Where stake concentrates across the pool population — Reward Flow stage 2

Through epoch 623 · 2026/04/09Nicolas Henin · 2026/06/18

This report analyses the second stage of Cardano's reward pipeline — the pool-level reward distribution — and traces a single diagnostic thread from mechanism to actors to consequences. It builds on the empirical baseline established in the Analysis of Cardano's Incentive Mechanism (Lopez de Lara, 2025; hereafter the Incentive Mechanism Analysis).

Every epoch, the pools pot (~15.5M ADA at epoch 616) enters this stage. The reward curve allocates it across pools based on stake, pledge, and block performance. What is not distributed returns to the reserve. At epoch 616, only 43.7% of the pools pot reached operators and delegators. This report asks why, and follows the answer where it leads.

The companion Treasury & Pool Pots Distribution covers the upstream stage that assembles the pot; the companion The Operator's Cut covers the downstream stage that splits each pool's allocation between operator and delegators.

Participation gap and unused pledge-incentive budget return 54% of the pool pot to reserve. Of the 15.53M ADA/epoch budget, only 6.79M (44%) reaches operators and delegators. The participation gap (unstaked ADA) accounts for 31.6% — outside the formula's control, upstream of this stage. The unused pledge-incentive budget accounts for 22.1%, with 95.6% of the bonus allocation wasted — the single largest addressable inefficiency in the system. All other causes — pledge-not-met confiscation (2.1%), missed blocks (0.5%), oversaturation (0.3%) — are an order of magnitude smaller.

Pledge is unused at scale and structurally unfair across pool sizes.78% of staked ADA sits in pools with pledge ratio < 1%; the stake-weighted median is 0.07% — the bonus is silent for almost every operator.

The unfairness is algebraic, not just empirical. The activation function $A(\nu, \pi) = \nu^2 \cdot \pi[1 - \pi(1-\nu)]$ has three structural defects: a permanent quadratic size penalty $\nu^2$ at every pledge ratio, a non-monotone regime in π for any pool below half-saturation (pledging more pays less), and a cubic collapse to $\nu^3$ at full self-pledge. The strongest commitment signal is paid the worst-case scaling on size — and the entire mainnet population sits in the regime where increasing pledge can reduce the bonus.

Empirical consequence: pledge yield tops out at 0.68%/yr at saturation, well below the 2.3%/yr delegators earn passively, and 3.4M ADA per epoch (22% of the pot) reserved for the bonus returns to reserve unclaimed. The pledge mechanism, designed as Cardano's primary Sybil-resistance tool, has never activated.

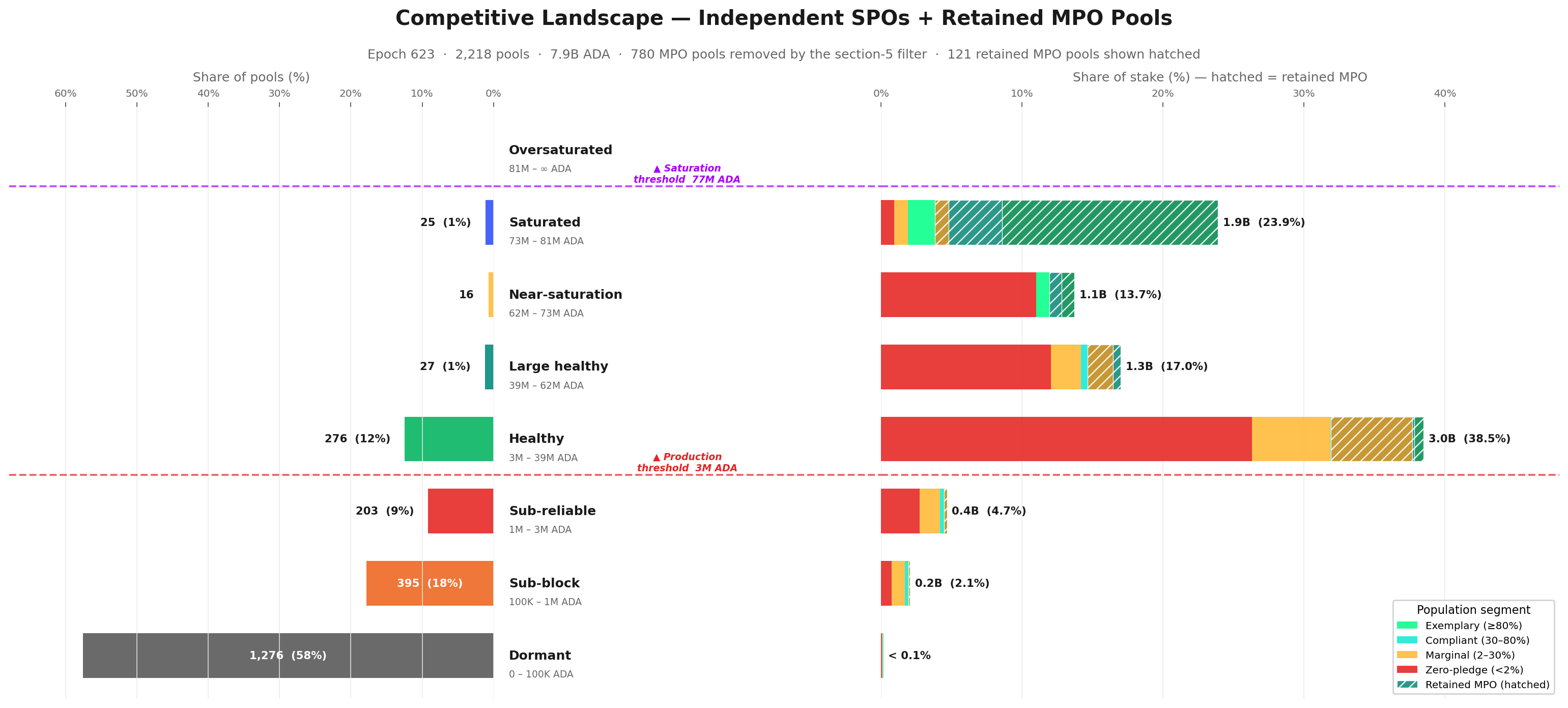

Two structural thresholds shape pool space. The production threshold (~3M ADA at today's active stake) is the stake level at which a pool produces ≥1 block per epoch with 95% probability (λ=3 in the Poisson process) — a physics boundary, emergent from slot-leadership, not a parameter. The saturation cap (77M ADA = $z_0 = 1/k$) is the formula ceiling that limits any single pool's share of network reward. Operator-viability — the stake level at which the operator can pay themselves enough to cover real costs — is a separate, volatile concept that tracks the ADA/USD price and the operator's fee-structure choices; at today's prices it coincides with the production threshold (the pool generates ~5.5× the operator's cost), so we treat viability as orders of magnitude only in §4.1.2.2 — Viability threshold (orders of magnitude only) and do not draw it as a separate line elsewhere.

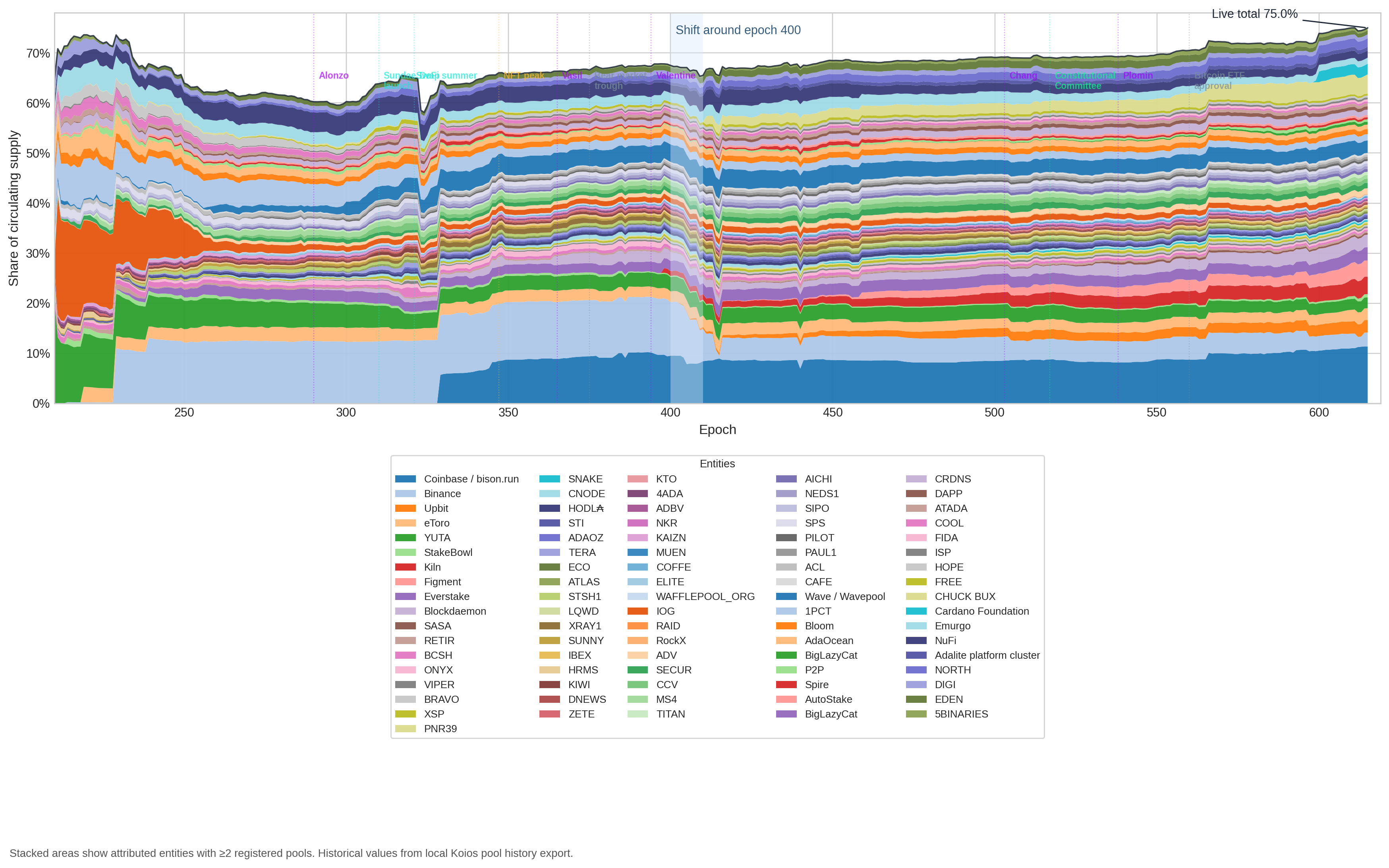

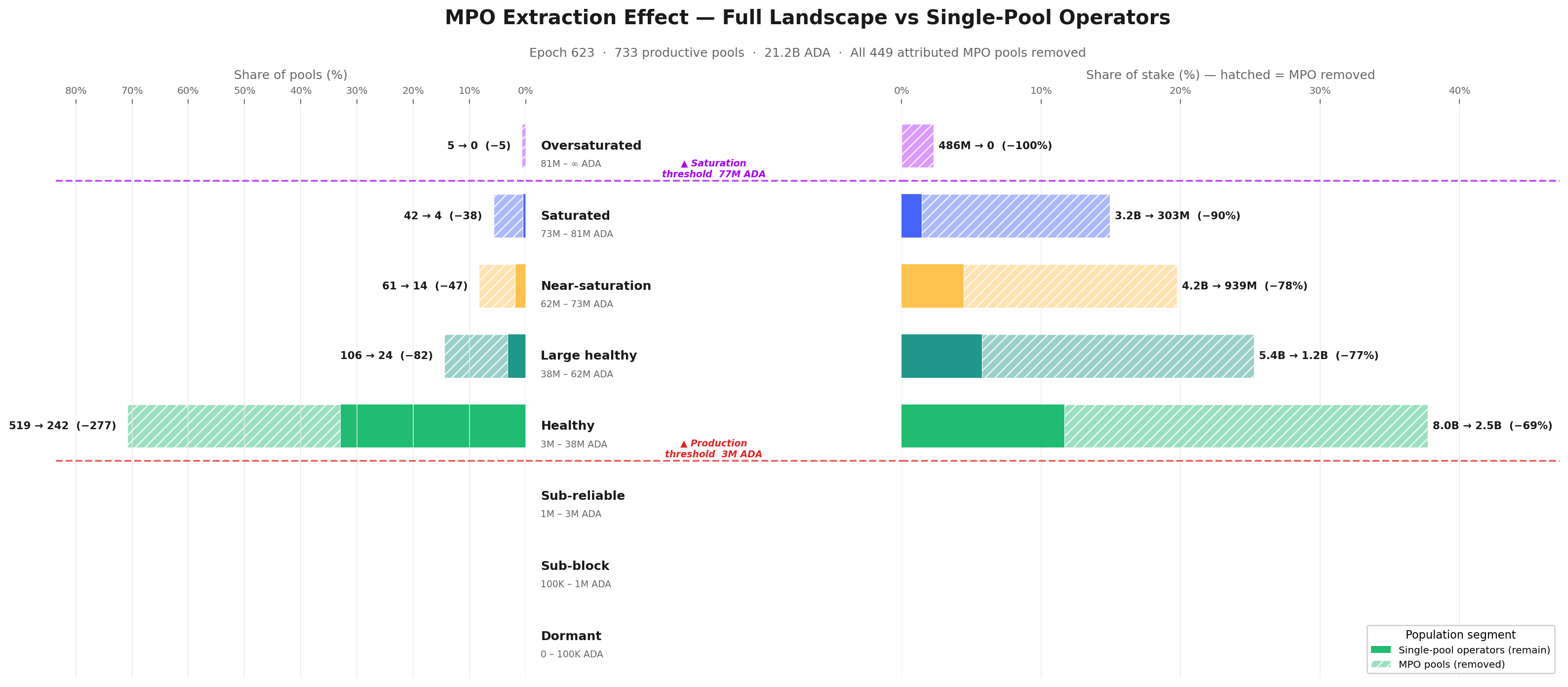

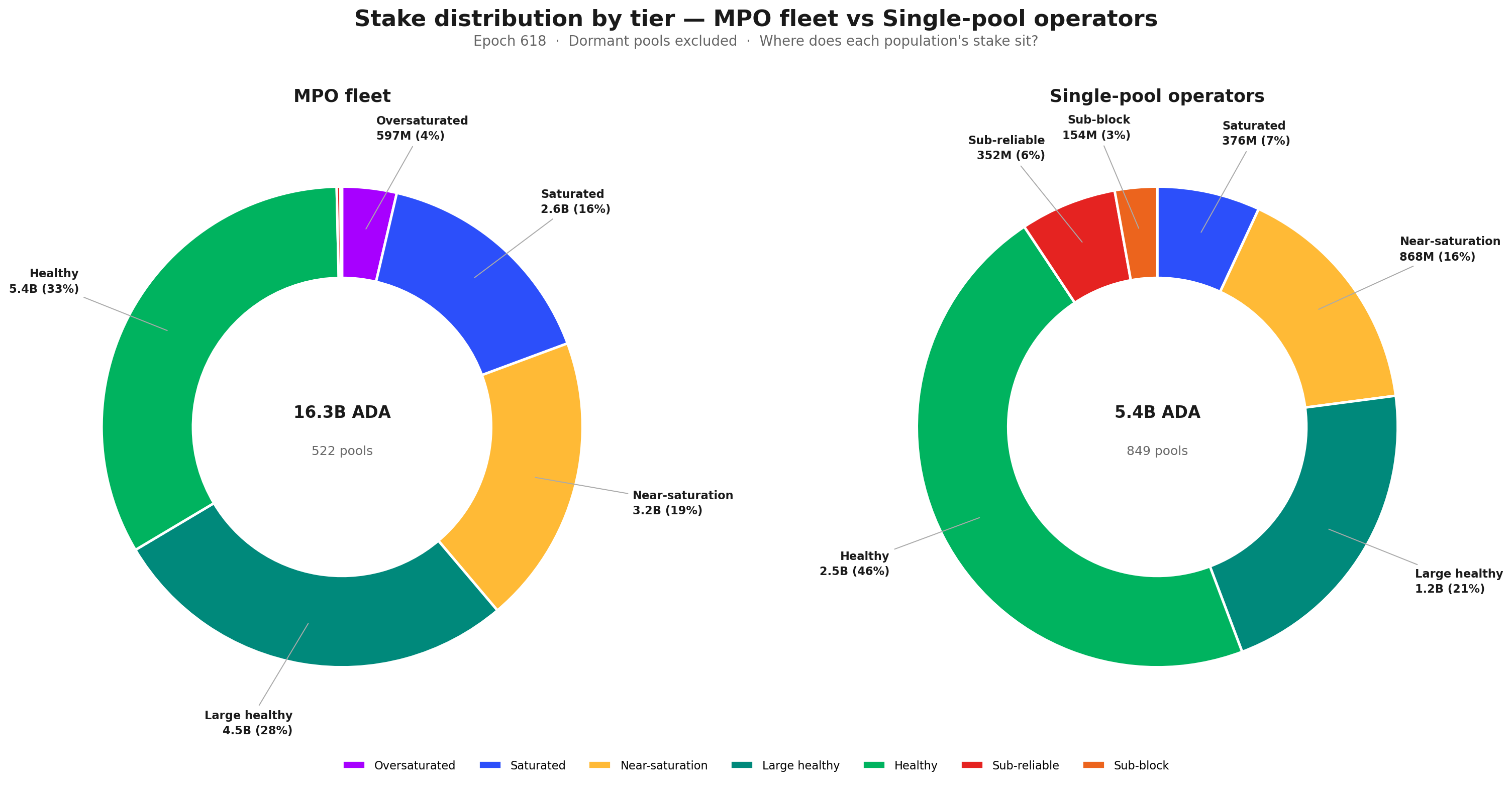

The pool distribution is sharply asymmetric.1,987 pools (73%) sit below the viability line, holding only 2.7% of active stake and destroying value for their delegators. Conversely, 27% of pools (Healthy and above) hold 96.6% of all staked ADA — the inversion of headline pool count vs. stake share is the defining structural feature of the landscape.

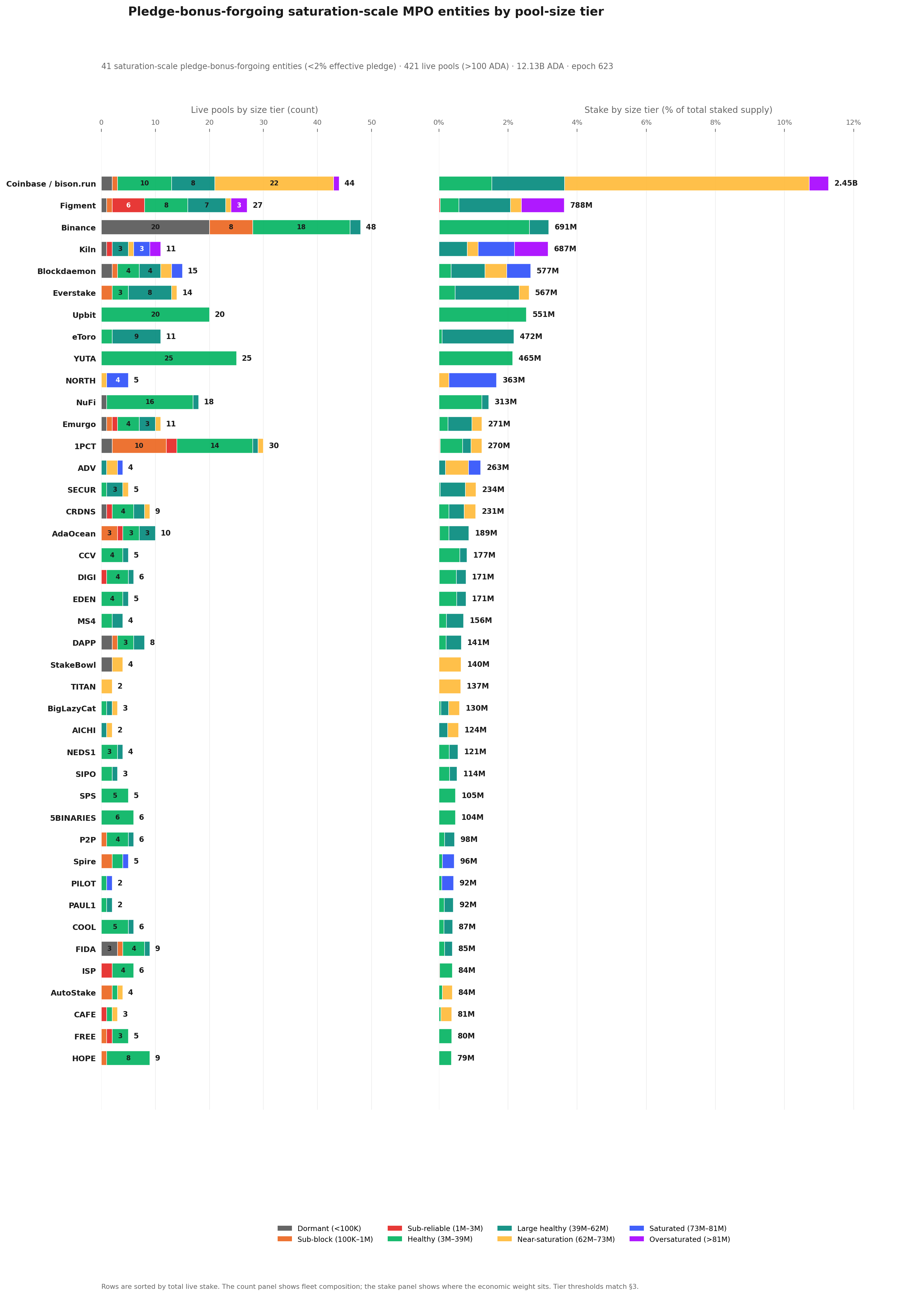

But pools live under two pressures, not one. Per-pool economics is only half the story: each pool appears as an independent on-chain entry, yet multi-pool entities can run sub-reliable pools as part of fleet strategy and split aggregate stake across many pools. The upper-tail concentration is structurally invisible at the pool level — entity attribution (POL.O5) reveals that 76.7% of productive stake is held by 83 MPO entities.

The boundaries are dynamic — they shift with active stake, fixed costs, and $k$ — so any CIP must be evaluated against where they move, not against a snapshot.

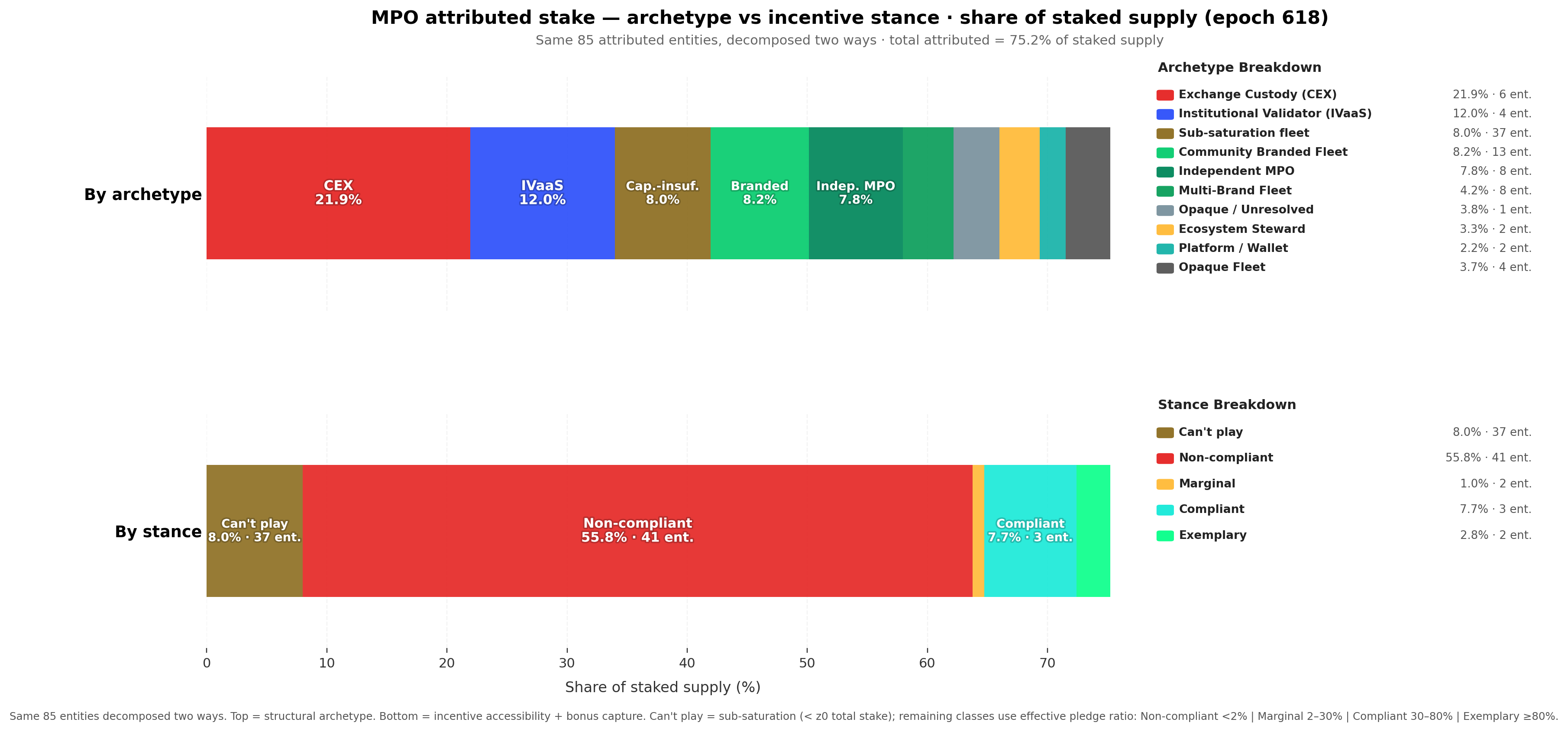

83 multi-pool operators control 76.7% of productive stake. They operate 449 productive pools (≥3M ADA at epoch 623, the production threshold) holding 16.24B ADA. Of those, 48 are saturation-scale to play the pledge game, 35 are not — and 42 of the 48 saturation-scale MPOs are zero-pledge, forfeiting ~550K ADA/epoch in pledge bonus rather than pledge. CEX + IVaaS alone hold 7.39B ADA (34.9% of productive stake) at structurally zero pledge: custodial operators cannot pledge capital they do not own. Two exemplary MPOs capture the entire bonus among pledgers — and one of them (Cardano Foundation) pledges by mandate, so the mechanism's output rests on a single private entity.

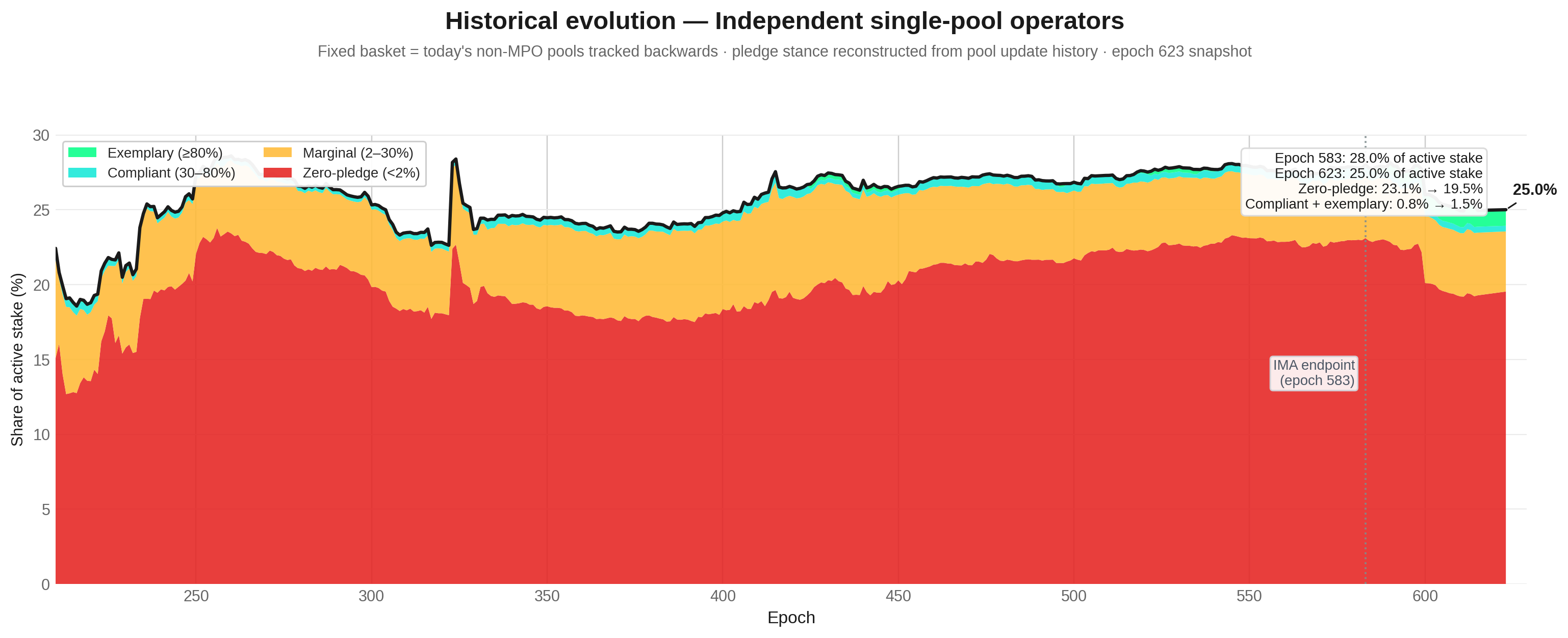

The single-pool operator base is far smaller and weaker than it appears. The Incentive Mechanism Analysis's headline of 741 healthy pools collapses to 284 single-pool operators once MPO fleet members are removed — 61% of the headline were fleet pools, the competitive field is 3× smaller than it appears. 80.6% of single-pool productive stake is zero-pledge: pledge is correctly priced as irrelevant at their scale. Only 51 marginal single-pool operators (13.9% of single-pool productive stake) partially pledge, sitting at the decision boundary that any policy reform must target. The segment's share of active stake fell from 28.0% → 25.0% since epoch 583 — slow structural decline.

The incentive-responsive field is a fraction of the network. Once non-responsive entities are stripped out, the arena that demonstrably reacts to the pledge signal holds 7.89B ADA — only 36% of active stake. 77 of 83 MPO entities (13.89B ADA, 65.6% of productive stake) are outside the pledge-response path through three distinct mechanisms: CEX cannot pledge custodied funds, IVaaS cannot pledge client assets, and community fleets choose not to. The reward sharing scheme was designed for a world of single-pool operators competing on pledge commitment; the world that exists is a multi-game environment dominated by entities operating outside the mechanism's reach.

The remainder of the report walks the diagnostic in four steps: the initial design presents the SL-D1 reward formula in three layers (original notation → normalized saturation coordinates → mainnet parameterization); distribution efficiency decomposes the 56% pot loss; the pool landscape dissects the populations by tier, by entity, and by the independent base; and the synthesis at the end of §4 reassembles the layers. All counts and amounts use the latest available pool snapshot (epoch 618) and the latest complete epoch with reward data (epoch 616) unless stated otherwise.

Table of Contents

1. Mainnet Observations

POL.O1

Observation 01 · 4 findings

Participation gap and unused pledge-incentive budget return 54% of the pool pot to reserve

4 findings

Only 6.79M of 15.53M ADA/epoch reaches operators and delegators — a 44% distribution efficiency.

Two causes dominate the loss: the participation gap (unstaked ADA) returns 4.91M ADA/epoch — 31.6% of the pot, upstream — outside formula control; the unused pledge-incentive budget returns 3.43M ADA/epoch — 22.1% of the pot, 95.6% of the bonus allocation wasted.

All other causes are an order of magnitude smaller — pledge-not-met confiscation (2.1%), performance (0.5%), oversaturation (0.3%).

Less than half the pool pot reaches its targets. Only 6.79M of the 15.53M ADA per epoch budgeted for distribution actually reaches operators and delegators — a 44% distribution efficiency. The other 56% returns to the reserve unused

ADA that isn't staked at all is the single largest source of waste. Every epoch, 4.91M ADA is forfeited because roughly a third of the supply sits unstaked — that's 31.6% of the pot, returned to the reserve before the formula even gets a chance to distribute it

Almost all of the pledge-bonus budget is wasted. Every epoch, 3.43M ADA earmarked as the pledge bonus returns unclaimed — 22.1% of the pot and 95.6% of the bonus allocation. Unlike the participation gap, this loss is entirely within the formula's control

Two causes account for almost all the waste; everything else is rounding error. The participation gap and the unused pledge-incentive budget together return 53.7% of the pot to reserve. The remaining sources combined — pledge-not-met confiscation (2.1%), missed blocks (0.5%), oversaturation (0.3%) — add up to less than 3% of the pot

The reform priority is clear

POL.O2

Observation 02 · 6 findings

Pledge is unused at scale and structurally unfair across pool sizes

6 findings

78% of staked ADA sits in pools with pledge ratio < 1%; the stake-weighted median is 0.07%. The bonus that should reward commitment is silent for almost every operator.

The unfairness is algebraic, not just empirical. The activation function $A(\nu, \pi) = \nu^2 \cdot \pi[1 - \pi(1 - \nu)]$ has three structural defects: a permanent quadratic size penalty $\nu^2$ that scales every pledge ratio against pool size; a non-monotone regime in π for any pool below half-saturation, where pledging more than $\pi^* = 1/[2(1-\nu)]$ pays less; and a cubic collapse to $\nu^3$ at full self-pledge, where the strongest possible commitment is paid the worst-case scaling on size.

The combined consequence: yield on pledge capital tops out at 0.68%/yr at saturation (vs. 2.3%/yr passive delegation), and 3.4M ADA/epoch (22% of pot) reserved for the bonus returns to reserve unclaimed.

Almost no operator pledges meaningfully.78% of staked ADA sits in pools where the operator pledges less than 1% of the stake they manage; the stake-weighted median pledge ratio is 0.07%

Empirical — pledge is absent where stake concentrates

Pledging earns less than passive delegation, even at maximum scale. A fully-saturated pool whose operator pledges the entire saturation amount earns just 0.68%/yr on that pledged capital — below the 2.3%/yr anyone can earn by passively delegating

The pledge bonus budget goes unused.3.4M ADA every epoch — 22% of the pool pot — is reserved for the pledge bonus, but the formula's distribution mechanics return almost all of it to the reserve unclaimed

Small pools cannot earn meaningful pledge bonus, no matter how committed the operator. The formula scales the bonus by pool-size squared ($\nu^2$) before pledge is priced — at every pledge ratio. A pool at 10% of saturation is structurally capped at 1% of the bonus a saturated pool earns, regardless of operator commitment

Pledging more pays less past a sweet spot — for almost every pool on mainnet. For any pool below half-saturation, the bonus peaks at an interior pledge ratio $\pi^{*} = 1/[2(1-\nu)] < 1$, and pledging beyond that point reduces the bonus. At $\nu = 0.3$ the peak sits near 71% pledge ratio, and full self-pledge pays 16% less than the peak. The formula formally rewards operators for under-committing

The strongest possible commitment signal is paid the worst-case reward. When the operator pledges 100% of their own pool ($\pi = 1$), the bonus collapses to pool-size cubed ($\nu^3$). A half-saturated pool earns 12.5% of the maximum bonus; a pool at 10% of saturation earns just 0.1%

Algebraic — pre-empirical

POL.O3

Observation 03 · 5 findings

Three structural thresholds shape pool space: production (physics), viability (economics), saturation (formula)

5 findings

Three thresholds emerge from the protocol's own mechanics and partition the pool population. Each has a different nature and a different mutability profile.

Production threshold (~3M ADA) — physics, emergent. The stake at which a pool produces ≥1 block per epoch with 95% probability (λ=3 in the Poisson process — blocks are produced reliably enough for yield to be a usable signal for delegators). Not a protocol parameter; rises with active stake (to ~5.35M at full supply). The 1-block-expectation point (~1M ADA) is a special case at the bottom edge of this regime — below it, pools produce less than one block in expectation per epoch.

Viability threshold — economic, and it moves; sits structurally above the production threshold. The protocol's minPoolCost floor (currently 170 ADA, halved from 340 at epoch 445 / 2023-10-27; most pools still set 340) gives a nominal break-even at ~1.1M ADA — but this is just the formula's internal floor. Real economic viability requires covering infrastructure (~\$1,320–3,240/yr for block-producer + 2 relays + monitoring) plus operator labour at market DevOps/SRE rates (~\$5,160/yr minimum at 10 hrs/mo × \$43/hr) — totalling ~\$7,160/yr minimum, easily doubling for a more demanding setup. Because operator costs are fiat-denominated while revenue is in ADA, the real target tracks the ADA/USD price (~28,600 ADA/yr at \$0.25; ~71,600 at \$0.10). At today's prices no single-pool tier comfortably clears it; competitive compensation begins only at the 2-pool MPO tier.

Saturation cap (77M ADA = $z_0 = 1/k$) — formula, fixed by parameter. The reward ceiling per pool, designed to limit any single pool's share of network reward.

The cleaner future state would collapse viability into production, leaving only the physics-grounded boundary. This is harder than it sounds — zeroing minPoolCost removes the protocol-imposed floor, but the real labour-cost floor remains unless a structural mechanism (e.g., Rocket-Pool-style shared operations) is introduced. See §1.2.4.4.1 Enforce the production threshold.

The boundaries are dynamic — they shift with active stake, fixed costs, $k$, and the ADA/USD price — so any CIP must be evaluated against where they move, not against a snapshot.

The production threshold is physics-based — emergent from slot-leadership, not a parameter. At today's active stake (~21.18B ADA), regular block production starts at ~3M ADA, the stake level at which a pool has a 95% probability of producing at least one block per epoch (λ=3 in the Poisson process) — the point where yield is usable as a delegator signal. The 1-block-expectation point (~0.97M ADA) is a special case at the bottom of the regime: below it, pools have less than one expected block per epoch and rewards are noise, not signal. The threshold rises with active stake — at full supply (~38.5B ADA), the 3-block point climbs to ~5.35M ADA, pushing more pools below it

Operator-viability is volatile and tracks the ADA/USD price; at today's prices it coincides with the production threshold, but separates upward when ADA falls. A single-pool operator needs to extract roughly 390 ADA/epoch today (~\$7,160/yr cost floor — infrastructure ~\$1,320–3,240/yr + DevOps labour ~\$5,160/yr min — at \$0.25 ADA). At the production threshold (~3M ADA stake), the pool generates ~2,145 ADA/epoch on average, more than enough — viability and production coincide. At lower ADA prices the cost in ADA rises, and the reliable-income floor rises above production. The threshold is therefore not drawn as a fixed line in the rest of this document; it is treated as a separate volatile concept whose stability is a question for the V2 spec, not the diagnostic

The saturation cap is a formula ceiling — $z_0 = 1/k$. At $k = 500$, $z_0 = $ 77M ADA. Beyond it, the per-pool reward stops scaling with stake. The cap exists to limit any single pool's share of the network's reward — a per-pool anti-Sybil device, fixed by parameter

The cleaner future state collapses viability into production. Zeroing minPoolCost (or making it scale with the reward curve) removes the protocol-imposed floor, but the real labour-cost floor remains and viability stays above production unless a structural mechanism is introduced — e.g., a Rocket-Pool-style shared-operations path that lets sub-scale stake fund a single operator. The §1.2.4.4.1 Enforce the production threshold proposal pairs both: a minPoolCost reform AND a sub-threshold path for stake that cannot reach the production line on its own

Tier boundaries are dynamic — they shift with active stake, fixed costs, and $k$. When a CIP proposes $k = 1000$, the saturation threshold halves to ~38.5M and every "Large healthy" pool reclassifies as near-saturation. When active stake grows from 21B to 35B ADA, production and viability lines rise proportionally. The taxonomy is a framework for reasoning across scenarios, not a snapshot of today's values — reform evaluation must track where the boundaries move

Framework — not a snapshot

POL.O4

Observation 04 · 3 findings

A 73% sub-block tail (useless to consensus) and a 27% productive segment (unreadable without entity-level investigation)

3 findings

The pool population splits cleanly at the production threshold, and the two segments answer different questions.

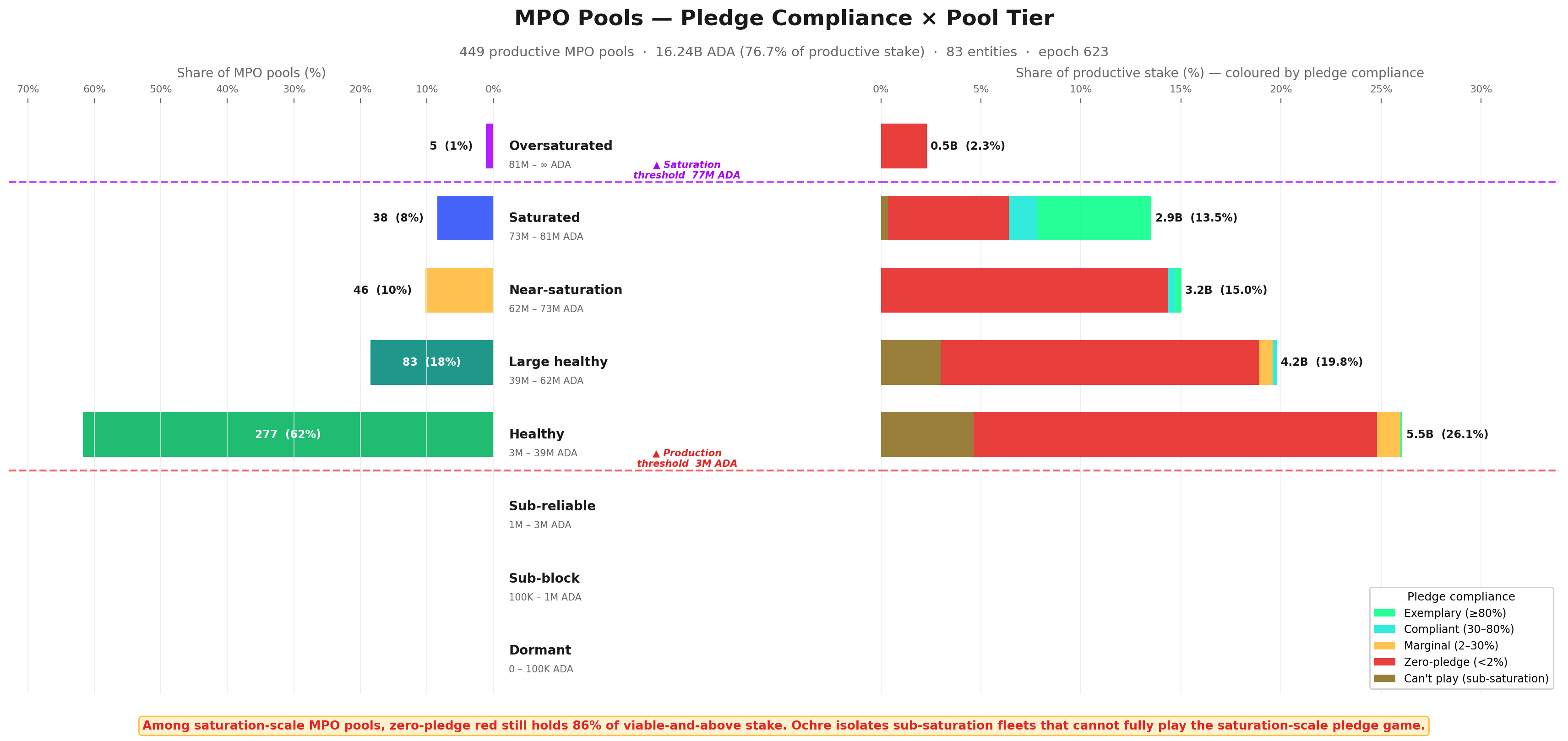

Below the production threshold (~3M ADA): a sub-block tail invisible to consensus.1,987 pools (73% of all pools with stake) sit below the 95%-block-probability bar and produce blocks too sporadically to be useful for the consensus protocol — they hold only 2.7% of active stake and exist as ghost capacity the protocol admits but cannot reliably activate. Below this threshold, a delegator cannot read a meaningful yield signal from any single pool — Poisson noise dominates the mean.

Above the production threshold: the productive segment cannot be read pool-by-pool.731 pools (27%) hold 96.6% of staked ADA and carry the network's actual block production. But each pool appears on-chain as if it were independent, while in fact multi-pool entities run fleets — pool count is therefore a poor proxy for operator count, and pool-level metrics conceal entity-level concentration. The entity-level breakdown — counts, archetypes, who responds to the pledge signal — is the subject of POL.O5 — entity-level analysis.

1,987 pools (73%) sit below the production threshold (~3M ADA) and produce blocks too sporadically to carry consensus reliably. At the production threshold a pool has a 95% probability of producing ≥1 block per epoch (λ=3); below it Poisson noise dominates and yield is statistical noise. Collectively these pools hold only 2.7% of active stake — ghost capacity the protocol admits but cannot reliably activate; neither delegators nor the consensus layer can read a meaningful signal from any single pool in this segment

The productive segment (731 pools, 27%) holds 96.6% of staked ADA — the actual consensus-carrying population. This is the segment any reform of $k$, the pledge curve, or the saturation cap actually moves. Pool count is not stake share: the inversion of headline pool count vs. stake share is the defining structural feature of the landscape

The productive segment cannot be read pool-by-pool — it must be read at the entity level. Many of the 731 productive pools are operated as fleets by a smaller set of entities; pool-by-pool analysis of the upper tail conceals the actual concentration and over-counts independent actors. The pool view tells us how much stake is productive; only the entity view tells us who controls that stake and who responds to the pledge signal. The entity-level breakdown — counts, archetypes, pledge stances — is the subject of POL.O5 — entity-level analysis

Methodological — entity lens required

POL.O5

Observation 05 · 7 findings

83 multi-pool operators control 76.7% of productive stake — and almost none of them pledge

7 findings

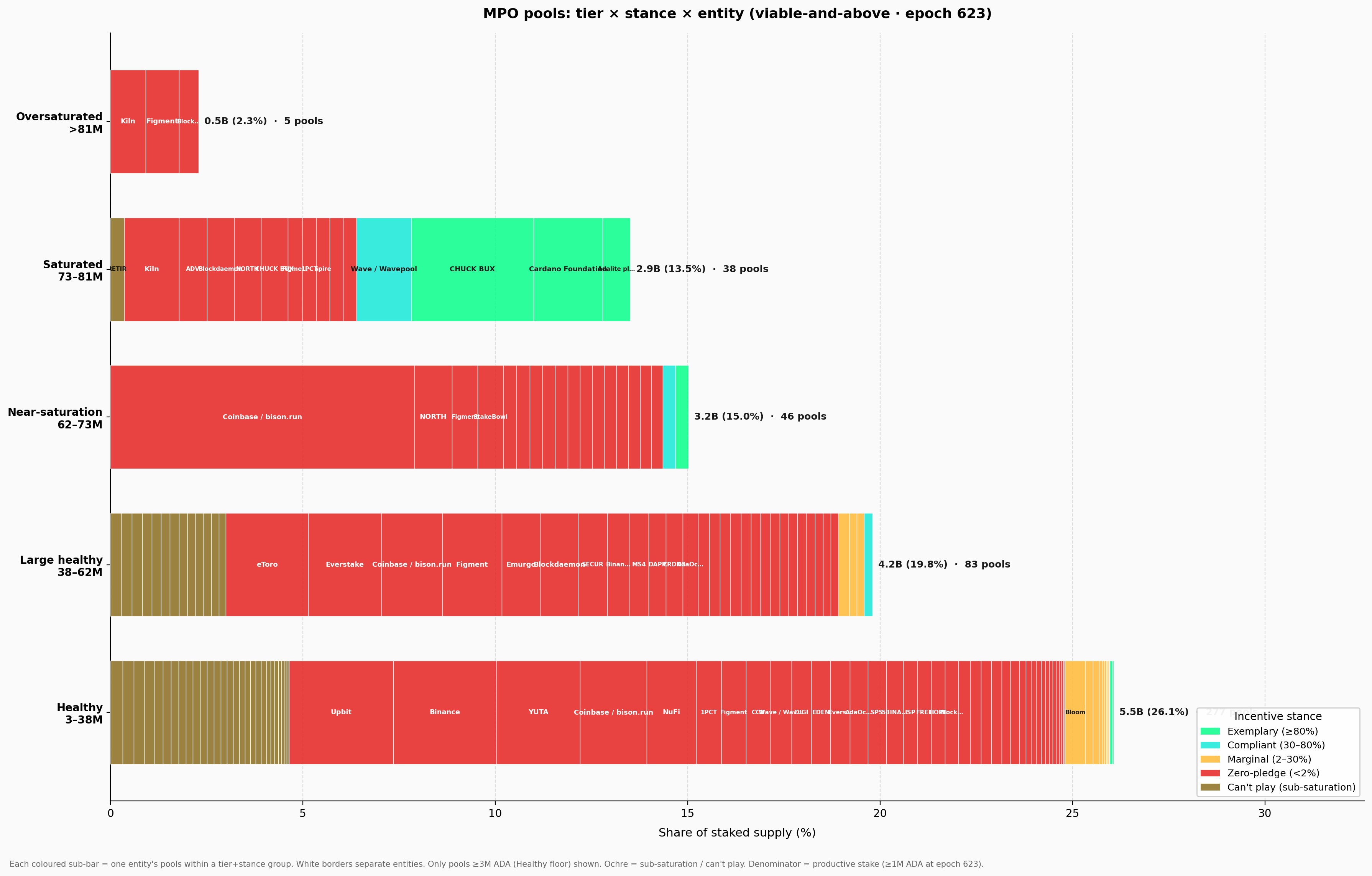

83 attributed entities operate 449 productive pools holding 16.24B ADA — 76.7% of productive stake.

The pledge picture is stark: of the 48 entities with enough capital to ever fill a pool to saturation, 42 sit at zero-pledge (pledge ratio < 2%), holding 12.20B ADA combined.

Architecture explains part of it: 10 of those 42 (CEX + IVaaS — Coinbase, Binance, Figment, Kiln…) hold 7.39B ADA they legally cannot pledge — exchanges custody retail balances, institutional validators run client assets. But that is only half the story. The other 32 are sovereign saturation-scale MPOs holding 4.80B ADA (22.7% of productive stake) that could pledge meaningfully but choose not to — they forfeit ~556K ADA/epoch in pledge bonus and absorb the cost. The architectural barrier is real; the strategic abandonment is larger as a share of the entities that could play. Only 2 of the 48 MPOs actually pledge most of their stake (≥80% pledge ratio) — Cardano Foundation (which pledges out of institutional duty, not in response to the formula) and Adalite Platform. Among private operators making an economic decision, the pledge mechanism currently succeeds on exactly one entity (Adalite).

Three quarters of the network's productive stake sits in 83 named entities. They operate 449 productive pools (≥3M ADA at epoch 623, the production threshold) holding 16.24B ADA — 76.7% of productive stake. 71 are strict multi-pool fleets; 12 are single-pool operators attributed by ticker, metadata, or relay clustering. The remaining 23.3% (4.94B ADA across 284 pools) sits in unattributed single-pool operators — attribution is a lower bound

48 MPO entities concentrate 14.55B ADA — 68.7% of productive stake — in operators each big enough to fill a saturation cap. These are the saturation-scale MPOs (aggregate stake ≥ $z_0 \approx 77\text{M ADA}$). Concentration at the entity tier is sharper than the 76.7% headline once the 35 sub-saturation entities (1.69B ADA, multi-pool by form but single-pool-like in economics) are stripped out. The top 5 of the 48 alone hold 5.44B ADA — 25.7% of productive stake (Coinbase, CHUCK BUX, Figment, Binance, Kiln); the top 10 hold 39.1%. The split is purely structural — pledge is taken up next

Entity-tier concentration — 68.7% of productive in 48 actors

Among the 48 saturation-scale MPOs, 42 are zero-pledge. They sit below the 2% pledge ratio bar and forfeit ~556K ADA/epoch (~40.6M/year) in pledge bonus rather than lock capital that would qualify for it. The responsive middle is tiny: 1 marginal, 3 compliant, 2 exemplary. The pledge gap is universal among saturation-scale MPOs; the bonus penalty (~11–21% of maximum reward for the largest offenders) is a modest tax on operators of multi-million-ADA fleets — not a deterrent

Architecture explains 10 of those 42 — exchanges and institutional validators legally cannot pledge. CEX (6 entities, 119 productive pools) + IVaaS (4 entities, 54 productive pools) hold 7.39B ADA — 34.9% of productive stake — at architecturally zero pledge. Exchanges custody retail balances; institutional validators run client assets they do not own. Pledging this capital is precluded by the legal/business model, not chosen — no parameter change moves this stake into the pledge game

The remaining 32 sovereign MPOs choose not to pledge — they hold 4.80B ADA (22.7% of productive stake) that could enter the pledge game but doesn't. After excluding the 10 architecturally-barred CEX+IVaaS entities, 32 saturation-scale MPOs remain in the zero-pledge bucket — community-branded fleets, independent multi-pool operators, multi-brand fleets, opaque fleets, ecosystem stewards. They have no architectural barrier; they could lock capital and capture the pledge bonus. They don't. This is strategic abandonment, not custodial constraint — and it is the share of the MPO landscape any incentive reform must actually address

The mechanism's exemplary signal rests on one private entity. Only two MPO entities clear the ≥80% pledge bar at epoch 623 — Cardano Foundation (99.1%) and Adalite Platform (93.0%). CF pledges by institutional mandate, not economic incentive; remove it and the exemplary band collapses to a single private actor. A Sybil-resistance tool designed for 500 pools is, in practice, a transfer programme for one private entity

Zero-pledge dominates every viable tier — no single-tier reform reaches it. Among saturation-scale MPO productive pools, 85.5% of stake (12.44B of 14.55B ADA) sits in zero-pledge pools, and that stake spreads across Healthy, Large healthy, Near-saturation, and Saturated/Oversaturated. A reform targeting one tier leaves the others untouched and propagates secondary effects everywhere; any change reshapes the whole landscape, not just the segment it targets

Reform constraint

POL.O6

Observation 06 · 4 findings

Only 284 productive single-pool operators remain — and almost none of them pledge (like MPOs)

4 findings

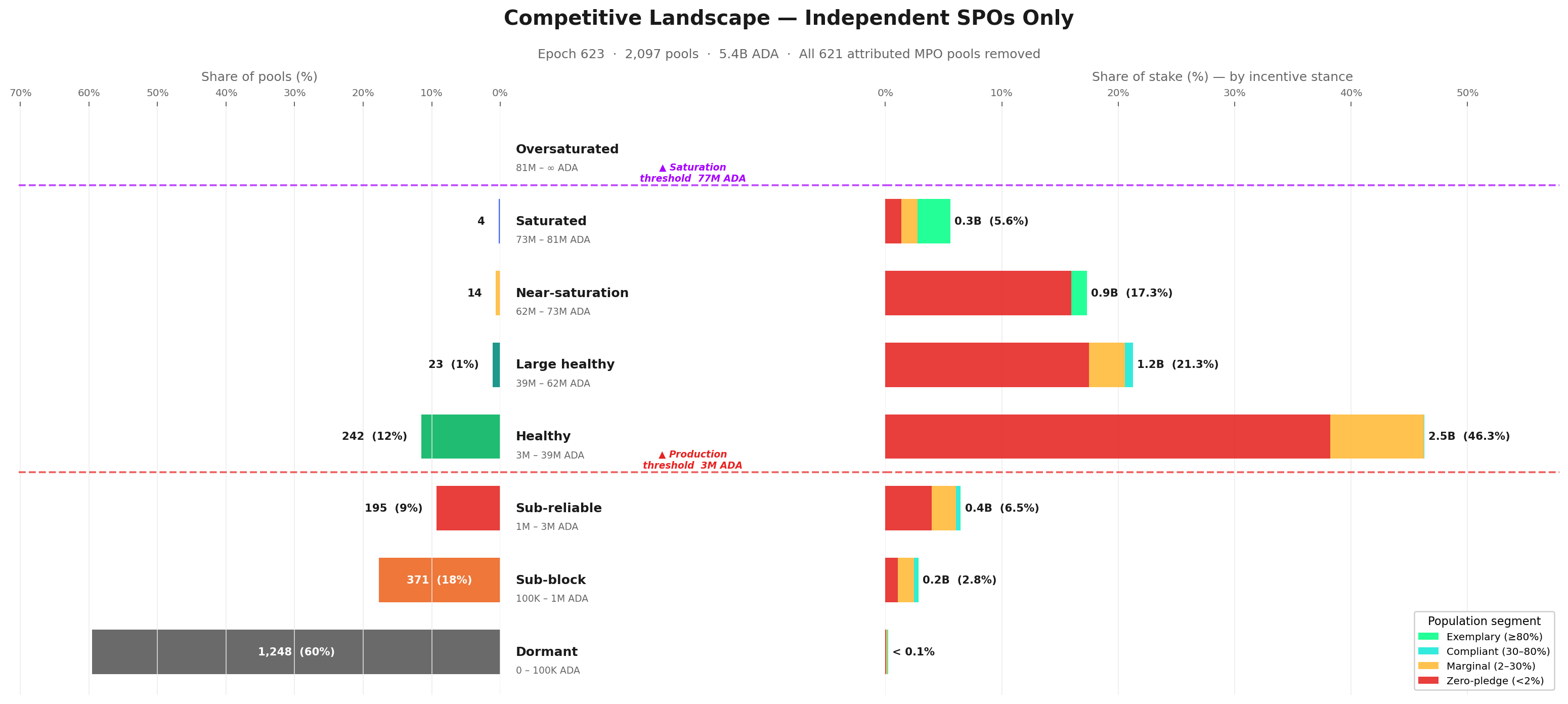

The "741 healthy pools" headline was 3× inflated. Strip out the fleet pools that were actually being run by multi-pool entities, and only 284 productive single-pool operators remain (productive = pool stake ≥3M ADA at epoch 623, the production threshold).

Almost none of them pledge.80.6% of single-pool productive stake sits at zero-pledge (< 2% pledge ratio). This is not irrational — at single-pool scale, the pledge bonus pays less than passive delegation, so locking ADA into the pledge is dominated. They are responding correctly to weak incentives, not failing to play.

Only 51 operators sit in the middle (pledge ratio between 2% and 30%) — the narrow group a parameter reform could plausibly move. Everyone else is either above the bar already (very rare) or below it (zero-pledge).

And the segment is shrinking. Its share of active stake fell from 28.0% → 25.0% since epoch 583 — capital is flowing toward MPO fleets, not toward the single-pool operators the mechanism was designed for.

The competitive field of single-pool operators is 3× smaller than the Incentive Mechanism Analysis headline. Lopez de Lara reported 741 'healthy' pools as evidence of a functioning incentive landscape; once MPO fleet members are stripped out, only 284 single-pool operators remain. 61% of the headline were fleet pools — operating under entity-level strategies (delegation source, fee setting, pledge), not the single-pool economics the headline was supposed to be about

At single-pool scale, pledging is rationally priced as not worth it.80.6% of single-pool productive stake (227 of 284 pools) sits in pools whose self-pledge is less than 2% of the stake they manage — call this zero-pledge: the operator has effectively declined the pledge bonus. The economics explain why: at single-pool scale, locking own ADA into the pledge yields at best 0.68%/year while passive delegation pays ~2.3%/year, so the pledge is dominated by the alternative use of capital at every realistic ratio. These operators are not failing to pledge — they are correctly responding to a formula that prices their effort below the delegation alternative.

Only 51 single-pool operators (18% of the 284) pledge a non-trivial fraction of their stake — and that small group is the entire population a parameter reform could move. "Marginal" here means pledge ratio between 2% and 30% — operators who have engaged with the bonus but are not capturing it meaningfully (bonus capture scales roughly linearly with pledge ratio, so a 2–30% pledge captures only 2–30% of the available bonus). They hold 685M ADA — 13.9% of single-pool productive stake. Everyone outside this band is either above the bar already (≥30%, very rare at single-pool scale — 6 operators total) or below it (zero-pledge — bonus not worth the opportunity cost); so any parameter reform that aims to move pledge upward has only this 51-operator middle to work with

Single-pool operators are quietly losing ground — the segment is shrinking, but its pledge mix is not improving. Single-pool operators' share of active stake fell from 28.0% to 25.0% since epoch 583 (a 3 percentage-point loss in 35 epochs). Inside the segment, the split between zero-pledge / marginal / compliant operators has barely moved across the same window — the decline is in volume, not in behaviour. Capital flowed away from single-pool operators toward MPO fleets; the operators who remained kept the same pledge mix

Slow structural decline

POL.O7

Observation 07 · 3 findings

The pledge mechanism reaches only 36% of stake — and the 64% outside it splits into three populations no single parameter can pull back in

3 findings

The pledge bonus was designed to discipline operator behaviour across the network. In practice it reaches only 36% of active stake (7.89B ADA) — single-pool operators plus the few MPOs that pledge meaningfully.

The other 64% is unreachable for three different reasons, each requiring a different fix: (i) Architectural — 10 entities, 7.39B ADA. CEX + IVaaS legally cannot pledge — exchanges custody retail balances, institutional validators run client assets they don't own. (ii) Strategic — 32 sovereign saturation-scale MPOs, 4.80B ADA. Community fleets, independent MPOs, multi-brand fleets, ecosystem stewards. They could pledge — they choose not to because the bonus pays less than passive delegation at their scale. (iii) Sub-scale — 35 sub-saturation MPOs, 1.69B ADA. Aggregate stake below one saturation cap; the pledge bonus is mechanically too small at their size to register.

77 of 83 attributed entities sit in one of these three buckets. Conflating them into a single "raise $a_0$" debate is why parameter reform alone keeps producing the same equilibrium.

The pledge mechanism's actual reach is 36% of active stake — 7.89B ADA. Strip out the entities that don't respond to the pledge signal, and what remains (single-pool operators + the few MPOs that do pledge meaningfully) carries 7.89B ADA out of ~21.7B active. The other 13.89B ADA — 65.6% of productive stake — is held by entities the bonus does not reach. The mechanism was designed to discipline operator behaviour across the whole network; in practice it operates on roughly a third of it.

MPO non-response splits into three distinct populations — confusing them is what keeps reform from working.Architectural: 10 entities (CEX + IVaaS) holding 7.39B ADA that cannot pledge by law/business model — exchanges custody retail balances, institutional validators run client assets they don't own. Strategic: 32 sovereign saturation-scale MPOs holding 4.80B ADA that could pledge but choose not to — at their scale the bonus pays less than passive delegation. Sub-scale: 35 sub-saturation MPOs holding 1.69B ADA whose entire fleet cannot fill one saturated pool — pledging is mechanically too small to matter. These are three different problems wearing the same label

No single parameter change addresses all three populations — each requires a different lever.Architectural responds to constitutional or contractual change (or to accepting that ~7.4B ADA is permanently outside the mechanism's scope). Strategic responds to altering the relative payoff of pledging vs delegating — i.e., reforming the pledge-yield curve so the bonus is no longer dominated. Sub-scale responds to a structural path (e.g., a shared-operations layer) for stake that cannot reach saturation alone. Raising $a_0$ — the "calibration" lever — addresses only the strategic group, and weakly

The scheme has been operational on mainnet since the Shelley hard fork on 2020/07/29 and its core parameters ($a_0$, $k$, $\rho$, $\tau$) have never been modified since.

This section presents the mechanism in two parts: the upstream pipeline that produces the budget (The Staking Populations), and the formula that allocates it across pools (Transaction Submitters–2.3). Understanding both is necessary to interpret the efficiency and behavioural analysis that follows.

2.1. Upstream: how the pools pot is assembled

Before any individual pool receives rewards, the protocol must answer a prior question: how much ADA is available this epoch?

The answer comes from the Treasury & Pool Pots Distribution stage — the first layer of the reward pipeline. Each epoch, the protocol assembles an epoch pot from three on-chain sources, then splits it between the treasury and the pools:

On mainnet: $\rho = 0.3\%$ (monetary expansion rate), $\tau = 20\%$ (treasury take). The split is exhaustive — nothing is lost.

In practice, this stage is dominated by a single input: monetary expansion accounts for ~99.8% of the epoch pot. Transaction fees contribute ~0.19%; deposits are unmeasurable at epoch granularity.

SPOs produce ~97% of assigned blocks on average, so the pot assembles reliably. The mechanism works — but it runs on a finite fuel supply.

Key facts from the upstream analysis (documented in the companion report Treasury & Pool Pots Distribution):

The reserve has crossed its half-life. From 13.29B to 6.53B ADA in 5.5 years. The nominal expansion draw has halved from ~39.9M to ~19.5M ADA/epoch. Significant reward pressure is projected around epochs 1000–1200 (~2028–2029).

Fee revenue is orders of magnitude below self-sufficiency. Even at full realistic capacity (~3.1 TPS), fees would cover only ~1.3% of the reserve expansion term. Reaching fee self-sufficiency requires fee revenue to grow by ~100× (two orders of magnitude) — combining a capacity upgrade (Leios), structurally higher transaction demand, and higher per-tx pricing (no single lever suffices).

Only ~44% of the pools pot is distributed. Of the ~15.5M ADA entering the pool-distribution stage at epoch 616, only ~6.8M reaches operators and delegators. The rest returns to the reserve — primarily because 43.5% of circulating ADA does not participate in delegation.

Reward parameters have never been adjusted. $\rho = 0.3\%$ and $\tau = 20\%$ are unchanged since Shelley inception. Neither has been the subject of a formal governance proposal.

These upstream conditions define the sustainability context within which the pool-level mechanism operates. They are outside the scope of the pool-distribution formula analysed below — but they set the budget ceiling that makes every inefficiency at this layer more consequential.

2.2. Flow overview

The pools pot ($PoolsPot^{\text{epoch}}$) enters this stage as a single budget. The protocol distributes it across individual pools in three steps:

Saturation clipping. Both total stake ($\sigma_i$) and pledge ($s_i$) are capped at the saturation threshold $z_0 = 1/k$. This prevents any single pool from capturing a disproportionate share.

Reward curve evaluation. A reward function $f$ computes the pool's optimal allocation from its clipped stake and pledge. The curve has two components: a base stake term (proportional to delegation) and a pledge-bonus term (nonlinear, governed by $a_0$). The pledge bonus is meant to reward operator commitment ("skin in the game").

Performance adjustment. The optimal allocation is scaled by apparent performance $\bar{p}_i$ to produce the actual allocation. Pools that miss blocks receive less. If the registered pledge is not met, the allocation is zeroed entirely.

Any rewards not distributed ($\sum_i \hat{f}_i < R$) return to the reserve.

Two design choices matter for the rest of the analysis:

Pledge sensitivity via $a_0$. The parameter $a_0$ controls how much additional reward a pool can earn through pledge. At $a_0 = 0.3$, the pledge bonus represents at most ~23% of the optimal allocation. Whether this is sufficient to meaningfully incentivise pledge is a central question.

Uniform saturation threshold. All pools share the same cap $z_0 = 1/k$. There is no mechanism to differentiate saturation based on pledge level or pool characteristics — CIP-0050 and CIP-0037 both propose to change this.

$$

\hat f(s,\sigma,\bar p) := \bar p \cdot f(s,\sigma)

$$

$$

\sum_i \hat f(s_i,\sigma_i,\bar p_i) \le R

$$

$$

R - \sum_i \hat f(s_i,\sigma_i,\bar p_i) \; \text{is not paid out and remains accounted in } (T_{\infty}-T)

$$

$$

\text{if pledge not met in epoch } \Rightarrow \hat f = 0

$$

2.3.2. Interpretation of the original reward function

The core reward function is evaluated on the clipped inputs

$s' := \min(s,z_0)$ and $\sigma' := \min(\sigma,z_0)$, not directly on the raw quantities $s$ and $\sigma$.

Thus:

$s$ — operator pledge before clipping

$\sigma$ — total stake delegated to the pool before clipping

$s'$ — pledge after clipping at the saturation threshold

$\sigma'$ — total stake after clipping at the saturation threshold

The function has two components:

A base term, $\sigma'$, which rewards stake up to saturation.

A pledge-bonus term, $s'a_0 \cdot \dfrac{\sigma' - s'\left(\frac{z_0-\sigma'}{z_0}\right)}{z_0}$.

The factor $\left(\frac{z_0-\sigma'}{z_0}\right)$ measures the remaining headroom before saturation. As the pool approaches saturation, this headroom shrinks and the pledge-bonus term is progressively dampened. The outer factor $\dfrac{R}{1+a_0}$ keeps the overall reward mass bounded.

2.3.3. Why rewrite the original formulation

The original SL-D1 formula is correct, but awkward to analyze directly:

It mixes two separate concerns in a single expression — the clipping step that enforces saturation, and the reward computation performed after clipping.

The pledge-sensitive part is harder to read than it needs to be. The term $\sigma' - s'\left(\frac{z_0-\sigma'}{z_0}\right)$ hides a quadratic dependence on pledge that only becomes obvious after expansion.

The most natural coordinates for analysis are not the raw stake shares $s$ and $\sigma$, but their positions relative to the saturation threshold $z_0$.

2.3.4. Normalized coordinates: pool size and pledge ratio

In the non-saturated regime where clipping is inactive ($s' = s$, $\sigma' = \sigma$), we introduce two dimensionless coordinates that capture the two structurally independent degrees of freedom an operator controls:

Under $0 < s \le \sigma \le z_0$, these satisfy $0 \le \nu \le 1$ and $0 \le \pi \le 1$. The pair $(\nu, \pi)$ ranges over the unit square $[0,1] \times [0,1]$.

The variables have a direct interpretation:

$\nu$ is the stake saturation level — what fraction of the saturation threshold is covered by the pool's total stake. $\nu = 1$ means the pool is fully saturated; $\nu = 0$ means it is empty.

$\pi$ is the within-pool pledge ratio — the fraction of the pool's stake that the operator commits as their own. $\pi = 0$ means a hollow pool (zero pledge); $\pi = 1$ means the operator owns 100 % of the pool (full self-pledge).

An important structural property emerges: the allocation depends only on how big the pool is relative to saturation and on the operator's commitment fraction — not on absolute ADA values.

The saturation threshold $z_0$ acts purely as a scaling parameter; the shape of the reward curve is governed by $a_0$ alone.

Pledge in absolute terms recovers as $s = \pi \cdot \sigma = \pi \nu z_0$. Substituting $\sigma = \nu z_0$ and $s = \pi \nu z_0$ into the non-saturated SL-D1 formula gives:

which we call the pledge-bonus activation function. Its factorisation into an outer size factor $\nu^2$ and an inner pledge-intensity factor $\pi\bigl[1 - \pi(1-\nu)\bigr]$ is the central observation for the rest of the analysis: pool size and commitment intensity contribute to the bonus multiplicatively, with the size factor dominating at low $\nu$.

2.3.5. Reader-friendly reward function

Define three derived quantities:

Symbol

Name

Definition

Interpretation

$P_{\max}$

Reward ceiling

$z_0R$

Maximum any single pool can earn per epoch. In the ideal design, $k$ pools each earn $P_{\max}$ and the full pot is distributed.

$\lambda_{\text{size}}$

Size fraction

$\frac{1}{1+a_0}$

Share of $P_{\max}$ accessible through stake alone (zero pledge). Defines the size ceiling.

$\lambda_{\text{pledge}}$

Pledge fraction

$\frac{a_0}{1+a_0}$

Remaining share of $P_{\max}$ unlockable by pledge. The commitment premium.

These satisfy $\lambda_{\text{size}} + \lambda_{\text{pledge}} = 1$.

The envelope determines what fraction of $P_{\max}$ the pool captures, and ranges from 0 to 1:

Tier

Envelope value

What it requires

Interpretation

Absolute ceiling

$E = 1$

$\nu = 1, \pi = 1$

Full saturation + full self-pledge → pool earns $P_{\max}$

Size ceiling

$E = \lambda_{\text{size}}$

$\nu = 1, \pi = 0$

Full saturation, zero pledge → pool earns $\lambda_{\text{size}} \times P_{\max}$

Typical pool

$E \ll 1$

$\nu \ll 1$

Undersaturated → reward scales linearly with $\nu$

Two structural properties of the envelope:

The base term $\lambda_{\text{size}}\nu$ is linear in $\nu$ — it depends only on total pool size relative to saturation. The distribution of stake across pools does not affect the aggregate base.

The bonus term $\lambda_{\text{pledge}}\,A(\nu, \pi)$ is non-linear and asymmetric in its two inputs. The outer factor $\nu^2$ imposes a quadratic size penalty that holds at every pledge ratio: even at the optimal $\pi$, a pool earns bonus proportional to $\nu^2$. At full self-pledge ($\pi = 1$) the inner factor degenerates and the bonus collapses to $\lambda_{\text{pledge}}\nu^3$ — the cubic that suppresses the bonus structurally for any pool below saturation and concentrates the reward signal in the largest pools.

The size ceiling is accessible to any saturated pool regardless of pledge. The commitment premium reserves 23.1% of $P_{\max}$ for pledge activation — but unlocking it requires operator capital equal to the full saturation threshold.

The implied yield on that capital ($\lambda_{\text{pledge}} \cdot P_{\max}$ annualized / $z_0$ in ADA) is substantially below the passive delegation yield, making the pledge bonus economically weak as an incentive.

The full formula including apparent performance reads as a cascade:

Each factor acts as a discount from $P_{\max}$. When all three equal their ideal value, the pool earns the full ceiling. Every departure reduces the payout, and the difference returns to the reserve.

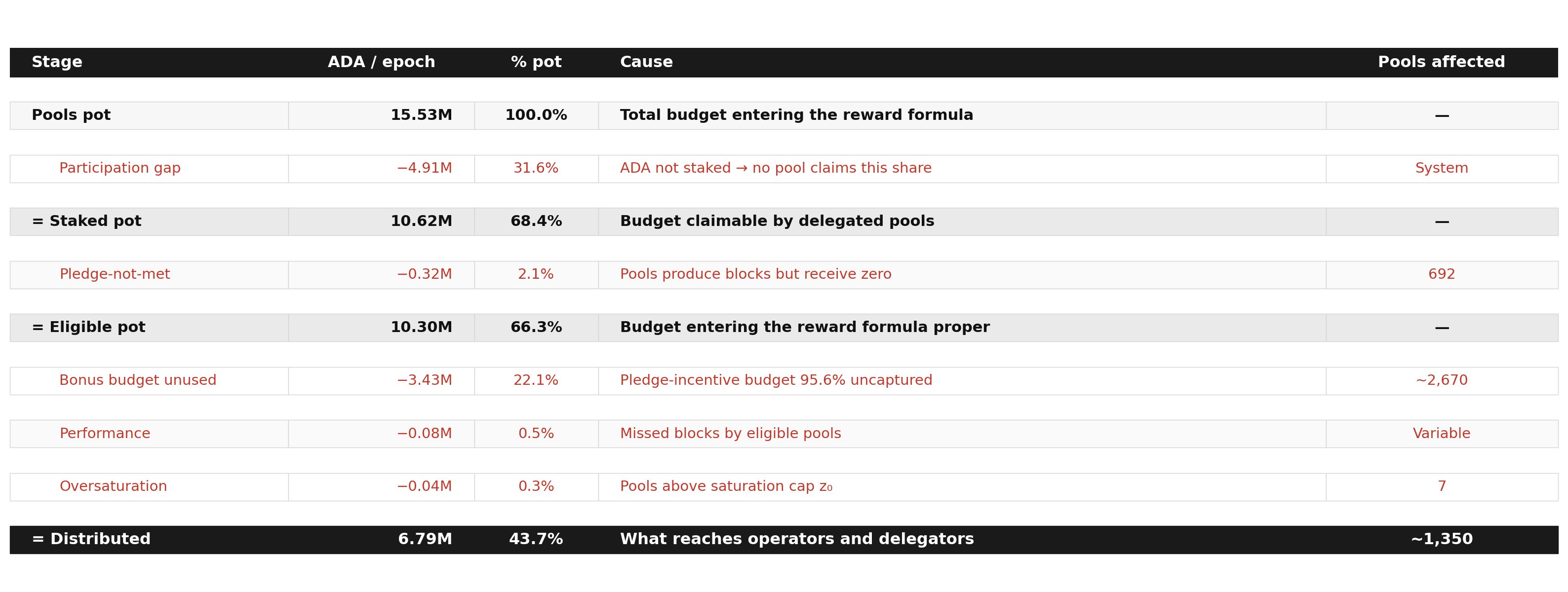

56.3% of the pools pot never reaches operators or delegators. Of the 15.53M ADA entering this stage at epoch 616, only 6.79M ADA was distributed. The rest returned to the reserve.

This section traces where the pot goes, step by step. Each step removes a slice before the next cause can act, and at each step the formula is opened to show why that slice is lost.

3.1. The participation gap

The pools pot is sized for the full circulating supply. With 43.5% of ADA undelegated, a proportional share of the pot has no pool to claim it.

ADA/epoch

% of pot

Pools pot

15.53M

100%

Participation gap

−4.91M

31.6%

Staked pot

10.62M

68.4%

FromObservationPOL.O1 — Participation gap and unused pledge-incentive budget return 54% of the pool pot to reserve

Finding#2→ ADA that isn't staked at all is the single largest source of waste. Every epoch, 4.91M ADA is forfeited because roughly a third of the supply sits unstaked — that's 31.6% of the pot, returned to the reserve before the formula even gets a chance to distribute it. Because the base is distribution-neutral, this gap depends only on how much ADA is staked — not on how it is arranged across pools. No formula change can close it. Only increased staking participation can.

3.2. Pledge-not-met confiscation

When a pool operator declares a pledge in their pool certificate but the owners' stake keys do not actually hold that amount at the epoch boundary, the protocol sets the pool's reward to zero for the entire epoch. Not a reduction — a total confiscation.

The pool still produces blocks and contributes to consensus. The delegators' ADA still participates in the protocol. But neither operator nor delegators receive anything.

It is the only pathway where the network does real work and gets nothing in return.

ADA/epoch

% of pot

Staked pot

10.62M

68.4%

Pledge-not-met confiscation

−0.32M

2.1%

Eligible pot

10.30M

66.3%

At epoch 615, 692 pools failed this check. They produced 1,049 blocks, and their 1.08B ADA of delegated stake earned nothing. The confiscated 0.32M ADA/epoch (~23M/year) is almost entirely base reward — these pools had near-zero pledge, so their bonus entitlement was negligible.

This happens more often than one might expect. Historically, 2,797 pools have experienced at least one pledge-unmet epoch, and 833 are chronically in default (pledge met less than 50% of the time).

The typical cause is operational: an operator moves ADA out of their pledge wallet for liquidity or DeFi, or mishandles a key rotation, and doesn't realize the consequence until rewards are already lost.

3.3. The reward formula

Before going further down the waterfall, the formula that governs everything below this point must be opened. Each pool's reward is:

Three multiplicative factors. When all three equal their maximum, the pool earns the full ceiling $P_{\max}$. Every departure from the ideal is a multiplicative discount — and the uncaptured fraction returns to the reserve.

Protocol parameters governing this stage. Three parameters directly control pool-level distribution. All have been constant since reaching their current value.

Parameter

Symbol

Value

History

Target pool count

$k$

500

Raised from 150 to 500 at epoch 257, unchanged since

Pledge influence

$a_0$

0.3

Set at Shelley (epoch 208), never changed

Saturation point

$z_0$

76.99M ADA

Mechanical consequence of $k$ and supply

In the ideal design, $k = 500$ pools each earn $P_{\max}$, and the full pot is distributed. On mainnet, the sum of all pool rewards is 6.79M ADA — only 43.7%.

The envelope $E$ splits into two additive components that explain where the rest goes:

The base is distribution-neutral: 100M ADA in one pool earns exactly the same base as 100M split across ten pools.

The bonus is distribution-sensitive: the activation function $A(\nu, \pi) = \nu^2 \cdot \pi \cdot [1 - \pi(1-\nu)]$ is non-linear, with an outer factor $\nu^2$ that imposes a quadratic size penalty at every pledge ratio. Under full self-pledge ($\pi = 1$) the inner factor degenerates and the bonus collapses to $A(\nu, 1) = \nu^3$ — cubing sub-unit values crushes them.

This split — 76.9% for size, 23.1% for pledge — is the key to understanding everything that follows.

3.4. The eligible pot and the pledge problem

After removing the participation gap and confiscated rewards, 10.30M ADA/epoch remains — the "eligible pot". This is what the formula distributes among pools that passed the pledge check.

Within it, the single largest loss is the unused pledge budget.

3.4.1. Why pledge matters — and why this is not zero-sum

The formula reserves $\lambda_{\text{pledge}} = 23.1\%$ of the pot — 3.58M ADA every epoch — as a bonus for operators who self-pledge. This is not a reward optimisation. It is the protocol's primary Sybil-resistance mechanism.

The design specification (Brünjes et al., 2020) is explicit: the pledge requirement exists so that "an adversary who wishes to increase his chances of being elected [must] split his stake among several stakepools, decreasing each pool's apparent pledge and therefore its attractiveness."

Pledge is the economic barrier that makes pool proliferation expensive. Without it, the cost of running a pool farm drops to near zero and the network's decentralisation guarantees erode.

The Incentive Mechanism Analysis characterised the pledge-bonus shortfall as economically neutral — a zero-sum redistribution where uncaptured ADA returns to the reserve. That framing is incomplete.

The 22.1% of the pot that returns unused is not idle capital awaiting redistribution. It is the budget the protocol explicitly allocates to its own security model — and 95.6% of that budget fails to activate.

FromObservationPOL.O1 — Participation gap and unused pledge-incentive budget return 54% of the pool pot to reserve

Finding#3→ Almost all of the pledge-bonus budget is wasted. Every epoch, 3.43M ADA earmarked as the pledge bonus returns unclaimed — 22.1% of the pot and 95.6% of the bonus allocation. Unlike the participation gap, this loss is entirely within the formula's control — it is the single largest inefficiency that incentive reform can address.

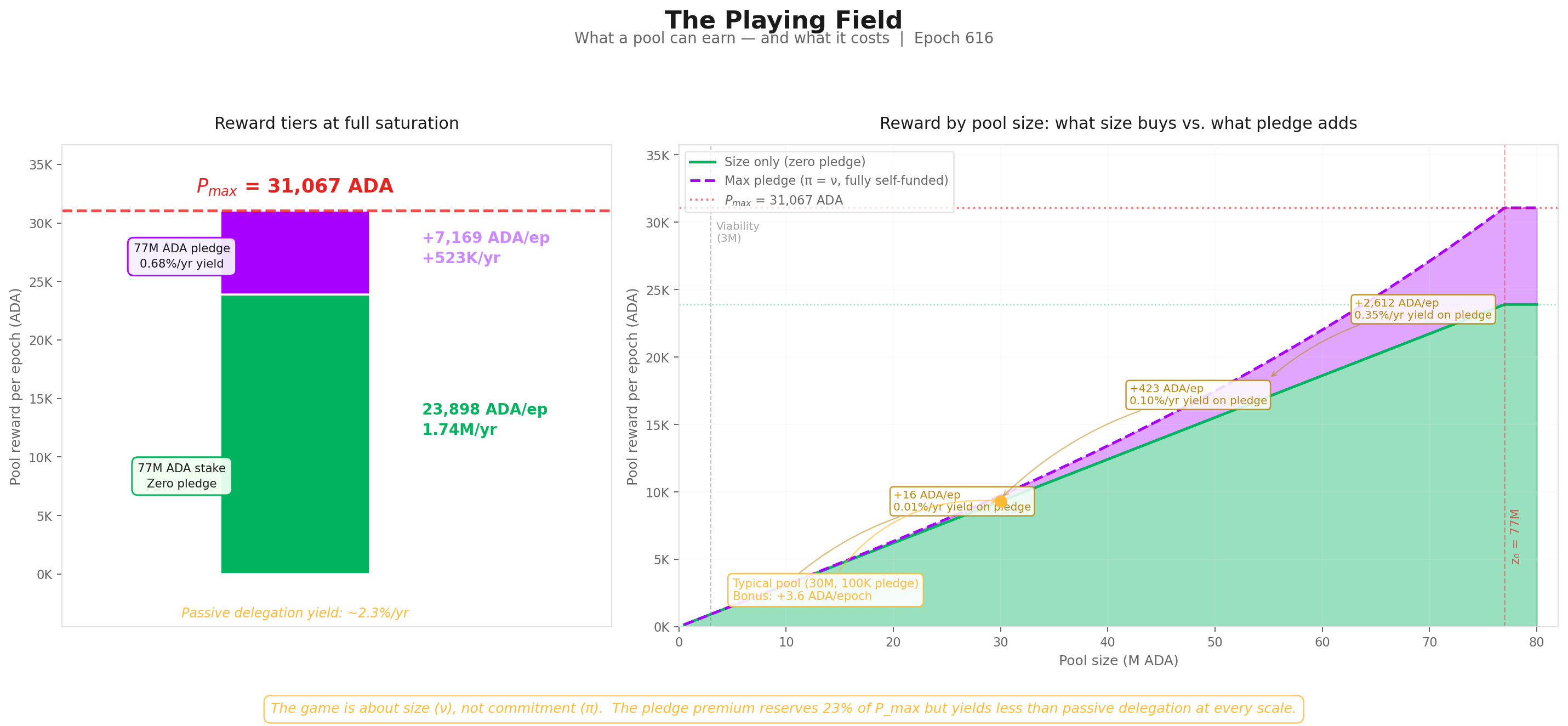

3.4.2. The playing field: what pledge actually buys

FigurePOL.3.1The pledge "playing field" as a stack of reward tiers. Any saturated pool earns the size ceiling (76.9% of $P_{\max}$) without pledging; the remaining 23.1% bonus requires the operator to pledge the full saturation amount (77M ADA) — a yield of just 0.68%/yr on locked capital.

Three reward tiers:

Tier

Reward/epoch

Reward/year

What it requires

$P_{\max}$ — absolute ceiling

31,067 ADA

2.27M ADA

77M ADA stake + 77M ADA pledge + $\bar{p}=1$

Size ceiling — zero pledge

23,898 ADA

1.74M ADA

77M ADA stake + $\bar{p}=1$. No pledge needed.

Pledge bonus — the gap

7,169 ADA

523K ADA

The difference. Requires 77M ADA of personal capital pledged.

The size-only ceiling ($\lambda_{\text{size}} \times P_{\max}$) is what any saturated pool earns regardless of pledge. It captures 76.9% of $P_{\max}$. The remaining 23.1% requires the operator to pledge the entire saturation amount (77M ADA).

The implied yield: $523\text{K ADA/yr} \div 77\text{M ADA} = \mathbf{0.68\%\text{/yr}}$ — below the passive delegation yield of ~2.3%/yr.

The bonus at every scale:

Pool size

ν

Zero-pledge reward

Full self-pledge (π=1) reward

Bonus

Relative uplift

Yield on pledge capital

3M ADA

0.039

931 ADA/ep

932 ADA/ep

+0.4 ADA

+0.05%

0.001%/yr

10M ADA

0.130

3,104 ADA/ep

3,120 ADA/ep

+16 ADA

+0.5%

0.011%/yr

30M ADA

0.390

9,312 ADA/ep

9,736 ADA/ep

+424 ADA

+4.6%

0.10%/yr

50M ADA

0.649

15,520 ADA/ep

17,484 ADA/ep

+1,964 ADA

+12.7%

0.29%/yr

77M ADA

1.000

23,898 ADA/ep

31,067 ADA/ep

+7,169 ADA

+30.0%

0.68%/yr

A 10M ADA pool where the operator pledges the entire pool earns 16 ADA more per epoch — a yield of 0.01%/yr on a 10M lockup.

A typical healthy pool (30M ADA stake, 100K ADA pledge) gains 3.6 ADA/epoch from pledge — less than the variance of a single block.

FromObservationPOL.O2 — Pledge is unused at scale and structurally unfair across pool sizes

Finding#2→ Pledging earns less than passive delegation, even at maximum scale. A fully-saturated pool whose operator pledges the entire saturation amount earns just 0.68%/yr on that pledged capital — below the 2.3%/yr anyone can earn by passively delegating. At every realistic scale, the bonus is too small to justify the capital lockup. The "game" for operators is overwhelmingly about size (ν), not commitment (π).

The bonus exists in the formula but not in the economics.

3.4.3. The envelope mechanics — and the three structural defects of A

The proportioning envelope splits each pool's reward into a size-proportional base and a pledge-tied bonus:

The base is well-behaved — purely proportional to saturation, independent of pledge. A zero-pledge pool earns $E(\nu, 0) = 76.923\% \cdot \nu$, and at full saturation it captures 76.9% of $P_{\max}$. The remaining 23.1% is gated by the activation function $A(\nu, \pi)$ — and that is where the pledge problem lives.

A factorises into a size factor and a pledge-intensity factor:

The two factors are independent and multiplicative. This factorisation is decisive — three structural defects follow from it directly. They are pre-empirical: properties of the algebra that hold regardless of $a_0$, regardless of mainnet data, regardless of any CIP that operates around (rather than on) A.

Defect 1 — Quadratic size penalty applies at every pledge ratio.

The outer $\nu^2$ multiplies every $(\nu, \pi)$ configuration. A small pool is quadratically penalised for being small before pledge enters the picture. Even at the optimal pledge ratio for a given pool size, the bonus is still scaled by $\nu^2$. At $\nu = 0.1$ (a 7.7M pool), the bonus contribution is capped at 1% of what a saturated pool earns, no matter how committed the operator.

FromObservationPOL.O2 — Pledge is unused at scale and structurally unfair across pool sizes

Finding#4→ Small pools cannot earn meaningful pledge bonus, no matter how committed the operator. The formula scales the bonus by pool-size squared ($\nu^2$) before pledge is priced — at every pledge ratio. A pool at 10% of saturation is structurally capped at 1% of the bonus a saturated pool earns, regardless of operator commitment. The penalty is permanent: it holds at every $\pi$ and cannot be unlocked by raising $a_0$ or any other parameter that does not touch A itself.

Defect 2 — A is non-monotone in π for any ν < 0.5.

This is zero at $\pi^* = 1 / [2(1-\nu)]$. Two regimes:

ν ≥ 0.5: $\pi^* \geq 1$. The maximum sits at or beyond the unit interval; A is monotone increasing in π over $[0, 1]$. Pledging more always earns more bonus.

ν < 0.5: $\pi^* < 1$. The maximum sits strictly inside $[0, 1]$. Pledging beyond $\pi^*$ pays less, not more. A pool at half-saturation peaks at $\pi = 1$; below half-saturation, fully self-pledging destroys part of the bonus the operator could have earned by committing less. Essentially the entire mainnet population sits below half-saturation.

Worked example at $\nu = 0.3$ (a Healthy-tier pool ≈ 23M ADA):

π

A(0.3, π)

vs. interior max

0.30

0.0233

-27%

0.50

0.0292

-9%

0.714 (= π*)

0.0321

max

0.80

0.0317

-1%

1.00 (full self-pledge)

0.0270

-16%

The formula whose stated purpose is "skin in the game" pays the operator less for putting in more skin, for the entire population of pools below half-saturation.

FromObservationPOL.O2 — Pledge is unused at scale and structurally unfair across pool sizes

Finding#5→ Pledging more pays less past a sweet spot — for almost every pool on mainnet. For any pool below half-saturation, the bonus peaks at an interior pledge ratio $\pi^{*} = 1/[2(1-\nu)] < 1$, and pledging beyond that point reduces the bonus. At $\nu = 0.3$ the peak sits near 71% pledge ratio, and full self-pledge pays 16% less than the peak. The formula formally rewards operators for under-committing — across essentially the entire mainnet pool landscape.

Defect 3 — Cubic collapse at full self-pledge.

At $\pi = 1$, the inner factor degenerates and the bonus reduces to:

$$A(\nu, 1) = \nu^3 \qquad \Rightarrow \qquad \text{bonus at full self-pledge} = \lambda_{\text{pledge}} \cdot \nu^3$$

The strongest possible commitment signal — every ADA pledged is the operator's own — is paid the worst-case scaling on sub-unit ν. The protocol designed an instrument to reward maximal commitment, and the algebra punishes it on size alone.

Saturation (ν)

$A(\nu, 1) = \nu^3$

Bonus (% of $P_{\max}$)

Total $E$

Relative uplift over zero-pledge

1.0 (full)

1.000

23.077%

100%

30.0%

0.8

0.512

11.82%

73.36%

19.2%

0.5

0.125

2.88%

41.35%

7.50%

0.3

0.027

0.62%

23.70%

2.70%

0.1

0.001

0.023%

7.72%

0.30%

FromObservationPOL.O2 — Pledge is unused at scale and structurally unfair across pool sizes

Finding#6→ The strongest possible commitment signal is paid the worst-case reward. When the operator pledges 100% of their own pool ($\pi = 1$), the bonus collapses to pool-size cubed ($\nu^3$). A half-saturated pool earns 12.5% of the maximum bonus; a pool at 10% of saturation earns just 0.1%. The protocol designed an instrument to reward maximal commitment, and the algebra punishes it on size alone.

The three defects compound. Defect 1 ensures small pools cannot earn meaningful bonus at any pledge level; Defect 2 ensures that within the small-pool regime, more commitment pays less past an interior optimum; Defect 3 ensures that even the maximum signal is suppressed by the size penalty cubed. The intended MPO-splitting penalty (the $-\pi^2(1-\nu)$ term in the inner factor) is achieved at the cost of all three.

The mechanism was designed for a world of 500 saturated pools; the actual landscape cannot activate it — and the algebra would fight it even if it could.

For a deeper walk-through — three operators (Bob at $\nu \approx 0.03$, Charles at $\nu \approx 0.22$, Alice at $\nu \approx 1$) traced across three pledge scenarios, and the implications for CIP-0050 / CIP-0037 which operate around A rather than on it — see the stake-cap synthesis, §2.2 The deeper bottleneck — A(ν, π) itself.

3.4.4. The evidence on mainnet

Absolute pledge amounts are misleading — a 1M ADA pledge means something very different for a saturated pool (ν ≈ 1, π ≈ 0.013) than for a small one (ν ≈ 0.1, π ≈ 0.13).

The relevant metric is the pledge ratio: declared pledge divided by active stake. This is what the formula actually prices through the $A(\nu, \pi)$ term.

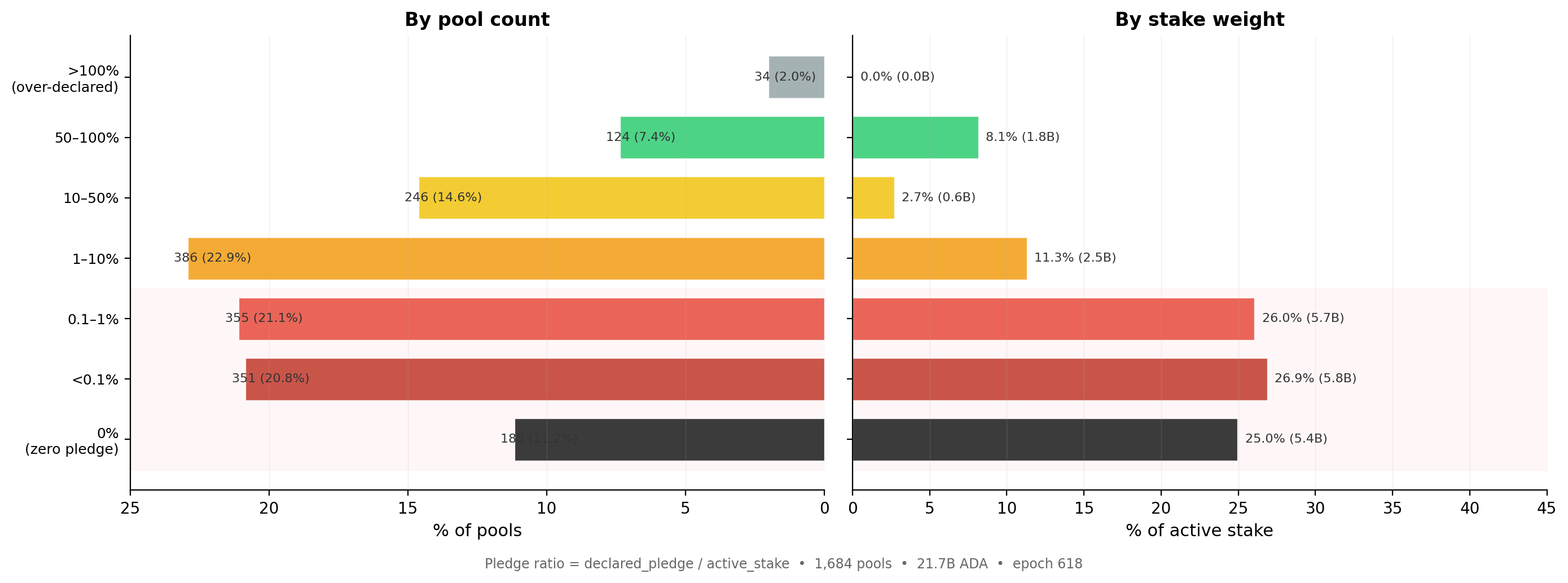

FigurePOL.3.2Distribution of pledge ratio (declared pledge ÷ active stake) across the 1,684 pools with meaningful delegation. 78% of staked ADA sits in pools with ratio < 1%, and the stake-weighted median is 0.07% — pledge is functionally absent where stake concentrates.

The chart covers the 1,684 registered pools with meaningful delegation (active stake > 10K ADA), excluding dormant and zombie registrations.

Pledge ratio threshold

Cumul. % of pools

Cumul. % of stake

Stake (ADA)

< 0.1%

32.0%

51.9%

11.3B

< 1%

53.1%

78.0%

16.9B

< 10%

76.0%

89.4%

19.4B

78% of all staked ADA sits in pools where the operator pledges less than 1% of managed stake, and 89% below 10%. Only one ADA in ten is delegated to a pool where the operator commits more than a tenth of the stake they manage.

The stake-weighted median pledge ratio is 0.07% — meaning half of all staked ADA sits in pools where the operator's personal commitment is less than one thousandth of delegated funds.

The unweighted median (0.73%) is 10× higher, reflecting the many smaller community pools with genuine skin-in-the-game but little stake weight.

FromObservationPOL.O2 — Pledge is unused at scale and structurally unfair across pool sizes

Finding#1→ Almost no operator pledges meaningfully.78% of staked ADA sits in pools where the operator pledges less than 1% of the stake they manage; the stake-weighted median pledge ratio is 0.07%. Pledge is absent precisely where stake concentrates. The pools that dominate the network in economic terms operate with near-zero pledge ratios — for them, the $A(\nu, \pi)$ term contributes essentially nothing.

This asymmetry is the structural signature of the pledge problem. At π = 0.001 (pledge ratio 0.1 %) and ν = 0.5 (a half-saturated pool), the bonus is approximately 0.006 % of $P_{\max}$ — and at the stake-weighted median π = 0.0007, even smaller still.

The anti-Sybil mechanism is present in the formula but absent from the economics.

3.5. Performance and oversaturation

Two minor waste sources complete the picture:

Performance ($\bar{p}$). A pool's actual block production relative to its VRF-assigned expectation. The network-wide aggregate averages 0.977 — meaning ~2.3% of the pot is lost to missed blocks. This is the only factor the operator directly controls through infrastructure quality. For sub-block pools (expected blocks < 3/epoch), Poisson variance dominates and epoch-to-epoch results are noisy, but in aggregate the effect is small: 0.5% of the pot.

Oversaturation. Seven pools hold stake above $z_0 = 76.99\text{M ADA}$; the excess earns nothing. The saturation cap was designed for 500 pools; only 8 reach it. It binds on 0.3% of the pot.

Combined: 0.8% of the pot. These are well-functioning mechanisms that do their job — they are not the problem.

3.6. Summary

3.6.1. Current snapshot

FigurePOL.3.3Single-epoch waterfall (epoch 616) tracing the 15.53M ADA pool pot from the participation-gap loss (31.6%) through the unused pledge-incentive budget (22.1%) and the secondary leakages, down to the 6.79M ADA / 44% that actually reaches operators and delegators.

Important

Key observation (POL.O1). Two causes account for 53.7% of the entire pools pot returning to reserve: the participation gap (31.6%) and the unused pledge budget (22.1%). Everything else — pledge-not-met confiscation (2.1%), performance (0.5%), oversaturation (0.3%) — is secondary by an order of magnitude. The reform priority is unambiguous: the participation gap is upstream and outside the formula's control; the unused pledge budget is the single largest inefficiency that incentive reform can address.

The supporting findings, each surfaced where its evidence sits:

FromObservationPOL.O1 — Participation gap and unused pledge-incentive budget return 54% of the pool pot to reserve

Finding#1→ Less than half the pool pot reaches its targets. Only 6.79M of the 15.53M ADA per epoch budgeted for distribution actually reaches operators and delegators — a 44% distribution efficiency. The other 56% returns to the reserve unused every epoch.

FromObservationPOL.O1 — Participation gap and unused pledge-incentive budget return 54% of the pool pot to reserve

Finding#4→ Two causes account for almost all the waste; everything else is rounding error. The participation gap and the unused pledge-incentive budget together return 53.7% of the pot to reserve. The remaining sources combined — pledge-not-met confiscation (2.1%), missed blocks (0.5%), oversaturation (0.3%) — add up to less than 3% of the pot. The reform priority is unambiguous.

FromObservationPOL.O2 — Pledge is unused at scale and structurally unfair across pool sizes

Finding#3→ The pledge bonus budget goes unused. Every epoch, 3.43M ADA — 22% of the pool pot — is reserved for the pledge bonus, but the formula's distribution mechanics return almost all of it to the reserve unclaimed (~250M ADA/year). This is the structural cost of maintaining $a_0 = 0.3$ on a landscape that cannot activate the bonus curve.

§4 — The pool landscape maps the population structure that produces this outcome — who controls which pools, who responds to the pledge signal, and who struggles below the production threshold.

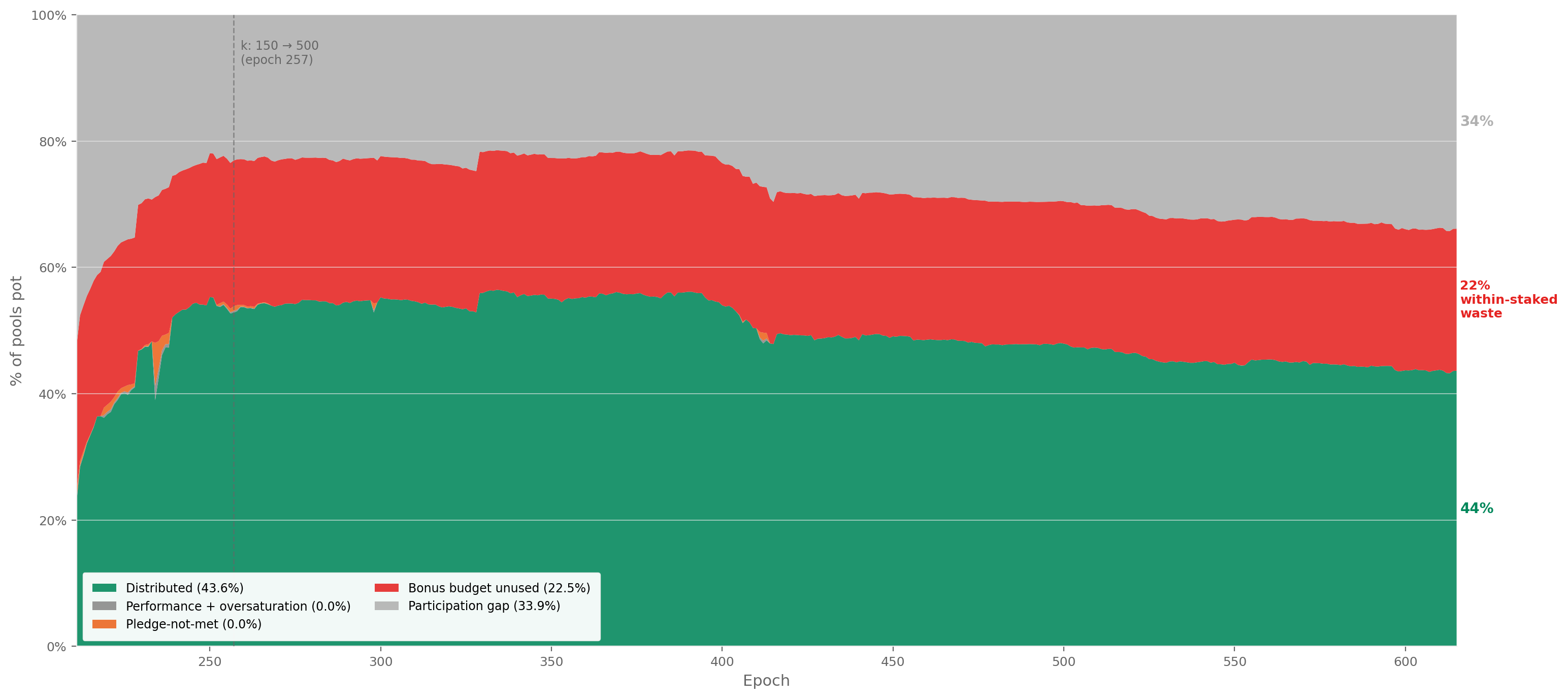

3.6.2. Historical evolution

FigurePOL.3.4Historical decomposition of the pool pot, Shelley launch (epoch 211) → epoch 615. Distribution efficiency peaked at ~55% around epochs 300–400 and has since degraded to 43.6%. The entire decline traces to the participation gap widening from ~22% to 34%; no other component has moved materially.

The historical decomposition reveals two facts that the single-epoch snapshot cannot:

The participation gap is the only component that has moved. Distribution efficiency peaked at ~55% around epoch 300–400 and has since degraded to 43.6%.

The entire decline traces to falling participation: the grey band widened from ~22% to 34% as the ratio of active stake to theoretical capacity ($k \times z_0$) fell. No other component changed materially.

The bonus budget has never activated. The red band — pledge bonus unused — has sat at ~22–23% of the pot since Shelley epoch 211. It was 23.1% when $a_0 = 0.3$ was set, and it is 22.5% today.

The pledge incentive was not functional at launch, did not improve after the $k$ increase at epoch 257, and has not responded to any subsequent change in the pool landscape.

This is not a recent degradation. It is a structural failure present since the mechanism was deployed.

3.6.3. Conclusion

What the Incentive Mechanism Analysis established. Lopez de Lara (2025) produced the first waterfall decomposition of the pools pot and identified the participation gap and the pledge-bonus shortfall as the two dominant waste channels. The analysis characterised the bonus shortfall as economically neutral — a zero-sum redistribution where uncaptured ADA returns to the reserve.

What this analysis adds. The zero-sum framing is incomplete. The pledge bonus is the protocol's primary Sybil-resistance mechanism — the economic cost that makes pool proliferation expensive.

When 95.6% of this budget fails to activate, the marginal cost of opening an additional pool drops to near zero. The mechanism designed to make pool farms expensive becomes permissive.

The 3.43M ADA returning to the reserve every epoch is the budget the protocol explicitly allocates to its own security model — and the five-year historical record (Historical evolution) confirms it has never responded to any change in the pool landscape. This is not a recent degradation; it is a structural failure present since the mechanism was deployed.

Furthermore, the yield analysis (The playing field: what pledge actually buys) shows the bonus is economically irrational to pursue at every realistic scale, and the mainnet evidence (The evidence on mainnet) confirms that operators have responded accordingly — pledge is absent precisely where stake concentrates.

FromObservationPOL.O1 — Participation gap and unused pledge-incentive budget return 54% of the pool pot to reserve

Finding#1→ Less than half the pool pot reaches its targets.6.79M of 15.53M ADA/epoch — 44% distribution efficiency.

Finding#2→ ADA that isn't staked at all is the single largest source of waste.4.91M ADA/epoch (31.6% of the pot) — upstream and outside the formula's control.

Finding#3→ Almost all of the pledge-bonus budget is wasted.3.43M ADA/epoch (22.1% of the pot, 95.6% of the bonus allocation) — the single largest inefficiency reform can address.

Finding#4→ Two causes account for almost all the waste; everything else is rounding error. Together 53.7% of the pot; secondary causes total under 3%.

FromObservationPOL.O2 — Pledge is unused at scale and structurally unfair across pool sizes

Finding#1→ Almost no operator pledges meaningfully.78% of staked ADA at pledge ratio < 1%; stake-weighted median 0.07%.

Finding#2→ Pledging earns less than passive delegation, even at maximum scale.0.68%/yr at saturation vs. 2.3%/yr passive — economically irrational to pledge.

Finding#3→ The pledge bonus budget goes unused.3.43M ADA/epoch reserved for the bonus returns unclaimed — the structural cost of $a_0 = 0.3$ on a landscape that cannot activate it.

§4 — The pool landscape identifies the actors who control this landscape and why they do not pledge.

4. The pool landscape — who wastes, who pledges, and who struggles

§3 — Distribution efficiency showed that 56.3% of the pools pot never reaches operators — and that the single largest addressable cause is the unused pledge-incentive budget:

3.43M ADA/epoch (~250M ADA/year) — returning to the reserve unused since Shelley launch.

The pledge mechanism — designed as Cardano's primary Sybil-resistance tool — has never activated:

Signal

Value

Reading

Bonus budget wasted

95.6%

Near-total failure

Staked ADA in pools with pledge ratio < 1%

78%

Pledge is absent where stake concentrates

Best-case yield on pledge capital

0.68%/yr

Below passive delegation yield (2.3%/yr)

By every measure, the mechanism is broken.

The question this section asks. Prior work identified a population of struggling pools below the viability line as the primary policy concern. But how many operators are genuinely in that position? Who are they? And is their struggle a cause of the pledge failure — or a consequence of something deeper about who controls the landscape?

How this section answers it:

§4.1 — Theoretical pool classification. A size-based taxonomy grounded in the protocol's own mechanics, separating where operators struggle from where they thrive.

§4.2 — Behind the pools: entity-level analysis.75% of staked supply turns out to be operated by multi-pool entities whose relationship to the pledge mechanism ranges from structural impossibility to strategic indifference.

§4.4 — The full picture. Who wastes, who pledges, and who genuinely struggles, in one synthesis.

4.1. Theoretical pool classification

Before looking at who controls the pools, a structural map of the landscape itself is needed.

4.1.1. The case for pool categorization

The reward curve is continuous — it maps stake to reward without discrete jumps. Yet the pool landscape is not continuous.

A pool with 50K ADA and one with 50M ADA both participate in the same formula, but they inhabit entirely different worlds: one barely produces blocks, the other anchors the delegation market.

Treating them as points on a single spectrum leads to conclusions that are technically correct and analytically useless. Three thresholds — production, viability, and saturation — emerge from the protocol's own mechanics and partition the space into tiers with distinct identities:

Threshold

What it captures

Derived from

Production

Minimum stake for regular block production

Slot leadership probability × epoch length

Viability

Minimum stake to cover operating costs

Fixed-cost floor ÷ reward rate per ADA

Saturation

Maximum efficient stake per pool

Circulating supply ÷ $k$

Each tier has a characteristic behaviour, a characteristic problem (or none), and a characteristic response to parameter changes.

Why this matters for CIP evaluation. These thresholds are dynamic — they are functions of active stake, fixed costs, reward rates, and $k$. When a CIP proposes to change $k$ from 500 to 1000, the saturation cap halves and the tier boundaries shift. When active stake grows from 21B to 35B ADA, the production and viability lines rise. The taxonomy is a framework for reasoning across scenarios, not a snapshot of today's values.

4.1.2. Structural thresholds

4.1.2.1. Production threshold

Key result: at current active stake (21.18B ADA), a pool needs ~3M ADA to be in the productive population — defined as the stake level at which the pool produces at least one block per epoch with 95% probability. The threshold is dynamic: it scales linearly with active participation and rises to ~5.35M ADA at full supply.

Block production is a Poisson process — leadership is assigned slot by slot, and a pool with relative active stake $\sigma$ has expected blocks per epoch $\lambda = L \cdot f \cdot \sigma$ (with $L = 432{,}000$ slots, $f = 0.05$, so $L \cdot f = 21{,}600$). The probability of producing at least one block in a given epoch is:

This is the threshold at which a delegator can rely on the pool producing in 19 of 20 epochs — yield is a signal, not statistical noise. Below 3M ADA, blocks are still produced occasionally — at λ = 1 (~1M ADA stake), a pool has only a 63% chance of producing in any given epoch and 37% chance of producing nothing — but the income is too volatile for a delegator to read or for an operator to plan against.

The mechanism. Cardano's Ouroboros Praos assigns block production rights slot by slot. For each of the $L$ slots in an epoch, a pool with relative active stake $\sigma_i$ is elected slot leader with probability:

$$\phi(f, \sigma_i) = 1 - (1-f)^{\sigma_i}$$

where $f$ is the active slot coefficient and $\sigma_i = \text{stake}_i / S_{\text{active}}$. For small $\sigma_i$ (all pools below saturation), the expected block count simplifies to:

$$E[\text{blocks}_i] \approx L \times f \times \sigma_i$$

The protocol constants have never changed:

Parameter

Symbol

Value

Epoch length

$L$

432,000 slots

Active slot coefficient

$f$

0.05

Expected blocks/epoch

$L \times f$

21,600

The only moving part is total active stake — and that makes the threshold dynamic:

At full participation the 3-block threshold rises to 5.35M ADA — pushing more pools below viability.

Why 3 blocks matters. Block assignments are Poisson-distributed. The coefficient of variation ($\text{CV} = 1/\sqrt{\lambda}$) tells the story:

Pool stake

E[blocks]

CV

What a delegator sees

100K ADA

0.10

316%

Mostly zero — one block is an event

500K ADA

0.51

139%

One block every ~2 epochs, very noisy

~1M ADA

1.00

100%

0 blocks as likely as 2 — unreliable

~3M ADA

3.00

58%

Regular production begins

10M ADA

10.27

31%

Stable reward stream

77M ADA (z₀)

79.09

11%

Near-deterministic

At 1 block/epoch the reward is as variable as its own mean. At 3 blocks/epoch the pool produces in the overwhelming majority of epochs — this is where a delegator can first observe consistent performance.

The ~3M ADA line identified in prior work is not an arbitrary ADA amount: it is the point where Poisson noise stops dominating.

FromObservationPOL.O3 — Three structural thresholds shape pool space: production (physics), viability (economics), saturation (formula)

Finding#1→ The production threshold is physics-based — emergent from slot-leadership, not a parameter. A pool sits in the productive population when it produces at least one block per epoch with 95% probability ($\lambda \geq 3$, since $P(\geq 1) = 1 - e^{-\lambda}$). At today's active stake ($S_{\text{active}} \approx 21.57$B ADA), this requires ~3M ADA of pool stake. Below it, blocks are still produced occasionally — at ~1M ADA the pool has only a 63% chance of producing in a given epoch — but income is too volatile to be read as a usable signal. The threshold rises with active stake: at full supply (~38.5B ADA), the production line climbs to ~5.35M ADA.

Current landscape:

Threshold

Pools above

Active stake covered

≥1 block/epoch (0.97M ADA)

946

99.1%

≥3 blocks/epoch (2.92M ADA)

729

97.3%

≥10 blocks/epoch (10.1M ADA)

511

91.6%

Below this threshold, pools produce too few blocks for delegators to assess reliability — and their reward variance is too high to sustain consistent yields.

4.1.2.2. Viability threshold (orders of magnitude only)

Key result: at today's ADA/USD price (~\$0.25), the operator-viability threshold coincides with the production threshold (~3M ADA stake). The pool generates ~2,150 ADA/epoch on average — enough for the operator to keep the ~390 ADA they need and pass the rest to delegators. But unlike production, viability is volatile — it tracks the ADA/USD price, the operator's fee-structure choices, and the operator's actual cost setup. This section discusses orders of magnitude only; the rest of this document and its visuals do not draw a viability line, because the line moves too much to be a stable analytical reference.

The question. Production tells us whether the pool produces blocks reliably. Viability tells us whether the operator can pay themselves enough — out of the pool's reward stream — to cover real costs. The two answer different questions, and viability layers extra variables on top of production.

Step 1 — what does an operator actually need to take per epoch?

A Cardano stake pool requires one block-producing node and two relay nodes running 24/7 plus the operator's own time to monitor, patch, rotate keys, and participate in governance. Order-of-magnitude annual costs:

Infrastructure (block-producer + 2 relays + monitoring + DNS + backups): \$1,320–3,240/year at common VPS providers.

Operator labour (5–15 hrs/month at DevOps/SRE market rates of \$43–86/hour): ~\$5,160/year at the conservative lower bound (10 hrs/month × \$43/hr).

Total cost floor: ~\$7,160/year minimum, easily doubling for a more demanding setup.

Costs are paid in fiat, so the ADA-equivalent moves with price:

ADA/USD

Cost in ADA/year

Cost in ADA/epoch (73 epochs/yr)

\$0.10

~71,600

~980

\$0.25 (today)

~28,600

~390

\$0.50

~14,300

~196

\$1.00

~7,160

~98

Step 2 — what stake makes the pool generate that much reward?

Network pool pot ≈ 15.5M ADA/epoch distributed across the 21,600 expected blocks/epoch → average reward per block ≈ 715 ADA. A pool with stake σ and λ = 21,600 × σ / S_active expected blocks gets ~λ × 715 ADA/epoch in expectation.

For pool reward = 390 ADA/epoch (the cost an operator needs to extract today):

— but at 549K ADA, $\lambda = 0.55$ → P(0 blocks per epoch) = $e^{-0.55} \approx 58\%$. The pool earns 0 in over half of all epochs, with sporadic bursts when it wins a block. Income at this stake level is mathematically positive but operationally unreliable.

Step 3 — viability collapses to production (today).

For the operator's income to be reliable enough to plan against, the pool must sit at the production threshold (~3M ADA, λ=3, 95% prob of ≥1 block). At that level:

Expected pool reward = 3 × 715 = 2,145 ADA/epoch, reliably (95% of epochs)

Operator needs only ~390 ADA/epoch of that — about 18% of pool reward

The remaining 82% is available for delegators

At \$0.25 ADA, the operator-viability threshold is therefore the production threshold (~3M ADA). The pool generates 5.5× what the operator needs; viability is comfortably absorbed by reliable production.

How viability moves with price.

ADA/USD

Cost (ADA/epoch)

Stake for that reward in expectation

Reliable-income floor

\$0.10

~980

~1.4M ADA

~3M ADA (production-bound)

\$0.25 (today)

~390

~549K ADA

~3M ADA (production-bound)

\$0.50

~196

~275K ADA

~3M ADA (production-bound)

\$1.00

~98

~140K ADA

~3M ADA (production-bound)

Across this range, the expectation-only stake target moves between ~140K and ~1.4M ADA — but the reliable-income floor (where Poisson noise is small enough that monthly income covers monthly costs in nearly every epoch) is always at or above the production threshold.