CIP-0037 is the second stake-cap candidate in the bundle — same diagnostic target as CIP-0050 (POL.O2.F1: 78 % of staked ADA below 1 % pledge ratio; POL.O2.F2: pledge yield 0.68 %/yr against 2.3 %/yr passive), reached through a different primitive: a smooth saturation curve $\text{sat}(p) = \text{clamp}(\ell \cdot p, e \cdot \text{orig\_sat}, \text{orig\_sat})$ that grows with pledge, with a 20 % floor at the bottom and the V1 cap at the top.

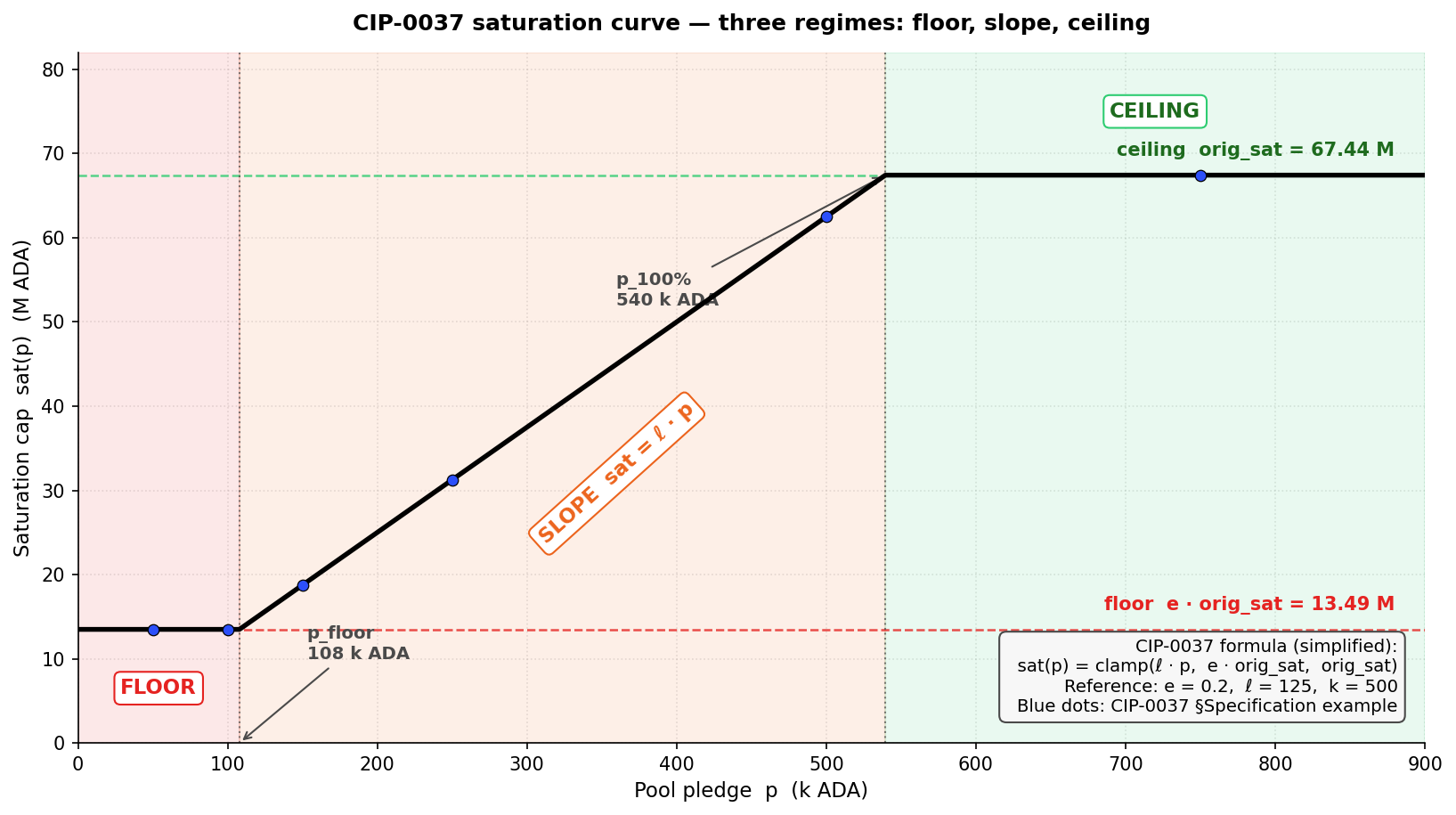

CIP-0037 replaces the static V1 saturation cap (~67 M ADA) with a saturation curve indexed on pledge. The curve has three regimes:

Three parameters control the curve — $e$ (floor), $\ell$ (slope), and $p_{100\%}$ (ceiling anchor). A hard fork is required; no pool re-registration.

Same problem as CIP-0050, framed differently. The CIP's own framing (Casey Gibson, 2021):

Operators have rationally decided pledge isn't worth the opportunity cost.

CIP-0037 makes per-pool reward capacity grow with pledge. Splitting a fixed pledge across many pools shrinks each pool's envelope — the incentive to expand a multi-pool fleet becomes self-defeating.

Pledge becomes a decisive input to the saturation cap, monotone on the slope regime, and the 20 % floor protects every pool below 13.49 M ADA (Dormant, Sub-block, Sub-reliable, and the lower half of the Healthy tier) regardless of pledge level. Zero-pledge pools keep one fifth of V1 capacity instead of dropping to zero.

Three scalars to calibrate $(e, \ell, p_{100\%})$ against CIP-0050's single dimensionless $L$ — and the ceiling anchor $p_{100\%} = 500\,000$ ADA is absolute, so its fiat cost slides with the ADA/USD rate (\$50 k at \$0.10/ADA, \$500 k at \$1.00/ADA, \$2.5 M at \$5.00/ADA). Any k change reshapes the entire curve via $\text{orig\_sat} = \text{Supply}/k$, forcing joint recalibration of all three parameters.

The remainder of the document walks the proposal in three steps: §4 quantifies what changes on mainnet today; Appendix A unpacks the formula, the three regimes (floor, slope, ceiling), and the structural kinship with CIP-0050; Appendix B documents the per-finding evidence with verdict tags.

The 20 % floor protects pools up to 13.49 M ADA. The lower half of the Healthy tier and everything below it stays whole at zero pledge.

Above 13.49 M, the same absolute pledge threshold (~108 k ADA) applies regardless of pool size. The harder a pool grows on delegation, the more aggressively the cap clips it at the median retail pledge ratio.

This appendix gives the full mechanical decomposition of CIP-0037: the formula in its simplified clamped form, the three regimes, structural kinship with CIP-0050, structural properties, and quantification at current mainnet parameters. The opener summarises the conclusions; this appendix carries the derivations and figures that back them.

CIP-0037 replaces the static $z_0 = 1/k$ saturation cap with a pledge-indexed saturation function. Simplified from the canonical source (see errata note below):

$$\boxed{\text{sat}(p) \;=\; \text{clamp}\bigl(\ell \cdot p,\;\; e \cdot \text{orig\_sat},\;\; \text{orig\_sat}\bigr)}$$

where $\text{clamp}(x, \text{lo}, \text{hi}) = \min(\text{hi}, \max(\text{lo}, x))$.

The reward-eligible stake becomes $\sigma' = \min(\sigma, \text{sat}(p))$; the reward curve then applies to $\sigma'$. The operator/member split is unchanged.

Three regimes fall directly from the clamp.

The blue dots on the curve in figure A.1 are the six numerical example points the CIP itself publishes in its Specification section — they lie exactly on the clamped piecewise curve.

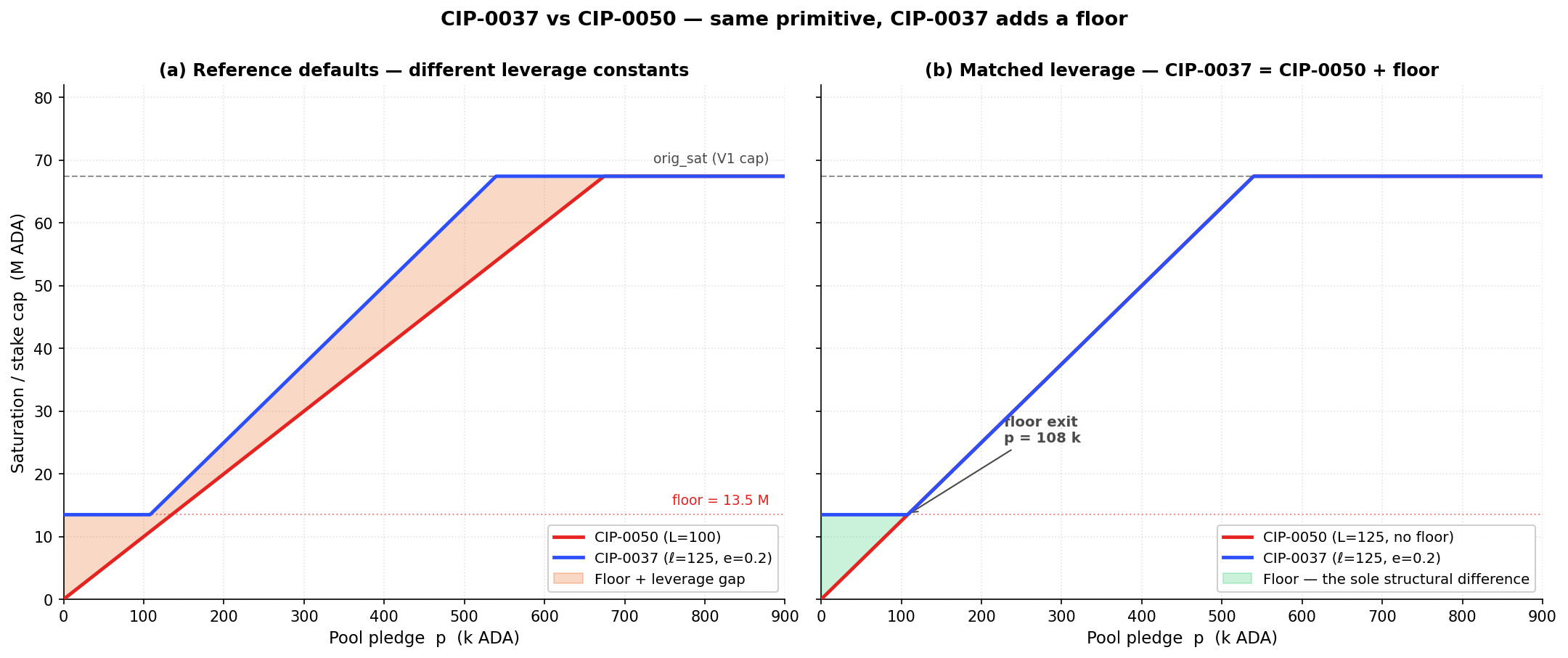

The slope is identical. Reference leverage differs only by convention ($\ell = 125$ vs $L = 100$). The sole structural difference is the floor:

Panel (a) uses each CIP's reference leverage ($\ell = 125$ for CIP-0037, $L = 100$ for CIP-0050) — the gap conflates the 25 % leverage difference with the floor. Panel (b) matches leverage at $\ell = L = 125$ to isolate the floor as the sole structural difference. Reading this correctly reframes the two proposals: CIP-0037 is CIP-0050 plus a floor. Every S1 / S2 / S3 finding in Appendix B carries across one-for-one, modulated by whether the floor binds in the regime considered.

All calibrations use reference parameters ($e = 0.2$, $\ell = 125$, $p_{100\%} = 500$ k, $k = 500$, $\text{orig\_sat} = 67.44$ M ₳).

$$p_{\text{floor-exit}} = \frac{e \cdot \text{orig\_sat}}{\ell} = \frac{0.2 \cdot 67.44 \text{ M}}{125} \approx 108\,000 \text{ ₳}$$

CIP's own worked case: 1 M ADA pledge budget at reference parameters.

Three cards organise the analysis: what the curve actually delivers (S1), the capital-capability bias from the Healthy tier upward (S2), and the governance, price-robustness, and entity-level gaps unique to this parameterisation (S3).

CIP-0050 makes pool-splitting strictly revenue-neutral: total reward cap across $N$ pools equals the single-pool cap, for any pledge budget.

The 20 % floor softens CIP-0037 at the very bottom — Sub-reliable pools and below stay whole even at zero pledge. That is a real advantage over CIP-0050's hard break.

From the Healthy tier upward, the picture inverts. The floor-exit threshold of ~108 k ADA is the same absolute amount for a 2 M pool and a 50 M pool. Mid-tier retail pools therefore need absolute pledge levels most operators simply do not have, and the cut bites harder than the floor's headline 20 % suggests.

The discrimination is by capital capability — same as CIP-0050.

CIP-0037 shares the same structural critique as CIP-0050: correct target (the pledge signal), correct layer (reward-distribution pre-split), but with capital-capability bias, small-pool viability risk, and an entity-level concentration gap.

Same precondition as CIP-0050: a fee-layer viability instrument must be active first to protect the retail population most exposed to clipping. The sequence:

The CIP proposes a saturation function $\text{sat}(p)$ that grows with pledge. Splitting a fixed pledge across more pools moves each pool left on the curve, reducing per-pool capacity.

CEN.O1

Multi-pool entities flourished (23 → 85 entities, 65% → 76% of productive stake) while single-pool operators struggle (555 → 291 pools, 39% → 24% of stake)

The designed entry → growth → established path is no longer observable. The productive set tracks a 700–1,000 band since epoch 300 (733 pools at epoch 623 as the threshold rises with total stake), with only 1.7% turnover per epoch — but composition has hardened underneath that flat aggregate. 83 attributed entities control 76.7% of productive stake (12 with 11+ pools alone hold 41.0%); multi-pool fleets grew from 23 to 85 while single-pool operators contracted from 39.1% to 24.4% of stake.

Three quarters of registered pools are economically irrelevant. 2,144 of 2,877 (75%) sit below the production threshold (~3M ADA) and together hold only 2.7% of stake · Three quarters of productive stake sits in 83 named entities. They control 76.7% through 449 productive pools (71 strict multi-pool + 12 attributed single-pool) — and the count is a lower bound (operators using fully separate per-pool infrastructure stay invisible)

9 findings

CEN.O2

When a Titan delegator switches pools, the whole pool moves with them — whale-funded pools swing ±20% between epochs (1 in 5 swings >50%) while retail pools barely move (±8%)

A pool's stake stability depends on who its delegators are — not on the market segment it competes in. In whale-funded pools (the 28 custodial-by-delegation pools, where the typical delegator holds ≥ 100K ₳), a single Titan-tier address (10M+ ₳) is large enough that when they move, the whole pool moves: stake swings ~±20% between epochs, and 1 in 5 of them swings more than 50%. The operator loses revenue predictability and the remaining delegators see their block-production rhythm wobble. Retail pools (broad small-delegator base) absorb churn smoothly — they only move ±8% between epochs. Custodial-by-extraction pools (≥ 99% margin) barely budge (±7%) because their delegators are locked in by inertia. What looks like delegator activity in the aggregate is mostly a handful of institutional treasuries shifting capital.

A single Titan delegator moving in or out can shake a whole pool — whale-funded pools swing ~±20% between epochs vs ±8% for retail. In the 28 custodial-by-delegation pools (typical delegator holds ≥ 100K ₳), stake moves by roughly ±20% between epochs, with 21% of them swinging by more than 50% — these are pools where a single address is large enough that its movement dominates the variance. Retail (809 pools, broad small-delegator base) is mostly stable (±8%) — no single delegator can move the pool. Custodial-by-extraction (79 pools, ≥99% margin) is the most inert (±7%) — stagnation, not active management

1 finding

CEN.O3

The delegator population is wildly skewed in stake — 1,000 of 1.36M delegators (0.07%) hold 57% of staked ADA, and 9× population growth has not shifted the shape

The delegator population is shaped like a power-law tail — almost all the staked capital sits in a tiny upper sub-population. Of the 1.36M active delegators, 1,000 (0.07%) hold 57% of staked ADA; the top 10,000 (0.74%) hold 79.2%; Gini = 0.976 — more concentrated than US wealth (~0.85) and comparable to the most unequal asset distributions in financial markets. The median delegator holds just 32 ADA while the mean is 16,055 ADA — a 500× gap that quantifies the skew. The population has grown 9× since epoch 300 without changing its shape: every cohort of new entrants has joined at the bottom of the distribution, leaving the top-1% share locked at 78–82%.

Half the delegator base stakes less than a single transaction fee at peak congestion. Median: 32 ADA. Mean: 16,055 ADA. The 500× gap measures the skewness of a power-law distribution where each tier above 10K ADA holds roughly 20% of total stake despite containing exponentially fewer delegators · The delegator population's stake is concentrated in its top 0.07%. 1,000 delegators (0.07% of the 1.36M population) hold 57% of staked ADA; the top 10,000 (0.74%) hold 79.2%. Gini = 0.976 — more concentrated than US wealth (~0.85) and comparable to the most unequal asset distributions observed in financial markets

3 findings

CEN.O4

Most delegators stay put for years — 42% have stuck with the same pool for 2.7+ years, only 21% switch within 25 days, and the population's switching rate is 75% below early Shelley

The delegator population settled long ago — most of it doesn't move. Tenure splits the population cleanly into three sub-groups: 42% have stayed with the same pool for 2.7+ years (201+ epochs), 21% switch within 25 days (≤ 5 epochs), 37% sit in the middle (somewhere between). Aggregate switching has collapsed 75% from 2,000–3,500 redelegations per epoch in early Shelley to 600–800 today — three regimes: experimentation → middle → mature. And almost all of that switching comes from the retail population: custodial and private pools barely move.

Pool-switching collapsed 75% from early Shelley. Redelegations fell from 2,000–3,500 per epoch (early Shelley experimentation) to 600–800 today — three regimes: experimentation (epochs 210–260) → middle period with hard-fork spikes (260–500) → mature settled market (500+) · The base splits cleanly into stickers and switchers, with a thin middle. 42% loyal (201+ epochs, > 2.7 years), 21% volatile (≤ 5 epochs, < 25 days), 37% moderate. The loyal majority anchors pool economics; the volatile tail generates the bulk of the churn signal

3 findings

CEN.O5

The bigger the delegation, the more it moves — whales (1M+ ₳) hold 65% of the staked supply and switch ~4× more often than small delegators

The bigger the delegation, the more often it moves. The smallest delegators (< 1K ₳) average just 0.67 pool switches over their lifetime — they delegate once and forget. Whales (1M+ ₳) average 3.06 switches — about 4–5× more. And whales hold 14.1B of the 21.8B staked supply (65%) — yet only 38% of that capital sits in long-term (201+ epoch) delegations. The bulk of the network's staked capital sits in the hands of its most actively-managed delegations. Pool operators depending on a few whale delegators therefore face structurally higher stake instability than those with a broad retail base.

Whales switch 4–5× more often than micro-delegators. Lifetime switches: <1K = 0.67, 1K–10K = 0.95, 10K–100K = 1.64, 100K–1M = 2.65, 1M+ = 3.06. Loyal share (201+ epochs): <1K = 82%, 1M+ = 39%. Switching intensity scales monotonically with stake size — small delegators delegate once and forget; large delegators actively manage their position · Most of the network's staked capital sits in delegations that move. Whales (1M+) hold 14.1B of the 21.8B staked total (65%), yet only 38% of that stake sits in loyal (201+ epoch) delegations — the rest distributes across moderate and volatile tenures. Pool operators dependent on a few large delegations face structurally higher stake instability than those with a broad base of small loyal delegators

2 findings

CEN.O6

The delegator population doesn't shop on price — half their switches produce zero yield change, switch direction is balanced (30.8% cheaper / 31.5% pricier), and 92% of long-term delegators sit in the cheapest 0–5% margin band

The delegator population behaves like passive parkers, not yield-shoppers. When delegators do switch, half (50.5%) land in pools with statistically indistinguishable yield (±5 bps; median ROS differential +0.02 bps — well below any threshold a delegator could observe). Switch direction is symmetric too: 30.8% go cheaper / 37.7% stay flat / 31.5% go pricier — no fee-chasing pattern. The one asymmetric move is by pool size (the population drifts toward larger pools regardless of price). And 92.1% of long-term delegators (201+ epochs) sit in the cheapest 0–5% margin band — the cheapest pools are also the stickiest, so loyalty and low fees coexist, they don't trade off. The DeFi sub-population is essentially absent: 99.83% of staked ADA is key-based; only 38M ADA across 399 script addresses is held by smart contracts.

Delegators cannot see what they're paying for — the yield signal is too flat to act on. Half of all switches (50.5%) produce zero yield change (±5 bps); the median ROS differential is +0.02 bps with an interquartile range of −0.47 to +0.55 bps. The signal is an order of magnitude below any threshold a delegator could observe, let alone optimise against · Operator take direction is balanced — no fee-chasing pattern is detectable. 30.8% of switches go to a cheaper pool, 31.5% to a more expensive one, 37.7% land at the same take. The take × ROS matrix's diagonal dominates (lower take → better ROS at 18.4%, similar → similar at 25.6%, higher → worse at 16.5%) — confirming take and ROS are two views of one signal, and that signal is too flat to drive behaviour

5 findings

CEN.O7

The non-participant population is 39.8 % of the supply, structurally inert, and held by a tightly-concentrated minority of custodians and legacy holders

The non-participant population — addresses controlling ADA that is not delegated to any pool — has been stable at 36–39 % of circulation for over 300 epochs (14.4 B ADA at epoch 623). Only 0.37 % of circulation is reachable by reward design (registered staking key but not delegated); the remaining 39.4 % sits in addresses that cannot delegate without a protocol-level change. The "unreachable" core is not a faceless retail tail — 246 wallets hold 74 % of it, top-3 alone hold 19 %; the addresses split cleanly into recognisable archetypes (exchange hot wallets, institutional cold storage, pre-staking-era legacy holders, DeFi vaults). The "addressable" pool collapses to ~2,100 active accounts and 0.06 % of supply once zero-balance shells and a single DeFi vault are removed. The reward mechanism's recruitment ceiling is narrow; meaningful re-engagement requires changing the address architecture, not the incentive curve.

The staking rate is structurally declining despite persistent net delegator inflows. The rate has fallen from 71% (epoch ~260) to 59% (epoch 623) — a 12 pp loss over ~360 epochs. Circulating ADA grew from ~32B to ~37B while staked ADA grew from ~23B to only ~22B; the non-participant pool is growing faster than the staking pool. · 14.36B ADA (39.8% of circulating supply) does not participate in staking — and only a sliver of that is reachable by reward design. The non-participant pool has been stable at 36–39% for over 300 epochs. Only 0.37% of circulation (134.6M ADA, 24,176 accounts) is nominally addressable by an incentive-design change — and even that figure shrinks under scrutiny (§5.5). The remaining 39.4% sits in addresses that cannot delegate without a protocol-level change.

8 findings

CEN.O8

The active submitter population is shrinking and concentrating into a smaller, more active core

The submitter population — addresses paying fees in any given epoch — collapsed from a peak of 790,335 actors (epoch 304) to 31,176 (epoch 627), a −96% contraction against only a 92% drop in transactions. The same population now transacts ~3.8× per epoch (vs ~2.0× at peak), and the address-to-transaction ratio fell from 0.88 (epoch 210) to 0.26 (epoch 627). The chain is not losing activity; the population doing it is shrinking while each surviving member transacts more often.

The submitter population peaked at 790K addresses and has since contracted by 96% — the chain runs busily, with a much smaller crowd. The population grew in step with transaction count through early Shelley, peaking at 790,335 unique addresses and 1,566,974 transactions at epoch 304 (the CNFT minting frenzy). From epoch 310 onward the population collapsed faster than volume: 101K submitters at epoch 384, 58K at epoch 500, 31,176 at epoch 627. Transaction volume fell only 92% over the same window — a population one twenty-fifth of its peak still sustains three quarters of the per-epoch transaction rate seen during 2023–2024. · Breadth is collapsing while per-actor intensity is rising — the same shrinking core just transacts more often. The address-to-transaction ratio fell from 0.88 (epoch 210) to 0.26 (epoch 627), and tx-per-submitter rose from ~2.0 (epoch 304) to ~3.8 (epoch 627). Cumulative Shelley-era throughput totals 118.07M transactions and 37.85M ADA in fees. The growth-trajectory signal is unambiguous: new addresses are not entering the fee-paying population at a rate that would sustain breadth — the same shrinking core is just transacting more often.

2 findings

CEN.O9

Two submitter sub-populations coexist: a stakeable head-count majority and a small non-stakeable minority that pays a third of the fees

At epoch 627, the stakeable majority — base-key (addr1q) addresses carrying a stake credential — is 73.3% of submitter head-count and pays 47.4% of fees. The non-stakeable minority — enterprise (addr1v, addr1w) and legacy Byron addresses that structurally cannot delegate — is only ~16% of head-count but generates 30.1% of fee revenue (averaged 622–627), and that share has not fallen below 14% since the Alonzo era. The reward pipeline taxes a sub-population it cannot reward.

By address count, the submitter population remains overwhelmingly stakeable — but the script segment has grown structurally. At epoch 627: 73.3% base-key (addr1q) addresses carrying a stake credential, 10.8% base-script (addr1z), 9.2% enterprise-key (addr1v), 4.9% legacy Byron, 1.6% enterprise-script (addr1w), 0.2% base-other. Compared to the earlier snapshot at epoch 384 (87% base-key, <1% script), the shift is clear — base-key dropped 14 pp while base-script grew from 0.4% to 10.8%. The count-based picture remains misleading: the small script population punches far above its weight in fee terms. · Roughly 30% of fee revenue is generated by addresses that structurally cannot delegate, and this share has been stable since Alonzo. Over the recent 6-epoch window (622–627): enterprise-script (addr1w) 17.0%, enterprise-key (addr1v) 10.8%, legacy Byron 2.3% — totalling 30.1%. The non-stakeable fee share has oscillated between 18% and 44% since epoch 300, averaging ~25%; the structural floor is set by DeFi contract activity, the ceiling by speculative episodes. At no point since Alonzo has it fallen below 14% — the reward mechanism taxes a constituency it excludes.

2 findings

CEN.O10

A small DeFi-script sub-population — ~3,800 contracts at epoch 627 — generates a third of the fee base

The script-using sub-population — base-script (addr1z) and enterprise-script (addr1w) addresses — is 3,851 actors at epoch 627 (12.4% of submitters) and generates 36.0% of epoch fees. Across the full post-Alonzo era it represents 12.5% of transaction count but 29.6% of cumulative fees. The per-address fee rate of an enterprise-script submitter (12.1 ADA/epoch) is 14× that of a base-key submitter (0.83 ADA/epoch). The chain's fee floor is supported by a population of roughly 3,800 smart contracts — a population dimension the current incentive design does not address.

Script transactions are 12.5% of post-Alonzo count but 29.6% of cumulative fees — the DeFi economy pays a 2.4× per-transaction premium. The premium peaked above 3× during the Alonzo era (epochs 310–340), when fewer than 30% of transactions commanded over 60% of fees. It has moderated to ~1.5× in recent epochs but remains structurally above parity. For the sustainability argument, this means per-transaction fee intensity is coupled to script adoption — a variable the current incentive design does not address. · At epoch 627, ~3,800 script addresses (12% of submitters) generate 36% of fee revenue — the pipeline depends on the continued operation of these contracts. Specifically: 490 enterprise-script + 3,361 base-script = 3,851 actors (12.4% of the submitter population) generated 14,481 ADA in fees — 36.0% of the epoch total. The per-address rate of an enterprise-script submitter (12.1 ADA/epoch) is 14× that of a base-key submitter (0.83 ADA/epoch). The script population grew sixteen-fold since epoch 384 (0.7% → 12.4%) while their fee share held steady around one third — the per-address premium has moderated but the structural dependency has deepened.

2 findings

CEN.O11

The fee-paying population is bimodal: a heavy-paying core of a few hundred high-frequency actors and a long tail of ~147K small contributors

Over epochs 622–627, the top 10 addresses generate 20.0% of fees and the top 500 generate 58.4% — out of ~147K active submitters. The heavy-paying core is recognisable: a MinSwap DEX-script address leads, followed by addresses tied to the NUFI, TITAN, BERRY, and OYSTR pools and several enterprise-script DEX contracts and bot wallets. The concentration is heavy-tailed but below the delegation Gini of 0.976. 500 addresses out of 147K (0.34%) pay the majority of fees — the fee floor depends on a sub-population small enough to know by name.

The top 10 addresses pay 20% of all fees; the top 500 (out of ~147K) pay 58%. Over epochs 622–627, 500 addresses out of ~147K (0.34%) pay the majority of fees. Concentration is heavy-tailed but less extreme than delegation stake (Gini 0.976). Compared to the prior 618–623 window (top-10 = 24.3%, top-500 = 60.8%), the recent window shows a mild de-concentration of 4 pp at the top — driven by a single very-high-volume address whose activity tapered. The fee base sits on a few hundred high-frequency automated actors, not a diffuse retail tail. · The top 10 fee payers ran 110,739 transactions over 6 epochs (16.1% of volume) — fee-pot stability hinges on a population small enough to know by name. The top 50 ran 219,720 transactions (32.0%) over the same 6-epoch window. The top fee payers are dominated by recognisable archetypes: a MinSwap DEX-script address leads at 12,105 ADA over 6 epochs; pools tied to NUFI (NuFi exchange-style operator), TITAN, BERRY, and OYSTR appear among the top 10 alongside enterprise-script DEX contracts and bot wallets. The fee floor of the network depends on a population of ~10 actors whose churn risk is not modelled by any incentive parameter.

2 findings

CEN.O12

The fee-paying population and the delegator population barely overlap — funders and beneficiaries are largely different people

Joining the submitter set (~147K addresses, epochs 622–627) to the 1,352,113 active delegators at epoch 627 reveals the population gap: only 41.8% of fee revenue comes from currently-delegating addresses; 28.1% from base addresses whose stake credential is not in the delegation set; 30.1% from addresses with no stake credential. From the delegator side, only 3.1% of the 1.352M delegators submit any transaction in a 6-epoch window. Fewer than 4 ADA in every 10 ADA of fees flow back to the population that paid them through any reward channel.

Only 41.8% of fee revenue comes from currently-delegating addresses; the remaining 58.2% comes from addresses outside the delegation set at the snapshot epoch. Across epochs 622–627, the 1.352M delegators at epoch 627 contributed 41.8% of fee revenue (92,538 ADA out of 221,565). The stakeable-but-inactive segment (base addresses whose stake credentials are not in the delegation set) contributed 28.1% (62,340 ADA). The structurally non-stakeable segment (enterprise + legacy) contributed 30.1% (66,684 ADA). The mismatch is symmetric on both sides — the funding base does not match the reward base. · Only 3.1% of delegators submit any transaction in a 6-epoch window — 96.9% of delegators are passive holders. Of the 1,352,113 active delegators at epoch 627, only 42,082 appear as the first input of any transaction during epochs 622–627 (a 30-day window). The remaining 1,310,031 (96.9%) hold stake, accrue rewards, and never touch the chain. From the other side, the submitter base has 76,561 unique stake credentials over the same window, of which 42,082 (55.0%) are in the delegation set — the rest carry a stake credential that has never been delegated, has been deregistered, or sits idle.

3 findings

TRE.O1

The epoch pot rests on a single source — and that source has crossed its half-life

The protocol's reward formula admits three inputs to the epoch pot — monetary expansion, transaction fees, deposits. In practice only one matters. Monetary expansion supplies ~99.8% of the pot; fees contribute ~0.17% and even at full realistic network capacity would cover only 1.3% of the expansion term (a ~100× structural gap in fee revenue terms); the deposit channel is unmeasurable at epoch granularity. Stake pool operators assemble the pot reliably (η = 0.977 average — the cooperative-behaviour gate is satisfied but never binding). The budget therefore depends almost entirely on the reserve, which is shrinking by 0.3% every epoch.

Monetary expansion is the only material input to the pot — supplies ~99.8%, every epoch, since Shelley. Outside a single recent anomaly at epoch 620 (~5% fee share), fees have never crossed 3% — even during peak NFT/DeFi activity. The pot's trajectory is therefore tied almost entirely to reserve stock and ρ; the formula admits three sources but the mechanism behaves as if it had one · Fee revenue is structurally insufficient — closing the gap requires fee revenue to grow ~100× (two orders of magnitude). Fees contribute ~0.17% of the pot at epoch 623, and even the realistic capacity ceiling (~254K ADA/epoch at 3.1 TPS × 432K s × 0.19 ADA/tx) covers only ~1.3% of the reserve expansion term (~19.23M ADA). Closing the gap requires a throughput upgrade (Leios), a structural shift in transaction demand, and higher per-tx pricing (no single lever suffices); until that crossover, the second source named in the SL-D1 formula is a rounding error

4 findings

TRE.O2

The reserve has crossed its half-life — the budget is on an exponential decay schedule

The reserve has fallen from 13.29B to 6.45B ADA — −51.43% in ~5.7 years of Shelley operation. The decay is exponential: every epoch draws 0.3% of whatever remains, so the nominal pot has already halved (from ~39.9M to ~19.36M ADA/epoch) and continues to shrink mechanically even when participation does not. Significant reward pressure is projected at epochs 1000–1200 (~2028–2029) when expansion-driven rewards stop matching today's scale.

The reserve is half-depleted in 5.7 years and the nominal expansion has already halved. Stock has fallen from 13.29B → 6.45B ADA (a −51.43% decline) over ~5.7 years; the nominal monetary draw has dropped from ~39.9M → ~19.36M ADA/epoch. Because the formula draws a fixed 0.3% of remaining reserve, the decay is exponential — the absolute pot keeps shrinking even when participation does not. The single-source budget identified in TRE.O1 is now visibly thinning, on a schedule the formula cannot reverse · Significant reward pressure begins at epochs 1000–1200 (~2028–2029). At current parameters and participation, the reserve reaches ~2B ADA in this window — at which point per-epoch rewards drop materially. Full depletion is projected around epoch 3500 (~2040s). The window for governance to intervene before the pot becomes too small to incentivise meaningful staking is on the order of 3–4 years

2 findings

TRE.O3

Less than half of the pools pot reaches operators and delegators — the rest props up the reserve as a side effect of low participation

Of the 15.39M ADA/epoch allocated to the pools pot, only 6.78M ADA (~44%) actually reaches operators and delegators; the remaining ~8.61M returns to the reserve. Cumulatively over 413 epochs, 4.61B ADA has flowed back this way — ~71% of the current reserve stock exists because rewards were not fully distributed. The primary driver is upstream of the formula: ~16.8B ADA (~43.6% of circulating supply) does not participate in delegation at all. The reserve has lasted as long as it has because the system has been failing to pay out — adoption that pulls inactive stake into the game would accelerate depletion.

Less than half of the pools pot reaches its intended recipients. Of the 15.39M ADA allocated to the pool side at epoch 623, only 6.78M ADA (~44%) is distributed to operators and delegators; the remaining ~8.61M returns to the reserve. The mechanism therefore operates at less than half of its design throughput in steady state — the SL-D1 distribution rules are intact, but the pool-by-pool conditions for full payout are not met across most of the landscape · Cumulative undistributed rewards account for roughly three quarters of the current reserve stock. Over 413 epochs the return-to-reserve channel has accumulated 4.61B ADA — about 71% of the 6.45B ADA the reserve holds today. This buffer is a side-effect of incomplete distribution, not a design feature: the reserve has lasted as long as it has largely because the system has been failing to pay out. Any reform that improves distribution efficiency therefore accelerates depletion

3 findings

TRE.O4

The two parameters that govern this whole layer have never been adjusted

The treasury rate (τ = 20%) and the monetary expansion rate (ρ = 0.3%) have remained at their day-one values for the full ~5.7 years of mainnet operation. Neither has been the subject of a formal governance proposal. The current pot, treasury inflow, and reserve trajectory all reflect parameter choices made for a network with very different supply, participation, and pool-count conditions — and the absence of any review path is itself a structural feature.

Treasury rate (τ = 20%) and monetary expansion rate (ρ = 0.3%) have never been adjusted since Shelley. Both parameters were set on 2020/07/29 and have remained at their day-one values across ~5.7 years of mainnet operation. Decentralisation d was gradually reduced to 0 (epochs 208–257) and k was raised from 150 to 500 (Aug 2020) — but the reward-level parameters that drive every quantity in this section remain frozen, and neither has been the subject of a formal governance proposal

1 finding

POL.O1

Participation gap and unused pledge-incentive budget return 54% of the pool pot to reserve

Only 6.79M of 15.53M ADA/epoch reaches operators and delegators — a 44% distribution efficiency.

Two causes dominate the loss: the participation gap (unstaked ADA) returns 4.91M ADA/epoch — 31.6% of the pot, upstream — outside formula control; the unused pledge-incentive budget returns 3.43M ADA/epoch — 22.1% of the pot, 95.6% of the bonus allocation wasted.

All other causes are an order of magnitude smaller — pledge-not-met confiscation (2.1%), performance (0.5%), oversaturation (0.3%).

Less than half the pool pot reaches its targets. Only 6.79M of the 15.53M ADA per epoch budgeted for distribution actually reaches operators and delegators — a 44% distribution efficiency. The other 56% returns to the reserve unused · ADA that isn't staked at all is the single largest source of waste. Every epoch, 4.91M ADA is forfeited because roughly a third of the supply sits unstaked — that's 31.6% of the pot, returned to the reserve before the formula even gets a chance to distribute it

4 findings

POL.O2

Pledge is unused at scale and structurally unfair across pool sizes

78% of staked ADA sits in pools with pledge ratio < 1%; the stake-weighted median is 0.07%. The bonus that should reward commitment is silent for almost every operator.

The unfairness is algebraic, not just empirical. The activation function A(ν, π) = ν² · π[1 - π(1 - ν)] has three structural defects: a permanent quadratic size penalty ν² that scales every pledge ratio against pool size; a non-monotone regime in π for any pool below half-saturation, where pledging more than π^ = 1/[2(1-ν)] pays less; and a cubic collapse to ν³ at full self-pledge, where the strongest possible commitment is paid the worst-case scaling on size.

The combined consequence: yield on pledge capital tops out at 0.68%/yr at saturation (vs. 2.3%/yr passive delegation), and 3.4M ADA/epoch* (22% of pot) reserved for the bonus returns to reserve unclaimed.

Almost no operator pledges meaningfully. 78% of staked ADA sits in pools where the operator pledges less than 1% of the stake they manage; the stake-weighted median pledge ratio is 0.07% · Pledging earns less than passive delegation, even at maximum scale. A fully-saturated pool whose operator pledges the entire saturation amount earns just 0.68%/yr on that pledged capital — below the 2.3%/yr anyone can earn by passively delegating

6 findings

POL.O3

Three structural thresholds shape pool space: production (physics), viability (economics), saturation (formula)

Three thresholds emerge from the protocol's own mechanics and partition the pool population. Each has a different nature and a different mutability profile.

Production threshold (~3M ADA) —

physics, emergent. The stake at which a pool produces ≥1 block per epoch with

95% probability (λ=3 in the Poisson process — blocks are produced reliably enough for yield to be a usable signal for delegators). Not a protocol parameter; rises with active stake (to ~5.35M at full supply). The 1-block-expectation point (~1M ADA) is a special case at the bottom edge of this regime — below it, pools produce less than one block in expectation per epoch.

Viability threshold —

economic, and it moves; sits structurally above the production threshold. The protocol's

minPoolCost floor (currently 170 ADA, halved from 340 at epoch 445 / 2023-10-27; most pools still set 340) gives a

nominal break-even at ~1.1M ADA — but this is just the formula's internal floor. Real economic viability requires covering

infrastructure (~1,320–3,240/yr for block-producer + 2 relays + monitoring) plus

operator labour at market DevOps/SRE rates (~5,160/yr minimum at 10 hrs/mo × 43/hr) — totalling

~7,160/yr minimum, easily doubling for a more demanding setup. Because operator costs are fiat-denominated while revenue is in ADA, the real target tracks the ADA/USD price (~28,600 ADA/yr at 0.25; ~71,600 at0.10). At today's prices no single-pool tier comfortably clears it; competitive compensation begins only at the 2-pool MPO tier.

Saturation cap (77M ADA = z₀ = 1/k) —

formula, fixed by parameter. The reward ceiling per pool, designed to limit any single pool's share of network reward.

The cleaner future state would collapse viability into production, leaving only the physics-grounded boundary. This is harder than it sounds — zeroing

minPoolCost removes the protocol-imposed floor, but the real labour-cost floor remains unless a structural mechanism (e.g., Rocket-Pool-style shared operations) is introduced. See

§1.2.4.4.1 Enforce the production threshold.

The boundaries are

dynamic — they shift with active stake, fixed costs, k, and the ADA/USD price — so any CIP must be evaluated against where they move, not against a snapshot.

The production threshold is physics-based — emergent from slot-leadership, not a parameter. At today's active stake (~21.18B ADA), regular block production starts at ~3M ADA, the stake level at which a pool has a 95% probability of producing at least one block per epoch (λ=3 in the Poisson process) — the point where yield is usable as a delegator signal. The 1-block-expectation point (~0.97M ADA) is a special case at the bottom of the regime: below it, pools have less than one expected block per epoch and rewards are noise, not signal. The threshold rises with active stake — at full supply (~38.5B ADA), the 3-block point climbs to ~5.35M ADA, pushing more pools below it · Operator-viability is volatile and tracks the ADA/USD price; at today's prices it coincides with the production threshold, but separates upward when ADA falls. A single-pool operator needs to extract roughly 390 ADA/epoch today (~7,160/yr cost floor — infrastructure ~1,320–3,240/yr + DevOps labour ~5,160/yr min — at0.25 ADA). At the production threshold (~3M ADA stake), the pool generates ~2,145 ADA/epoch on average, more than enough — viability and production coincide. At lower ADA prices the cost in ADA rises, and the reliable-income floor rises above production. The threshold is therefore not drawn as a fixed line in the rest of this document; it is treated as a separate volatile concept whose stability is a question for the V2 spec, not the diagnostic

5 findings

POL.O4

A 73% sub-block tail (useless to consensus) and a 27% productive segment (unreadable without entity-level investigation)

The pool population splits cleanly at the production threshold, and the two segments answer different questions.Below the production threshold (~3M ADA): a sub-block tail invisible to consensus. 1,987 pools (73% of all pools with stake) sit below the 95%-block-probability bar and produce blocks too sporadically to be useful for the consensus protocol — they hold only

2.7% of active stake and exist as ghost capacity the protocol admits but cannot reliably activate. Below this threshold, a delegator cannot read a meaningful yield signal from any single pool — Poisson noise dominates the mean.

Above the production threshold: the productive segment cannot be read pool-by-pool. 731 pools (27%) hold

96.6% of staked ADA and carry the network's actual block production. But each pool appears on-chain as if it were independent, while in fact multi-pool entities run fleets — pool count is therefore a poor proxy for operator count, and pool-level metrics conceal entity-level concentration. The entity-level breakdown — counts, archetypes, who responds to the pledge signal — is the subject of

POL.O5 — entity-level analysis.

1,987 pools (73%) sit below the production threshold (~3M ADA) and produce blocks too sporadically to carry consensus reliably. At the production threshold a pool has a 95% probability of producing ≥1 block per epoch (λ=3); below it Poisson noise dominates and yield is statistical noise. Collectively these pools hold only 2.7% of active stake — ghost capacity the protocol admits but cannot reliably activate; neither delegators nor the consensus layer can read a meaningful signal from any single pool in this segment · The productive segment (731 pools, 27%) holds 96.6% of staked ADA — the actual consensus-carrying population. This is the segment any reform of k, the pledge curve, or the saturation cap actually moves. Pool count is not stake share: the inversion of headline pool count vs. stake share is the defining structural feature of the landscape

3 findings

POL.O5

83 multi-pool operators control 76.7% of productive stake — and almost none of them pledge

83 attributed entities operate 449 productive pools holding 16.24B ADA — 76.7% of productive stake.

The pledge picture is stark: of the 48 entities with enough capital to ever fill a pool to saturation, 42 sit at zero-pledge (pledge ratio < 2%), holding 12.20B ADA combined.

Architecture explains part of it: 10 of those 42 (CEX + IVaaS — Coinbase, Binance, Figment, Kiln…) hold 7.39B ADA they legally cannot pledge — exchanges custody retail balances, institutional validators run client assets. But that is only half the story. The other 32 are sovereign saturation-scale MPOs holding 4.80B ADA (22.7% of productive stake) that could pledge meaningfully but choose not to — they forfeit ~556K ADA/epoch in pledge bonus and absorb the cost. The architectural barrier is real; the strategic abandonment is larger as a share of the entities that could play. Only 2 of the 48 MPOs actually pledge most of their stake (≥80% pledge ratio) — Cardano Foundation (which pledges out of institutional duty, not in response to the formula) and Adalite Platform. Among private operators making an economic decision, the pledge mechanism currently succeeds on exactly one entity (Adalite).

Three quarters of the network's productive stake sits in 83 named entities. They operate 449 productive pools (≥3M ADA at epoch 623, the production threshold) holding 16.24B ADA — 76.7% of productive stake. 71 are strict multi-pool fleets; 12 are single-pool operators attributed by ticker, metadata, or relay clustering. The remaining 23.3% (4.94B ADA across 284 pools) sits in unattributed single-pool operators — attribution is a lower bound · 48 MPO entities concentrate 14.55B ADA — 68.7% of productive stake — in operators each big enough to fill a saturation cap. These are the saturation-scale MPOs (aggregate stake ≥ z₀ ≈ 77\textM ADA). Concentration at the entity tier is sharper than the 76.7% headline once the 35 sub-saturation entities (1.69B ADA, multi-pool by form but single-pool-like in economics) are stripped out. The top 5 of the 48 alone hold 5.44B ADA — 25.7% of productive stake (Coinbase, CHUCK BUX, Figment, Binance, Kiln); the top 10 hold 39.1%. The split is purely structural — pledge is taken up next

7 findings

POL.O6

Only 284 productive single-pool operators remain — and almost none of them pledge (like MPOs)

The "741 healthy pools" headline was 3× inflated. Strip out the fleet pools that were actually being run by multi-pool entities, and only 284 productive single-pool operators remain (productive = pool stake ≥3M ADA at epoch 623, the production threshold).

Almost none of them pledge. 80.6% of single-pool productive stake sits at zero-pledge (< 2% pledge ratio). This is not irrational — at single-pool scale, the pledge bonus pays less than passive delegation, so locking ADA into the pledge is dominated. They are responding correctly to weak incentives, not failing to play.

Only 51 operators sit in the middle (pledge ratio between 2% and 30%) — the narrow group a parameter reform could plausibly move. Everyone else is either above the bar already (very rare) or below it (zero-pledge).

And the segment is shrinking. Its share of active stake fell from 28.0% → 25.0% since epoch 583 — capital is flowing toward MPO fleets, not toward the single-pool operators the mechanism was designed for.

The competitive field of single-pool operators is 3× smaller than the Incentive Mechanism Analysis headline. Lopez de Lara reported 741 'healthy' pools as evidence of a functioning incentive landscape; once MPO fleet members are stripped out, only 284 single-pool operators remain. 61% of the headline were fleet pools — operating under entity-level strategies (delegation source, fee setting, pledge), not the single-pool economics the headline was supposed to be about · At single-pool scale, pledging is rationally priced as not worth it. 80.6% of single-pool productive stake (227 of 284 pools) sits in pools whose self-pledge is less than 2% of the stake they manage — call this zero-pledge: the operator has effectively declined the pledge bonus. The economics explain why: at single-pool scale, locking own ADA into the pledge yields at best 0.68%/year while passive delegation pays ~2.3%/year, so the pledge is dominated by the alternative use of capital at every realistic ratio. These operators are not failing to pledge — they are correctly responding to a formula that prices their effort below the delegation alternative.

4 findings

POL.O7

The pledge mechanism reaches only 36% of stake — and the 64% outside it splits into three populations no single parameter can pull back in

The pledge bonus was designed to discipline operator behaviour across the network. In practice it reaches only 36% of active stake (7.89B ADA) — single-pool operators plus the few MPOs that pledge meaningfully.

The other 64% is unreachable for three different reasons, each requiring a different fix:

(i) Architectural — 10 entities, 7.39B ADA. CEX + IVaaS legally cannot pledge — exchanges custody retail balances, institutional validators run client assets they don't own.

(ii) Strategic — 32 sovereign saturation-scale MPOs, 4.80B ADA. Community fleets, independent MPOs, multi-brand fleets, ecosystem stewards. They could pledge — they choose not to because the bonus pays less than passive delegation at their scale.

(iii) Sub-scale — 35 sub-saturation MPOs, 1.69B ADA. Aggregate stake below one saturation cap; the pledge bonus is mechanically too small at their size to register.

77 of 83 attributed entities sit in one of these three buckets. Conflating them into a single "raise a₀" debate is why parameter reform alone keeps producing the same equilibrium.

The pledge mechanism's actual reach is 36% of active stake — 7.89B ADA. Strip out the entities that don't respond to the pledge signal, and what remains (single-pool operators + the few MPOs that do pledge meaningfully) carries 7.89B ADA out of ~21.7B active. The other 13.89B ADA — 65.6% of productive stake — is held by entities the bonus does not reach. The mechanism was designed to discipline operator behaviour across the whole network; in practice it operates on roughly a third of it. · MPO non-response splits into three distinct populations — confusing them is what keeps reform from working. Architectural: 10 entities (CEX + IVaaS) holding 7.39B ADA that cannot pledge by law/business model — exchanges custody retail balances, institutional validators run client assets they don't own. Strategic: 32 sovereign saturation-scale MPOs holding 4.80B ADA that could pledge but choose not to — at their scale the bonus pays less than passive delegation. Sub-scale: 35 sub-saturation MPOs holding 1.69B ADA whose entire fleet cannot fill one saturated pool — pledging is mechanically too small to matter. These are three different problems wearing the same label

3 findings

OPE.O1

The flat fee (fixed cost) dominates operator revenue — but governance sets it, and operators resisted the last cut

The flat fee delivers 60% of retail operator revenue — yet operators don't compete on it. 89.5% of pools pick one of two floor values (the ones governance allows), so the parameter is effectively a governance-set price, not a competitive lever. When governance halved the floor from 340 ₳ to 170 ₳ in 2023, only ~36% of operators moved to the new floor — 64% still declare 340 ₳ today, 178 epochs (~1.5 years) after the cut. Operators are slow to follow even governance, and they actively resisted lowering the price the cut was meant to deliver to delegators.

The passive channel dominates the active one — the flat fee delivers 60% of operator revenue, the commission only 40%. Across the retail market, the fixed ₳/epoch flat fee accounts for 60% of operator revenue; the proportional commission accounts for the remaining 40%. The channel that dominates revenue is the one operators almost never touch. · Governance halved the floor 178 epochs ago — 64% of pools have not moved. The minPoolCost floor was halved from 340 ₳ to 170 ₳ through a successful governance action. 178 epochs later (~1.5 years), 64% of pools still declare 340 ₳ — including most of the largest entities. The price most operators charge is not a pricing decision; it is a governance setting they never revised.

5 findings

OPE.O2

The commission (margin) is doing two unrelated jobs: pricing a service on one side, privatising a pool without pledging on the other

The commission was designed as the operator's pricing tool: set a rate, charge it on each reward. On mainnet that role has split in two. 87% of pools use it as intended — commission ≤ 10%, pricing the service. 12% of pools set it ≥ 99%, taking essentially all rewards regardless of who delegates: a private pool funded by delegation, functionally equivalent to a self-pledged pool but without locking any capital. The 89-percentage-point range between the two uses is essentially empty (only 12 pools). The protocol exposes a continuous parameter; operators reduce it to two unrelated economic stances — price a service, or quietly privatise the pool.

The commission distribution is bimodal with an 89pp empty middle. 87% of pools set a commission at or below 10%; 12% set ≥ 99% (privatisation). The 89-percentage-point range between 10% and 99% contains only 12 pools. No economic attractor exists between competitive pricing and total extraction — operators either compete or fully privatise their pool, and almost no one in between · The market self-organises into four discrete tiers, not a continuous price distribution. No-commission (170 pools, 17.9% — almost certainly self-pledged), competitive (658 pools, 69.1% — at or below 10%), no man's land (12 pools, 1.3% — between 10% and 99%), privatisation (112 pools, 11.8% — at or above 99%). The four bands are an emergent equilibrium, not a design choice — the formula offers a continuous parameter and operators reduce it to four economic stances.

2 findings

OPE.O3

21% of productive stake is custodial — three mechanisms, three economics

21.1% of productive stake sits in pools where the operator effectively

keeps the rewards rather than delivering them to a retail delegation market. The delegation flow exists on-chain, but it isn't doing the work the formula assumes — the operator is. Three on-chain-detectable mechanisms achieve this, with very different per-entity economics:

(i) By pledge — self-funded pools. 10 entities self-stake their own pools (operator owns ≥95% of the delegation). They capture 100% of rewards because

they are the delegators. Median:

1.76M ₳/yr per entity.

(ii) By extraction — near-100% commission. 57 entities set the commission ≥ 99%, taking essentially all rewards regardless of who delegates. The pool is funded by delegation, but the operator collects everything (see

OPE.O2). Median:

282K ₳/yr.

(iii) By delegation — whale-only pools. 15 entities operate pools where the

typical (median) delegation exceeds 100K ADA — meaning the "delegators" are a small circle of whales, not retail. The pool serves an inner circle, not the open market. Median:

29K ₳/yr.

The three mechanisms produce three very different revenue scales (60× spread), but share the same underlying property: the open delegation market is not allocating this stake — the operator is. A fifth of productive stake is custodial — and it splits into three distinct mechanisms, not one. 79 entities operating 143 pools hold 4.55B ADA — 21.1% of productive stake in custodial pools. The split: (i) by pledge (10 entities, 36 pools, 1.59B — operator self-funds the pool); (ii) by extraction (57 entities, 79 pools, 2.04B — high commission on inert delegators); (iii) by delegation (15 entities, 28 pools, 0.92B — typical delegation ≥100K ₳). Each mechanism is detectable from on-chain observables and produces a different operator economics · The median delegation is what separates retail from custodial — not the mean. Custodial-by-delegation flags pools where the per-pool median delegation (db-sync epoch_stake) is ≥ 100K ₳ — i.e., where the typical delegator is a whale, not the average dragged up by one whale. For comparison, a delegation of 50K ₳ is already in the top 1.5% of all delegations on the network. The median measures the delegator's experience; the mean measures capital concentration. They are not the same signal.

3 findings

OPE.O4

The retail market is 79% of stake and the typical delegator holds 87 ₳

Once custodial pools are filtered out, the retail market is 809 pools, 516 entities, 17.02B ADA and 1,272,836 delegators — with a median delegation of 87 ₳ that is remarkably uniform across operator types, from independent single-pool to Coinbase and Binance.

Once custodial pools are filtered out, the retail market is bigger than mean-based estimates suggested — and it includes institutions. 809 retail pools, 516 entities, 17.02B ADA, 1,272,836 delegators. The retail-by-median-delegation classification keeps Coinbase, Binance, Kiln and other institutional operators inside the retail market — because their typical delegator is a small holder, even if the institutional brand is large. The retail market is the population the mechanism was designed for; it is the population every reform has to address · The typical retail delegator holds 87 ₳ — and the median is remarkably uniform across operator types. The median retail delegation across the entire 1.27M-delegator population is 87 ₳. Per-operator-type medians range from 45 to 962 ₳ — a tight 20× span across pool types from independent single-pool to Coinbase. Retail delegators are small, homogeneous, and yield-insensitive at this scale — any reform that prices below 87 ₳/year of incremental yield will not change their behaviour

2 findings

OPE.O5

Delegators pay 18× more for the same return

A sub-reliable delegator pays 48.3% effective price for 2.04% net return; a near-saturation delegator pays 2.7% for 2.34% — 18× the price for 0.30 percentage points of extra yield. Net return converges to 1.95–2.34% across the entire retail market — a signal too narrow to discipline pricing.

A delegator pays 18× more for 0.30 percentage points of extra yield. A delegator in a sub-reliable pool pays a 48.3% effective price (flat fee + commission as % of pool reward) for a 2.04% net return. A delegator in a near-saturation pool pays 2.7% for 2.34% — 18× lower price for 0.30pp more return. The effective price is a mechanical artefact of pool size (the flat fee's 1/σ regression), not a market signal — operators are not pricing competitively, the formula is pricing them · Net return converges to a narrow 1.95–2.34% band across the entire retail market — the signal is too weak to drive delegation. Regardless of pool size, operator type, or pricing plan, a retail delegator's net yield ends up between 1.95% and 2.34% — a 0.39 percentage point spread across the whole market. At this resolution, the yield signal cannot discipline operator pricing — delegators are not chasing 0.4pp of return; they are picking on visibility, brand, or convenience

2 findings

OPE.O6

Stake pool operator profitability ranges from 24K to 1M ₳/yr — operators who charge the most earn the least

Operator revenue scales with fleet size, not price — the sub-reliable single-pool operator absorbs 48.3% of pool rewards for 24,820 ₳/yr, while an 11+ pool MPO absorbs 7.7% for 1,035,496 ₳/yr (42× more revenue at 6× less price). No single-pool operator in the retail market earns a competitive wage.

The operators who charge the most earn the least — and vice versa. A sub-reliable single-pool operator absorbs 48.3% of pool rewards but earns only 24,820 ₳/yr. An 11+ pool MPO absorbs only 7.7% of pool rewards but earns 1,035,496 ₳/yr — 42× more revenue at 6× less effective price. The flat fee penalises small-pool delegators without compensating the operators who run those pools — both sides of the small-pool transaction lose · MPO revenue scales horizontally (more pools), not vertically (higher price). The 11+ pool bracket captures 26.5% of retail rewards through 7 entities. Their per-pool fee is the same 170/340 ₳ floor everyone else uses — they win by running more pools, not by pricing differently. Fleet size, not pricing, drives MPO operator economics — meaning a reform that targets pricing leaves fleet revenue untouched

4 findings

OPE.O7

Delegation follows visibility, not return

Delegators do not chase yield — 65.9% sit in hollow MPO pools at 2.18% net return while hollow single-pool near-saturation peers offer 2.34%. The pledge premium is negative once the flat fee drag (1.06pp for balanced vs 0.47pp for hollow) is priced in.

Two thirds of retail delegators sit in pools that pay less than the alternative — yield is not what they are choosing on. 65.9% of retail delegators sit in hollow MPO pools at 2.18% net return; hollow single-pool near-saturation pools offer 2.34% — 0.16pp more — and yet hold only 2.7% of delegators. Delegators are not chasing yield — they are picking on visibility, brand, exchange convenience, or default selection. The return signal does not drive delegation · The pledge premium is negative in the retail data — balanced operators deliver less net return than hollow ones. Balanced (genuine pledge commitment) operators deliver a median net return of 1.98%; hollow operators deliver 2.08%. The reason is mechanical: balanced single-pool operators incur a 1.06pp flat-fee drag vs 0.47pp for hollow ones, and that drag overwhelms whatever pledge premium the reward curve is supposed to add. The incentive mechanism's core assumption — that pledge commitment translates to better delegator outcomes — does not hold in the data

2 findings

OPE.O8

Reserve depletion is a structural clock: every epoch, the pot shrinks, the confiscatory zone widens, and yields erode

Reserve depletion is a structural clock built into the formula. Yield has fallen 5.3% → 2.0% in 413 epochs (R² = 0.99 with reserve), and the trajectory is irreversible without protocol-level intervention.

Concrete projections (from epoch 623, ~April 2026):

~12 months out (~Q2 2027) — yield at ~1.7%.

~20 months out (~Q4 2027) — yield crosses 1.5%.

~42 months out (~Q3 2029) — yield crosses 1.0%.

Each epoch the pot shrinks, the fixed-in-₳ flat fee consumes a growing share of pool rewards, and the retail yield spread compresses toward block-production noise. The failures documented in §4 don't stay still — they degrade every epoch by the same mechanical clock.

The delegator yield has fallen from 5.3% to 2.0% in 5.5 years and the decline is built into the formula. Yield has tracked reserve depletion with

R² = 0.99 across

413 epochs. Projection from epoch 623 (~April 2026):

~1.7% within ~12 months,

sub-1.5% within ~20 months (~Q4 2027),

sub-1.0% within ~42 months (~Q3 2029).

The decline is irreversible without protocol-level intervention — it is built into the monetary expansion formula. The entire yield surface descends as a unit; no pool-level strategy can offset the macro trajectory ·

The confiscatory zone expands upward every epoch — the failures in §4 are not static, they get worse mechanically. As the epoch pot shrinks, the flat fee (fixed at 170/340 ₳) consumes a growing share of pool rewards — the confiscatory zone from

§4.1 — The flat fee (fixed cost) expands upward. The 0.39pp retail yield spread compresses proportionally: at

1.0% base yield (~Q3 2029), the same relative dispersion produces ~0.20pp — indistinguishable from block-production noise. Pools productive today will cross the sub-reliable threshold purely from macro depletion.

The failures documented in §4 are not static — they degrade every epoch 3 findings

OPE.O9

Cardano's yield is no longer competitive — and the case for staking now rests on an ADA appreciation that hasn't materialised

At 2.0%, Cardano's delegation yield sits below the USD risk-free rate (4.3%) and at the bottom of the PoS chains' yield ladder. No other major chain combines this low a yield with liquid, non-custodial, slashing-free design.

The mechanism's design premise was that delegators stake because (i) the yield itself is meaningful and (ii) ADA appreciates in real terms (the formula's monetary design assumes deflation-like behaviour). Both assumptions are now under stress. The yield premise has empirically degraded (OPE.O8); and ADA has not shown the appreciation/deflation behaviour the formula was designed around — the case for delegation now rests almost entirely on a price thesis the protocol cannot guarantee.

If ADA fails to deliver real appreciation, the psychological effect compounds: delegators face low yield AND uncertain price, leaving only conviction-driven holders. The mechanism assumes yield-sensitive delegators; the regime now selects against them.

At 2.0%, Cardano sits below the USD risk-free rate and at the bottom of the PoS landscape. Cardano's current 2.0% delegation yield is below the USD risk-free rate of 4.3% and at the bottom of the PoS chains' yield ladder. No other major chain combines this low a yield with liquid, non-custodial, slashing-free design. The low return is the cost of that design — but the design now asks delegators to accept a yield below the risk-free rate, which only conviction-driven holders will do · The mechanism's premise depends on ADA appreciation that hasn't materialised — and if it doesn't, only conviction-driven holders remain. The reward formula was designed around a monetary regime where ADA itself appreciates (the reserve-depletion design implies deflationary-like behaviour as the supply approaches its cap). In practice, ADA price has not delivered that appreciation, leaving delegators with low yield + uncertain price. The mechanism's assumption — that yield-sensitive delegators allocate based on competitive returns — collapses to a self-selected pool of long-conviction holders, who do not respond to the formula's pricing levers. If the deflation premise fails, the psychological pressure compounds: there is no yield case AND no appreciation case, only a conviction case — which the formula cannot manufacture

2 findings

CEN.O1.F1

Three quarters of registered pools are economically irrelevant. 2,144 of 2,877 (75%) sit below the production threshold (~3M ADA) and together hold only 2.7% of stake

Structural threshold

The structural floorCEN.O1.F2

Three quarters of productive stake sits in 83 named entities. They control 76.7% through 449 productive pools (71 strict multi-pool + 12 attributed single-pool) — and the count is a lower bound (operators using fully separate per-pool infrastructure stay invisible)

Concentration — supply side

SPO supply side — fewer and fewer entities participate in consensusCEN.O1.F3

The pool count flat-lined since epoch 300; the equilibrium is replacement, not growth. The productive set tracks a 700–1,000 historical band (733 at epoch 623) with 1.7% turnover per epoch — 3,497 entries against 3,070 exits balance to near-zero net flow

Market maturity

The market has crystallised — replacement, not growthCEN.O1.F4

Concentration is heavy-tailed: 12 entities run 41% of productive stake. Of the 83 attributed, 12 with 11+ productive pools control 41.0% (8.69B / 21.18B); the top 2 alone (Coinbase 41p, YUTA 25p) hold 13.4%

Scale dominance

The productive operator landscape — 733 pools, 367 entitiesCEN.O1.F5

Custodial dominance sets a structural pledge floor. CEX + IVaaS (10 entities, 181 pools, 7.40B ADA, 34.3% of productive stake) operate at zero pledge by architectural constraint — custodied retail balances cannot legally be pledged

Custodial constraint

The productive operator landscape — 733 pools, 367 entitiesCEN.O1.F6

Independent operators are losing the field — 48% pool-count loss in 323 epochs. Single-pool operators contracted from 555 pools / 39.1% of productive stake (epoch 300 peak) to 291 / 24.4% (epoch 623); the contraction has accelerated in the most recent window

Structural decline

The market has crystallised — replacement, not growthCEN.O1.F7

Multi-pool entities absorbed the contraction and then some — fleet count nearly quadrupled. From 23 entities / 135 pools / 65% of stake (epoch 210) to 85 / 660 / 75.6% (epoch 623); the mid-tier (6–20 pools) tripled in entity count and nearly doubled in stake share

Entity expansion

The market has crystallised — replacement, not growthCEN.O1.F8

The mechanism's designed progression path is invisible in the data. Entry → growth → established is supposed to feed the independent segment; instead the independent population is contracting and the replacement pools that maintain the productive total are entity-operated

Pipeline failure

The market has crystallised — replacement, not growthCEN.O1.F9

On-chain attribution alone misses the bulk of fleet structure — 4 entities vs 85, a ~20× jump. Most multi-pool operators use separate keys per pool, so on-chain ownership clustering catches only the small minority that doesn't separate keys; any analysis stopping at the on-chain layer materially understates MPO concentration

Methodological — attribution layer matters

Behind the pools — entity attribution layers 4 on-chain entities into 85CEN.O2.F1

A single Titan delegator moving in or out can shake a whole pool — whale-funded pools swing ~±20% between epochs vs ±8% for retail. In the 28 custodial-by-delegation pools (typical delegator holds ≥ 100K ₳), stake moves by roughly ±20% between epochs, with 21% of them swinging by more than 50% — these are pools where a single address is large enough that its movement dominates the variance. Retail (809 pools, broad small-delegator base) is mostly stable (±8%) — no single delegator can move the pool. Custodial-by-extraction (79 pools, ≥99% margin) is the most inert (±7%) — stagnation, not active management

Segment-driven variance

A pool's stake stability is segment-drivenCEN.O3.F1

Half the delegator base stakes less than a single transaction fee at peak congestion. Median: 32 ADA. Mean: 16,055 ADA. The 500× gap measures the skewness of a power-law distribution where each tier above 10K ADA holds roughly 20% of total stake despite containing exponentially fewer delegators

Structural inequality

Half the delegator base stakes less than a transaction feeCEN.O3.F2

The delegator population's stake is concentrated in its top 0.07%. 1,000 delegators (0.07% of the 1.36M population) hold 57% of staked ADA; the top 10,000 (0.74%) hold 79.2%. Gini = 0.976 — more concentrated than US wealth (~0.85) and comparable to the most unequal asset distributions observed in financial markets

Concentration — demand side

Half the delegator base stakes less than a transaction feeCEN.O3.F3

Concentration crystallised by epoch 300 and has not moved since. A 9× growth in delegator count has not budged the top-1% share (locked at 78–82%) — new entrants are overwhelmingly micro-delegators (<1K ADA, 96% of new joins) who inflate the denominator without touching the numerator. The economic weight of staking was set in its first ~90 epochs

Structural lock-in

Concentration crystallised by epoch 300 — 9× growth in delegators, no change in the top-1%CEN.O4.F1

Pool-switching collapsed 75% from early Shelley. Redelegations fell from 2,000–3,500 per epoch (early Shelley experimentation) to 600–800 today — three regimes: experimentation (epochs 210–260) → middle period with hard-fork spikes (260–500) → mature settled market (500+)

Market maturity

The certificate stream tells a three-act storyCEN.O4.F2

The base splits cleanly into stickers and switchers, with a thin middle. 42% loyal (201+ epochs, > 2.7 years), 21% volatile (≤ 5 epochs, < 25 days), 37% moderate. The loyal majority anchors pool economics; the volatile tail generates the bulk of the churn signal

Structural bimodality

Most delegators stay put — 42% have held the same pool 2.7+ yearsCEN.O4.F3

Switching is a retail-market phenomenon — custodial and private pools contribute negligible churn. A retail-only filter (margin < 99.9%, excluding by-pledge / by-extraction custodial) produces near-identical aggregates: 40.0% switch rate, 42.4% loyal tenure, ~799 redelegations per epoch

Churn is retail-only

Switching is a retail-only phenomenonCEN.O5.F1

Whales switch 4–5× more often than micro-delegators. Lifetime switches: <1K = 0.67, 1K–10K = 0.95, 10K–100K = 1.64, 100K–1M = 2.65, 1M+ = 3.06. Loyal share (201+ epochs): <1K = 82%, 1M+ = 39%. Switching intensity scales monotonically with stake size — small delegators delegate once and forget; large delegators actively manage their position

Size-driven behaviour

The bigger the delegation, the more it movesCEN.O5.F2

Most of the network's staked capital sits in delegations that move. Whales (1M+) hold 14.1B of the 21.8B staked total (65%), yet only 38% of that stake sits in loyal (201+ epoch) delegations — the rest distributes across moderate and volatile tenures. Pool operators dependent on a few large delegations face structurally higher stake instability than those with a broad base of small loyal delegators

Capital instability

Loyalty and low fees coexistCEN.O6.F1

Delegators cannot see what they're paying for — the yield signal is too flat to act on. Half of all switches (50.5%) produce zero yield change (±5 bps); the median ROS differential is +0.02 bps with an interquartile range of −0.47 to +0.55 bps. The signal is an order of magnitude below any threshold a delegator could observe, let alone optimise against

Price signal invisible

Half of all switches produce zero yield changeCEN.O6.F2

Operator take direction is balanced — no fee-chasing pattern is detectable. 30.8% of switches go to a cheaper pool, 31.5% to a more expensive one, 37.7% land at the same take. The take × ROS matrix's diagonal dominates (lower take → better ROS at 18.4%, similar → similar at 25.6%, higher → worse at 16.5%) — confirming take and ROS are two views of one signal, and that signal is too flat to drive behaviour

No fee-chasing

Operator take direction is balanced — no fee-chasingCEN.O6.F3

Pool size — not price — is the only asymmetric signal in switching behaviour. Moves to smaller pools tend to accept higher take (21.5%), moves to larger pools tend to stay take-neutral (21.0%). The asymmetry suggests moves toward small pools follow non-economic factors (community affinity, retirement at origin, decentralisation preference); moves toward larger pools follow a path of least resistance — visibility, not optimisation

Visibility over optimality

Pool size — not price — is the only asymmetric signalCEN.O6.F4

Loyalty and low fees coexist — the cheapest pools are the stickiest. 92.1% of loyal delegations (201+ epochs) sit in the 0–5% margin range. Loyalty is a consequence of initial pool selection into the competitive neighbourhood, not a barrier to leaving it; fees segment the market at entry, not during tenure

Entry filter, not trigger

Loyalty and low fees coexistCEN.O6.F5

DeFi operates almost entirely outside the staking system. 99.97% of delegations and 99.83% of stake are key-based; script-based delegation (smart contracts, multisig, governance) is 399 addresses and 38M ADA. The DeFi ecosystem has not integrated with delegation in any meaningful way — and the credential type cannot separate custodial from retail capital, since both present as key-based

No smart-contract staking

DeFi operates almost entirely outside the staking systemCEN.O7.F1

The staking rate is structurally declining despite persistent net delegator inflows. The rate has fallen from 71% (epoch ~260) to 59% (epoch 623) — a 12 pp loss over ~360 epochs. Circulating ADA grew from ~32B to ~37B while staked ADA grew from ~23B to only ~22B; the non-participant pool is growing faster than the staking pool.

Supply-side erosion

CEN.O7.F2

14.36B ADA (39.8% of circulating supply) does not participate in staking — and only a sliver of that is reachable by reward design. The non-participant pool has been stable at 36–39% for over 300 epochs. Only 0.37% of circulation (134.6M ADA, 24,176 accounts) is nominally addressable by an incentive-design change — and even that figure shrinks under scrutiny (§5.5). The remaining 39.4% sits in addresses that cannot delegate without a protocol-level change.

Structural non-participation

2/5 of the supply has sat unstaked for over 300 epochsCEN.O7.F3

The non-participant floor is structural, not behavioural — incentive changes alone cannot reach 99% of it. Reward-mechanism changes (curve adjustments, fee-structure reforms) can at most shift the 0.37% addressable pool. Moving the other 39.4% requires protocol-level changes — enabling exchange-style addresses to stake, mandating staking-capable DeFi script standards, or introducing delegation-by-default for newly minted wallets.

Structural protocol limit

Most non-participants have no staking keyCEN.O7.F4

The "no staking key" residual is dominated by legacy and custody, not by active DeFi. Among the 2.45B identified by address shape, exchange-style addresses (1.04B) and pre-staking-era legacy addresses (1.32B) together account for 96%. DeFi contract addresses without staking total just 91M — one tenth as much, growing only slowly. The remaining ~11.8B sits in standard wallets where the holder never bothered to register a staking key. The unreachable mass is overwhelmingly inertia, not active opt-out.

Composition — legacy not DeFi

Most non-participants have no staking keyCEN.O7.F5

The no-staking-key pool is bimodal: 37% is pre-staking-era dormant, 44% is from the last 73 epochs — the middle is empty. The dormant fraction (928M) erodes at about 0.8M ADA per epoch as wallets occasionally awaken. The recent fraction (1,110M from epochs 550–623) reflects active exchange and DeFi cycling. The middle eras are essentially spent — the population splits cleanly into probably lost and operationally active, with very little in between.

Bimodal — dormant vs operationally active

The locked share splits cleanly between probably-lost and operationally-activeCEN.O7.F6

The structurally-excluded 2.5B is held by a few hundred wallets, not by a diffuse retail base. Top-3 wallets control 19.1%, top-10 control 41.6%, top-200 control 68.9% of the 2.5B residual. The top of the distribution splits into recognisable archetypes — exchange hot wallets, institutional cold storage, pre-staking-era legacy holders — addresses that can be named, not anonymous retail. Any policy aimed at this pool acts on a small, identifiable counterparty list.

Concentration of structurally-excluded ADA

A few hundred custodians hold three-quarters of the structurally-excluded ADACEN.O7.F7

DeFi-locked-without-staking is a one-contract problem, not an ecosystem problem. 89% of the 91M residual lives in one 80M-ADA contract; the remaining 99 contracts together hold ~10M (11%). Mandating staking-capable contract addresses in DeFi standards would primarily move that one contract — the rest of DeFi has either already integrated staking or holds amounts too small to materially shift the residual.

DeFi exclusion is a one-contract problem

The DeFi-locked share is one contractCEN.O7.F8

The "addressable" pool is mostly inert — the real ceiling for reward-driven recruitment is 0.06% of circulation, not 0.37%. Of the 24,176 nominally-addressable accounts, 91% hold zero ADA, 89% have been dormant since the first 41 epochs of Shelley, and 80% of the residual ADA sits in one DeFi vault. The genuine ceiling for reward-driven re-engagement is ~22.5M ADA (0.06% of circulation), spread across ~2,100 active accounts. The reward mechanism's recruitment ceiling is narrower than the headline 0.37% suggests by an order of magnitude.

Real ceiling on reward-driven recruitment

The "addressable" pool collapses to about 2,100 active accountsCEN.O8.F1

The submitter population peaked at 790K addresses and has since contracted by 96% — the chain runs busily, with a much smaller crowd. The population grew in step with transaction count through early Shelley, peaking at 790,335 unique addresses and 1,566,974 transactions at epoch 304 (the CNFT minting frenzy). From epoch 310 onward the population collapsed faster than volume: 101K submitters at epoch 384, 58K at epoch 500, 31,176 at epoch 627. Transaction volume fell only 92% over the same window — a population one twenty-fifth of its peak still sustains three quarters of the per-epoch transaction rate seen during 2023–2024.

Population contraction

A shrinking crowd paying for a busy chainCEN.O8.F2

Breadth is collapsing while per-actor intensity is rising — the same shrinking core just transacts more often. The address-to-transaction ratio fell from 0.88 (epoch 210) to 0.26 (epoch 627), and tx-per-submitter rose from ~2.0 (epoch 304) to ~3.8 (epoch 627). Cumulative Shelley-era throughput totals 118.07M transactions and 37.85M ADA in fees. The growth-trajectory signal is unambiguous: new addresses are not entering the fee-paying population at a rate that would sustain breadth — the same shrinking core is just transacting more often.

Same shrinking core, more active per-member

A shrinking crowd paying for a busy chainCEN.O9.F1

By address count, the submitter population remains overwhelmingly stakeable — but the script segment has grown structurally. At epoch 627: 73.3% base-key (addr1q) addresses carrying a stake credential, 10.8% base-script (addr1z), 9.2% enterprise-key (addr1v), 4.9% legacy Byron, 1.6% enterprise-script (addr1w), 0.2% base-other. Compared to the earlier snapshot at epoch 384 (87% base-key, <1% script), the shift is clear — base-key dropped 14 pp while base-script grew from 0.4% to 10.8%. The count-based picture remains misleading: the small script population punches far above its weight in fee terms.

Headcount remains overwhelmingly stakeable