETH staked — participants who would never have reached the threshold alone but who contribute meaningfully to Ethereum's consensus decentralisation.

The parallel suggests a concrete design direction for Cardano: a pool alliance mechanism, operating at the protocol level or as a standardised smart-contract layer, that lets sub-threshold participants combine operational commitment and capital to collectively cross the production threshold.

The components of such a mechanism are identifiable:

- Operator bond. A technically capable participant pledges what they can — say 100K ₳ — and commits to running infrastructure. This is their skin-in-the-game, analogous to Rocket Pool's operator bond.

- Capital matching. Delegators who want to support network decentralisation at a level above passive delegation contribute capital to the alliance. The pooled stake crosses the production threshold; the operator runs the pool.

- Transparent split. A declared, enforceable commission structure governs how rewards are shared between the operator and the alliance's capital providers — replacing the opaque fixed-cost-plus-margin mechanism with a legible contract.

- Collateral and accountability. The operator's bond is at risk: persistent underperformance or misconduct triggers a penalty visible to the alliance's capital providers, who can exit. The accountability channel that the current mechanism fails to create for passive delegators (The inversion) is built into the alliance structure by design.